Author:Nathan Frankovitz, Matthew Sigel

Compiled by: Wu Blockchain

Driven by the regulatory tailwind from Trump's election, Bit has successfully broken through its historical high. As market attention continues to rise, various key indicators suggest that the strong momentum of this bull market is likely to persist.

As we predicted in September, Bit (BTC) price experienced high volatility and surged after the election. Now, Bit has entered uncharted territory without technical price resistance, and we believe the next stage of the bull market has just begun. This pattern is similar to 2020, when Bit price doubled by the end of the year and further increased by about 137% in 2021. As the government's supportive attitude towards Bit has undergone a significant transformation, investor interest is rapidly increasing. Recently, the number of investment inquiries we have received has surged, and many investors have realized that their allocation to this asset class is clearly insufficient. Although we are closely monitoring the market for signs of overheating, we reiterate our forecast of a Bit price target of $180,000/BTC for this cycle, as the key indicators we track continue to show bullish signals.

Bit Price Trends

Market Sentiment

Bit's 7-day moving average (7 DMA) has reached a new all-time high of $89,444. On election night on Tuesday, November 5, Bit soared about 9% to a new all-time high of $75,000. This is consistent with our previous observation: when the likelihood of a Trump victory increases, Bit price tends to rise. Trump explicitly promised in his campaign to end the "enforcement-based" strategy of the U.S. Securities and Exchange Commission (SEC) and make the U.S. the "capital of crypto and Bit".

After Trump's election as president, regulatory resistance has turned into a driving force for the first time. Trump has already begun appointing crypto-friendly officials in the executive branch, and with the Republican Party in control of the unified government, the likelihood of relevant supportive legislation being passed has increased. Key proposals include plans to establish a national Bit reserve and rewrite legislation related to the crypto market structure and stablecoins, with FIT21 expected to be rewritten in market and privacy-friendly terms, and new stablecoin drafts allowing state-chartered banks to issue stablecoins without Federal Reserve approval.

As countries like the BRICS are exploring alternative options like Bit to circumvent U.S. dollar sanctions and currency manipulation, stablecoins provide a strategic opportunity for the U.S. to project the dollar globally. By eliminating regulatory barriers and allowing state-chartered banks to issue stablecoins, the U.S. can maintain the global influence of the dollar and leverage the faster adoption of cryptocurrencies in emerging markets. These markets have a voracious demand for financial services, hedging against local currency inflation, and DeFi.

We expect the SAB to be repealed in the first quarter of Trump's term, if not by the SEC, then by Congress, which will prompt banks to announce crypto custody solutions. If Gary Gensler has not yet resigned, Trump may fulfill his promise to replace the SEC chairman with a more crypto-friendly candidate and end the agency's notorious "regulation by enforcement" era. Furthermore, by 2025, the U.S. will revise its ETH ETF to support Staking, the SEC will approve Solana's (SOL) ETF 19b-4 proposal, and the ability to create and redeem ETFs in-kind will make these products more tax-efficient and liquid. Given Trump's prior acknowledgment of the energy-intensive commonalities between Bit mining and artificial intelligence (AI), we expect energy regulations to be relaxed, making baseload energy (such as nuclear) cheaper and more abundant, thereby boosting U.S. global leadership in energy, AI, and Bit.

This election marks a bullish inflection point, reversing the previous hawkish policies that have led to the outflow of capital and jobs. By unleashing entrepreneurial dynamism, the U.S. is poised to become the global leader in crypto innovation and employment, transforming cryptocurrencies into a key domestic growth industry and an important export product for emerging markets.

Bit Dominance

The 7-day moving average of Bit dominance (a metric measuring Bit's market capitalization relative to the total market capitalization of all cryptocurrencies) has risen 2 percentage points this month to 59%, the highest level since March 2021. While this upward trend, which began from 40% in November 2022, may continue in the short term, it is likely to peak soon. In September, we pointed out that a Harris victory could boost Bit's dominance due to a clearer regulatory status as a commodity. In contrast, Trump's pro-crypto stance and his expanded cabinet team are likely to drive more widespread crypto market investment. As Bit reaches new highs in a crypto-friendly regulatory environment, the wealth effect and reduced regulