Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

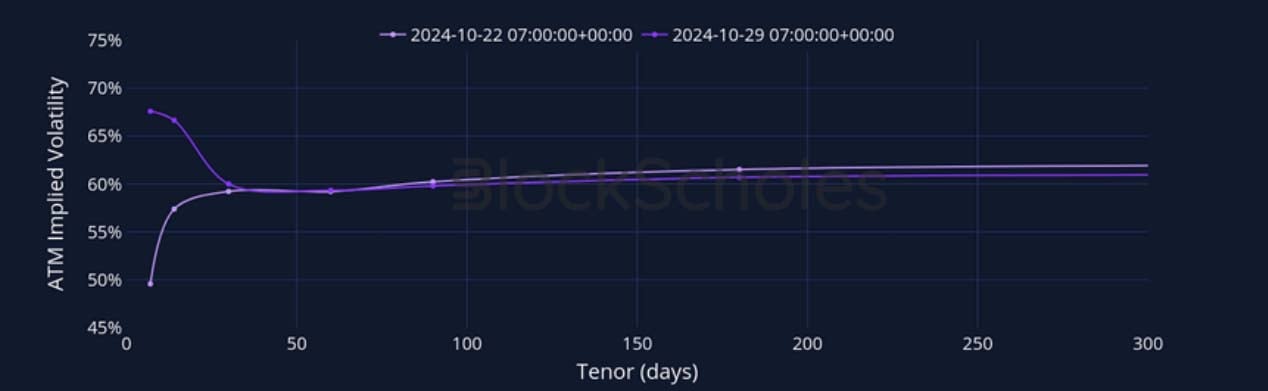

The bullish pre-election positioning that we saw building up earlier in October has continued with vigour over the last 3 days. Futures-implied yields, perpetual swap funding rates, and now implied volatility have risen to months-long highs, with short-tenor option expiries out-performing to invert the term structure of volatility in a similar manner to the shape we observed ahead of the ETF launch in January. ETH derivatives indicate an expectation that the second largest crypto-currency will continue its years- long trend of under-performance through the event risk, lagging BTC in all metrics and assigning a 10 point volatility premium over BTC, but echo the trend of increasing bullish sentiment that we see expressed across markets.

Futures Implied Yield, 1-Month Tenor

ATM Implied Volatility, 1-Month Tenor

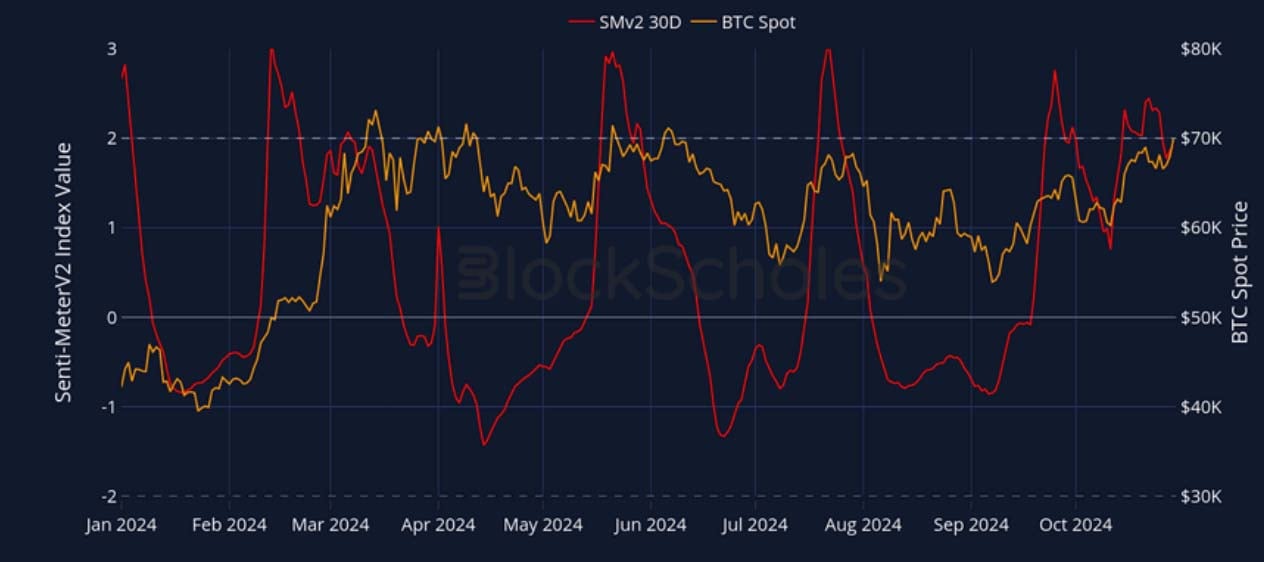

Crypto Senti-Meter

BTC Derivatives Sentiment

ETH Derivatives Sentiment

Futures

BTC ANNUALISED YIELDS – The inversion of the yield term structure has deepened, reflecting increasing leveraged long positioning ahead.

ETH ANNUALISED YIELDS – futures yields invert, albeit to lower levels than BTC, reflecting bullish-but-not-that-bullish positioning ahead of the election.

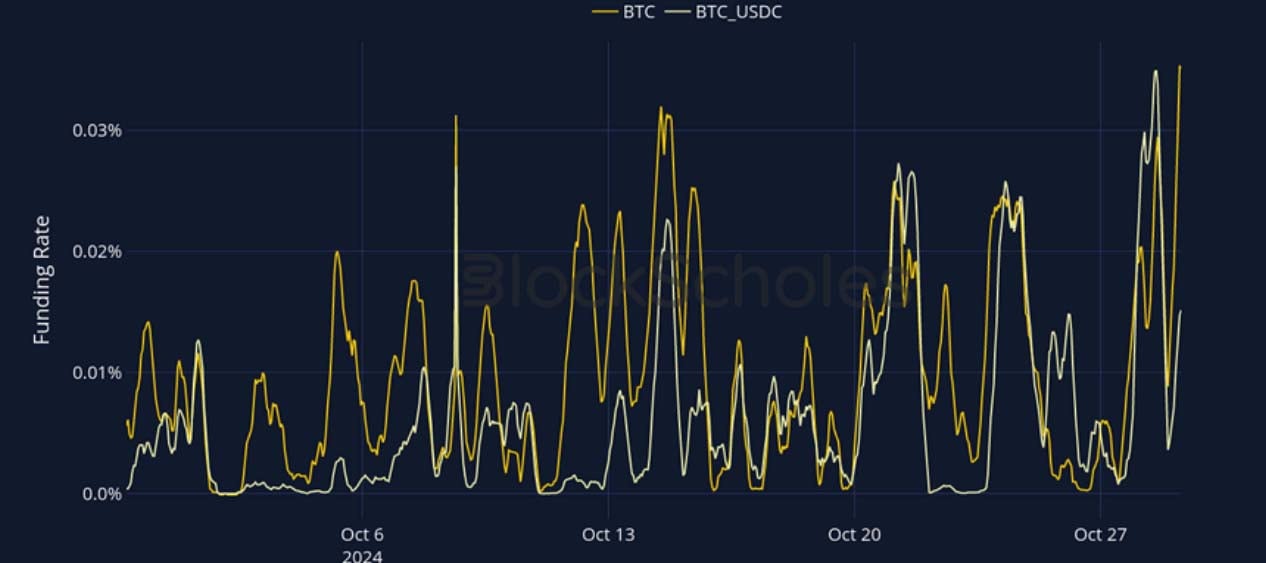

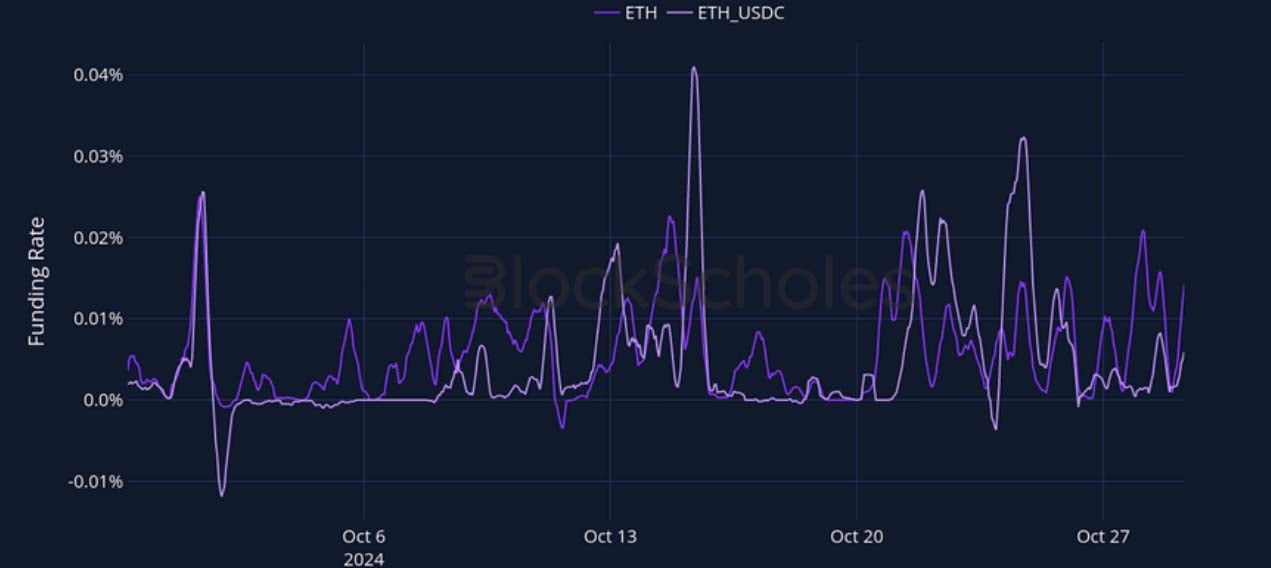

Perpetual Swap Funding Rate

BTC FUNDING RATE – Intense and sustained positive funding rates reflect a willingness to pay for leveraged long exposure into next week’s event risk.

ETH FUNDING RATE – ETH’s funding rate reflects the same conclusion as it’s futures yields – bullish positioning but without the same exuberance as BTC.

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – The term structure of volatility has finally inverted after months of an election-dated volatility premium.

BTC 25-Delta Risk Reversal – A brief reversal of short-dated sentiment over the last 2 days has resolved with a return to a bullish skew towards OTM calls.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – ETH’s term structure has inverted heavily at short-dated tenors, indicating a rush into pre-election positioning.

ETH 25-Delta Risk Reversal – Despite lagging BTC’s bullishness in futures and perps, ETH’s vol smiles are similarly skewed towards upside exposure.

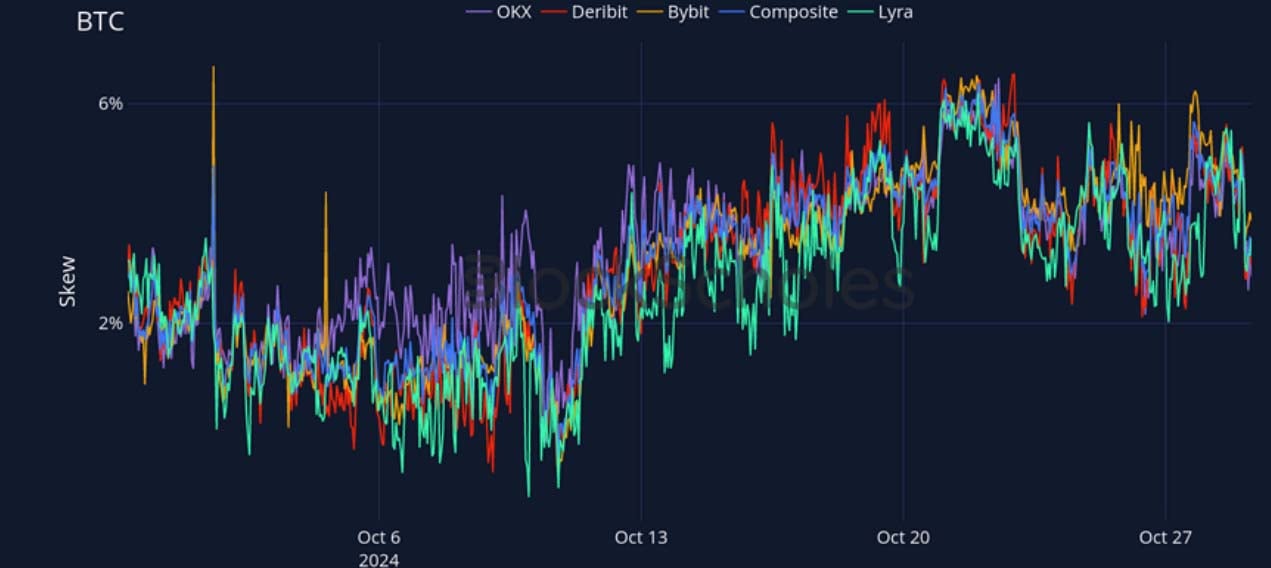

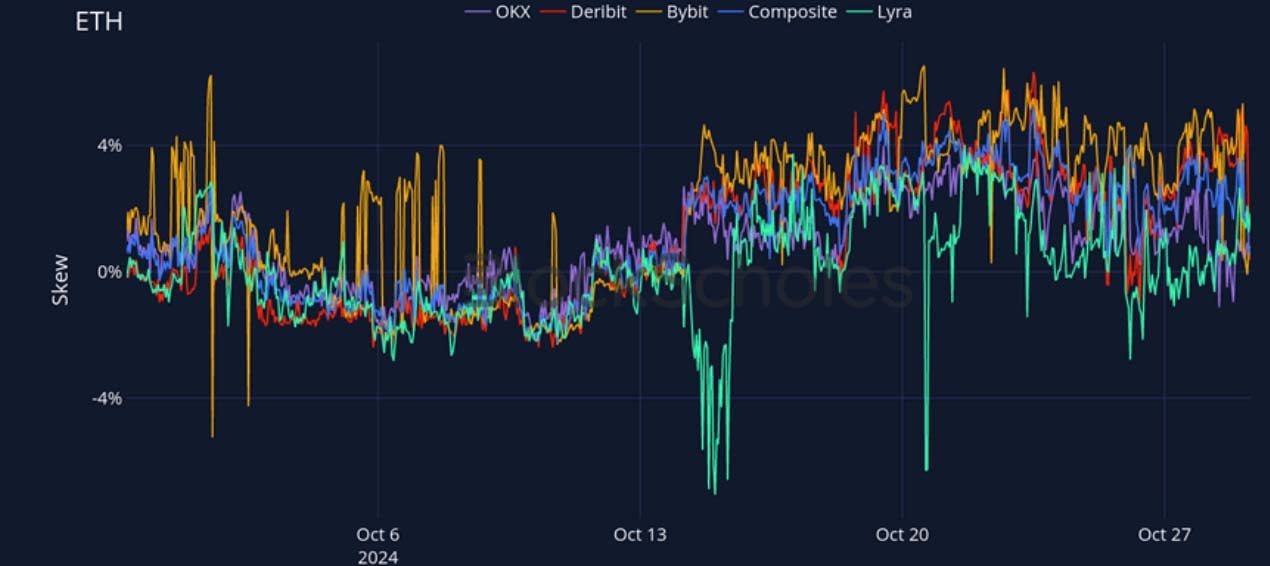

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

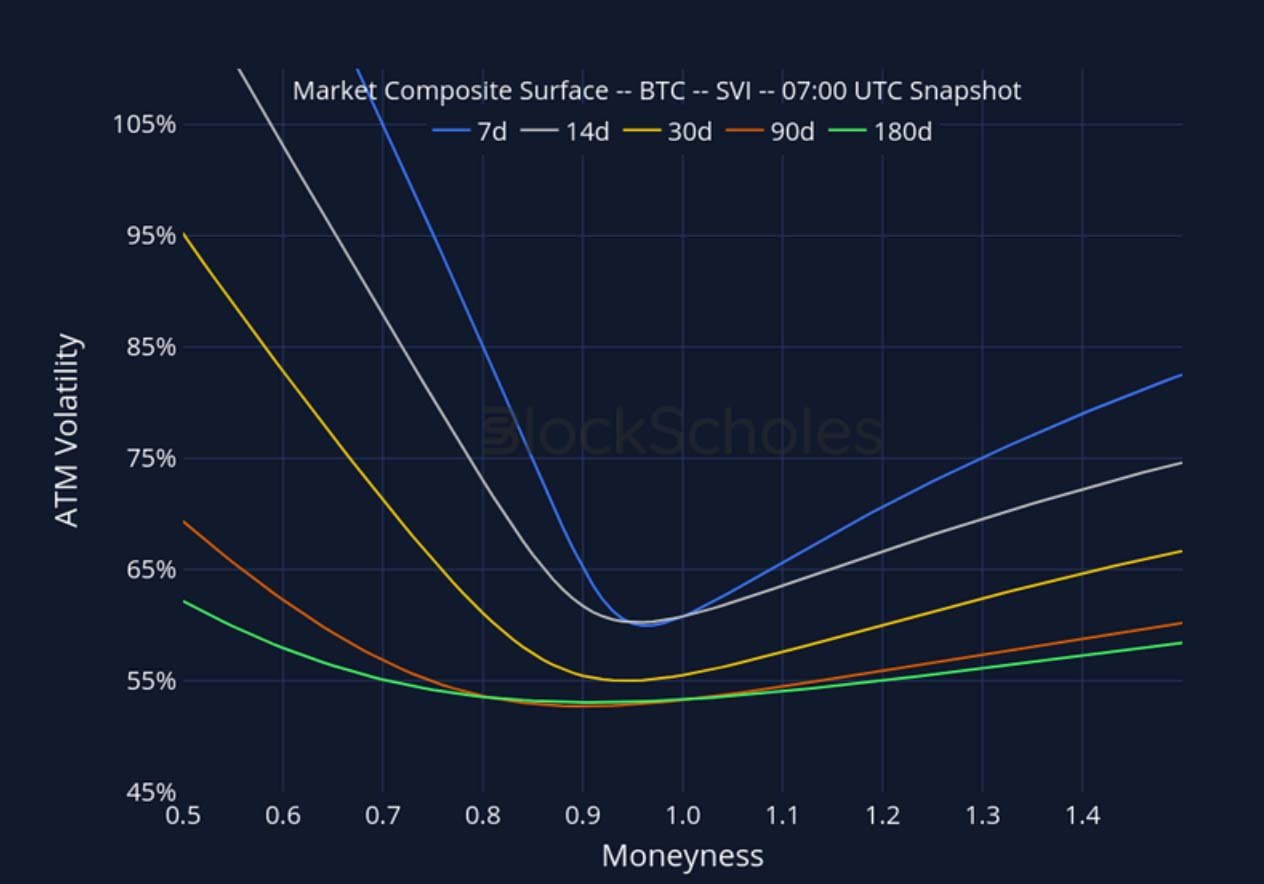

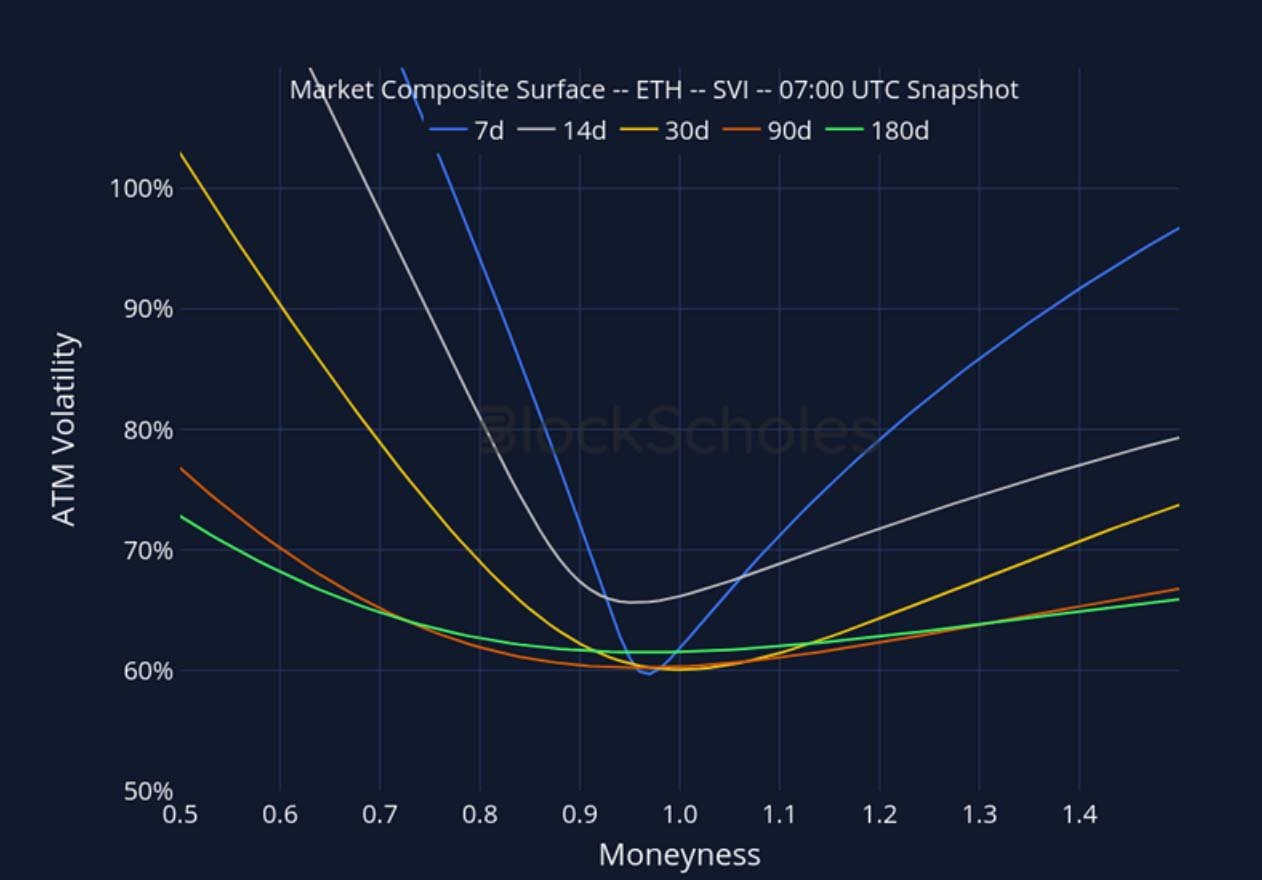

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 7:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 7:00 UTC Snapshot.

Listed Expiry Volatility Smiles

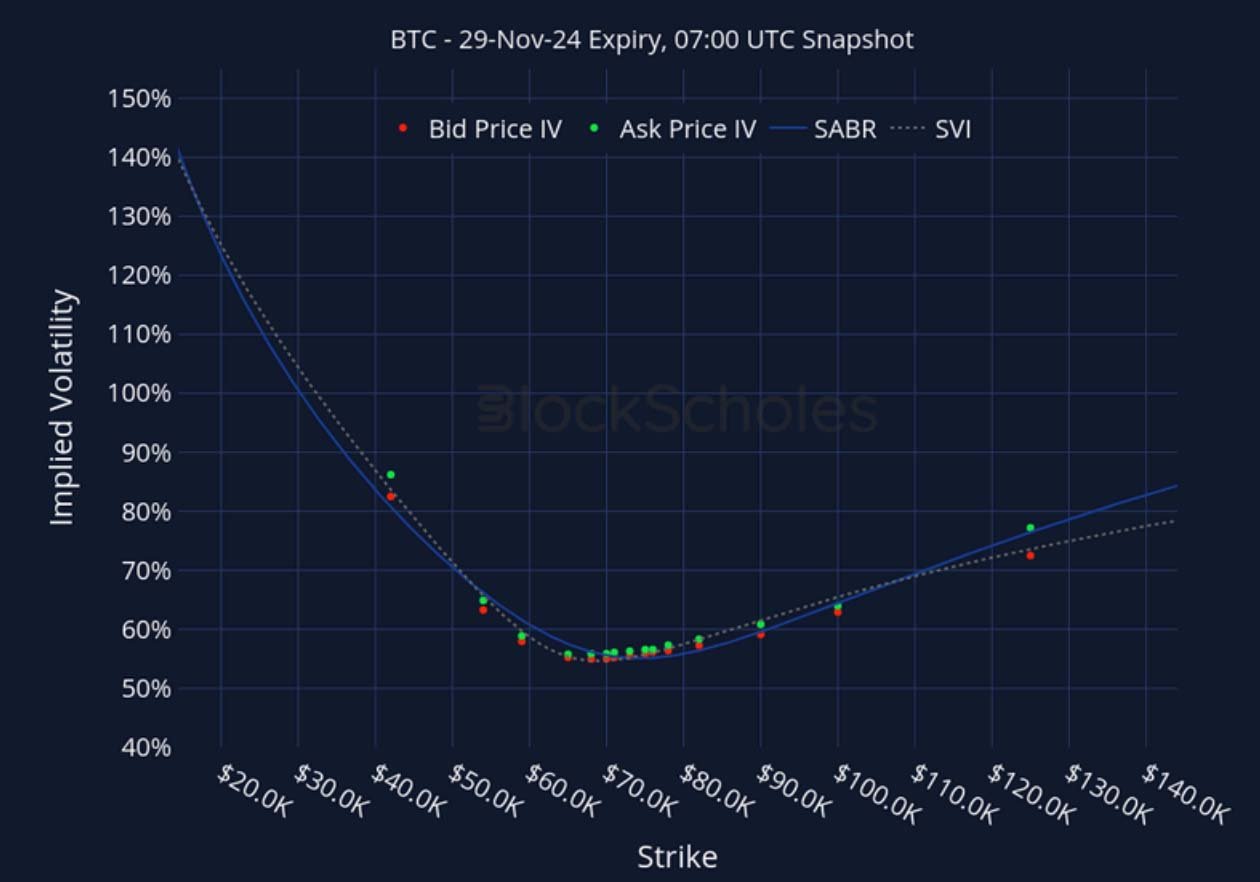

BTC 29-NOV EXPIRY – 7:00 UTC Snapshot.

ETH 29-NOV EXPIRY – 7:00 UTC Snapshot.

Cross-Exchange Volatility Smiles

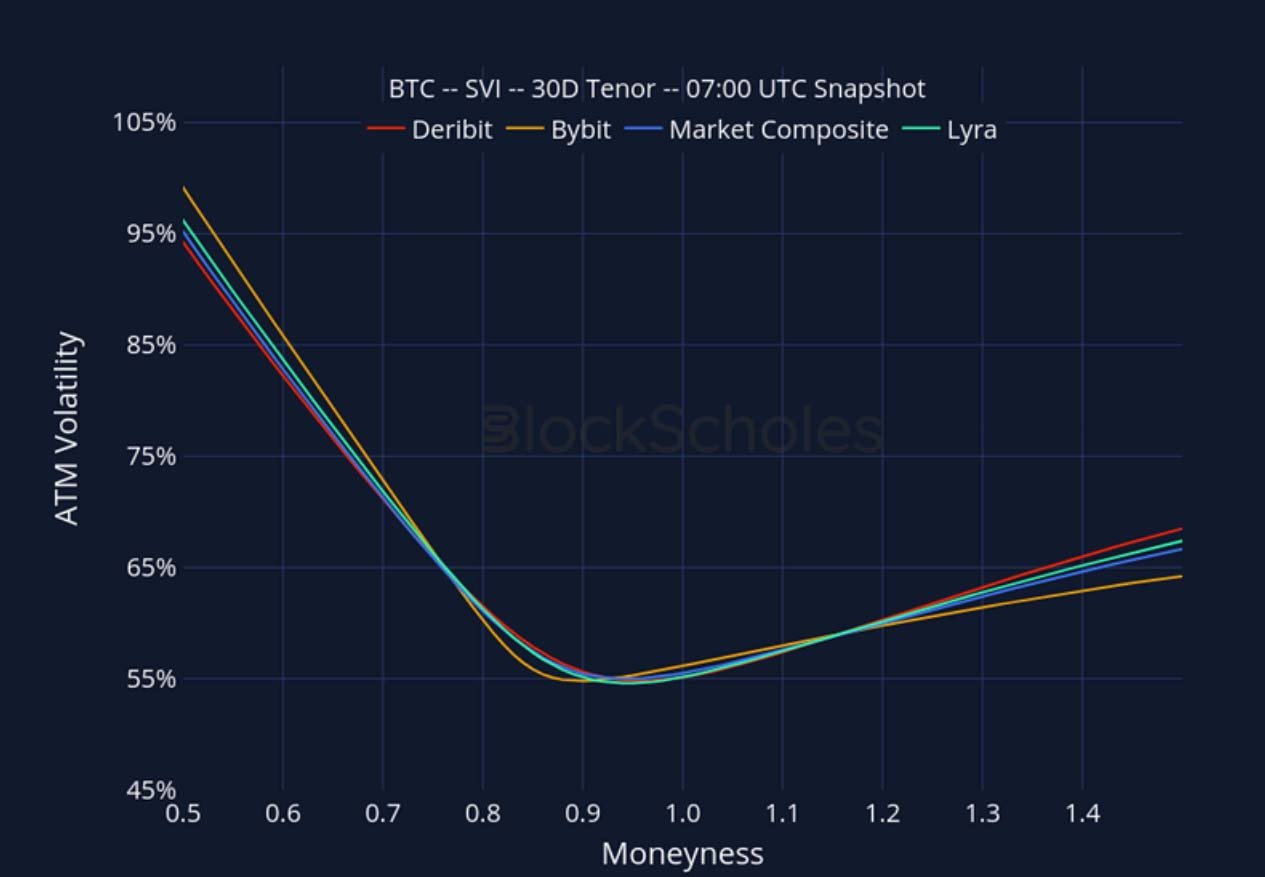

BTC SVI, 30D TENOR – 7:00 UTC Snapshot.

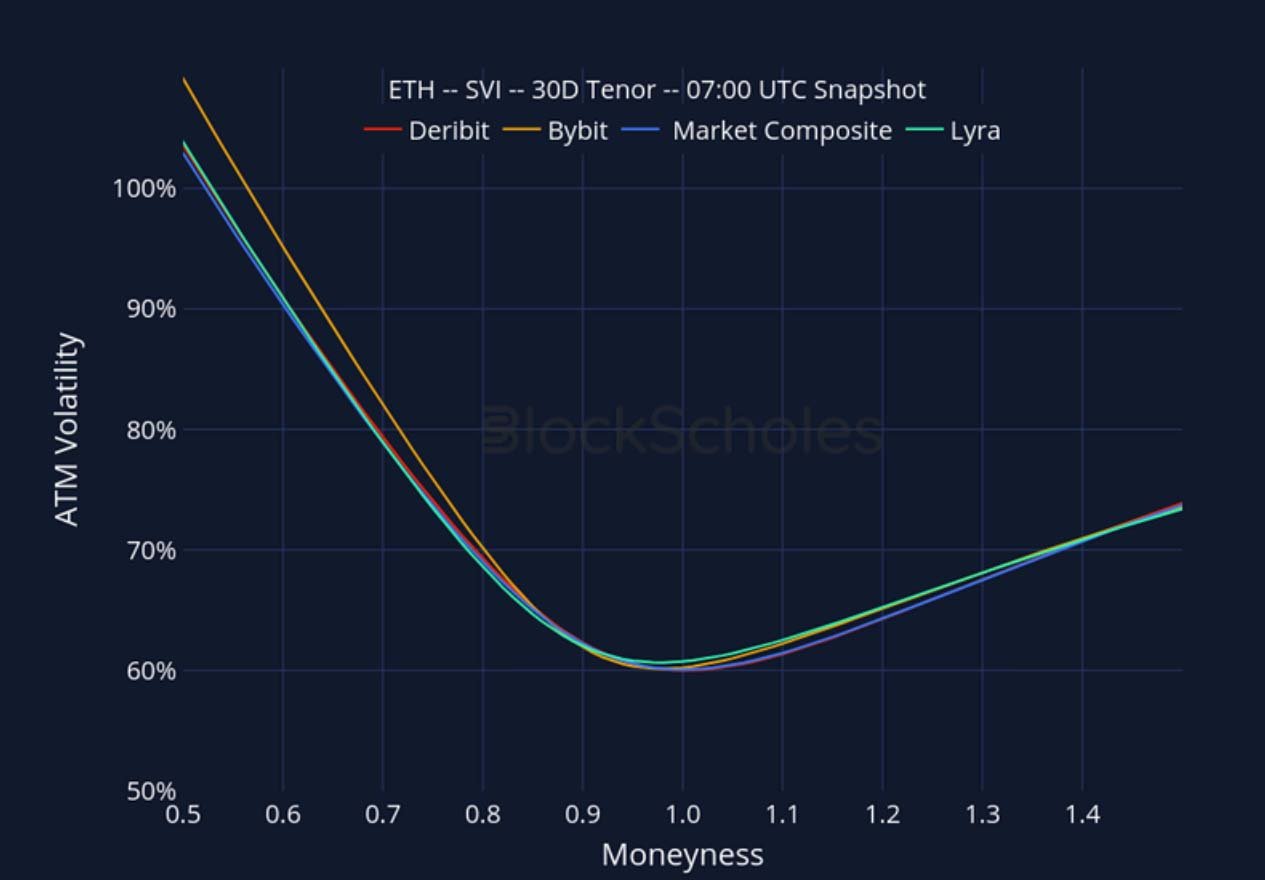

ETH SVI, 30D TENOR – 7:00 UTC Snapshot.

Constant Maturity Volatility Smiles

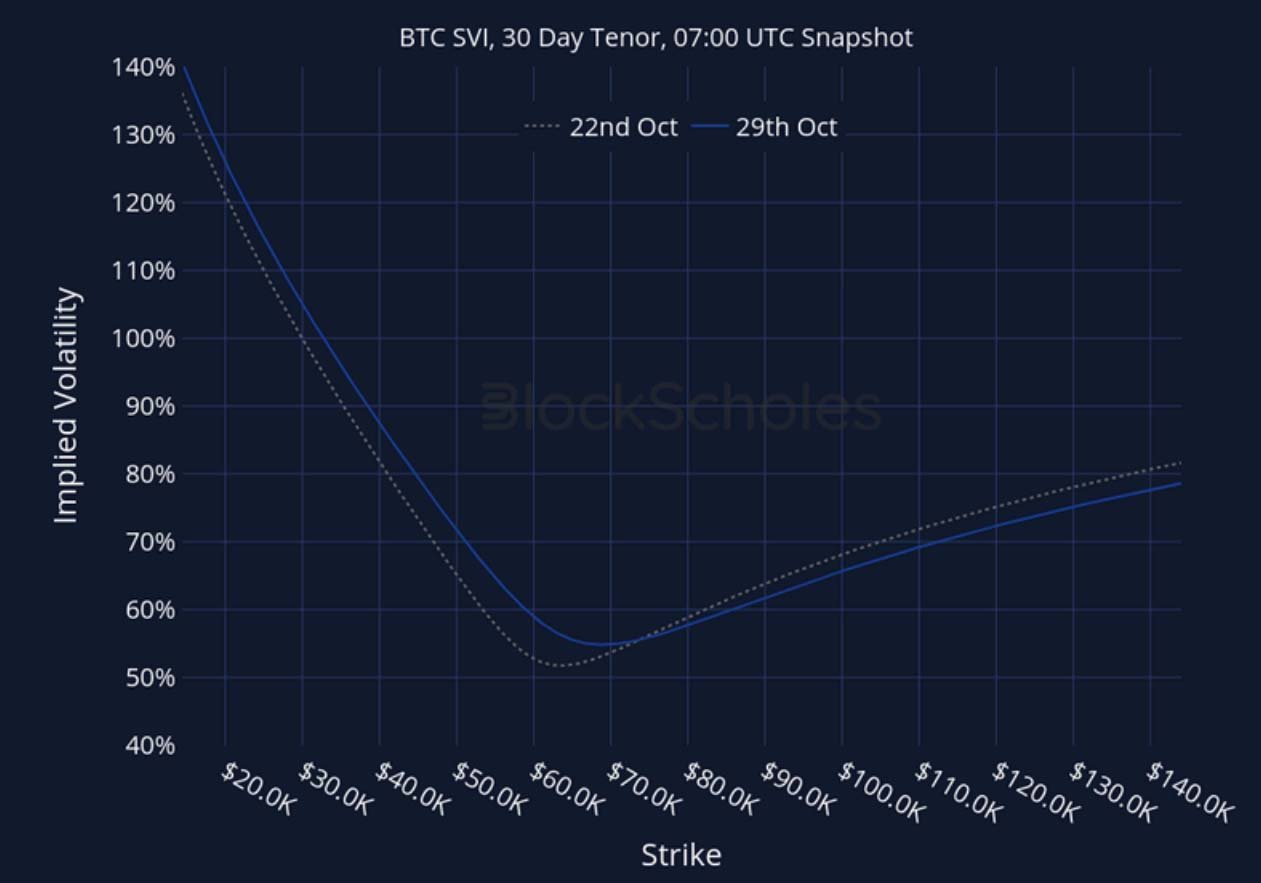

BTC SVI, 30D TENOR – 7:00 UTC Snapshot.

ETH SVI, 30D TENOR – 7:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.

RECENT ARTICLES

Crypto Derivatives: Analytics Report – Week 44

Block Scholes2024-10-31T09:08:42+00:00October 31, 2024|Industry|

BTC Takes Out 70k As Trump Odds Run Higher

Imran Lakha2024-10-30T10:28:15+00:00October 30, 2024|Industry|

Vol Commentary: Election Play

Cumberland2024-10-30T05:49:42+00:00October 30, 2024|Industry|

The post Crypto Derivatives: Analytics Report – Week 44 appeared first on Deribit Insights.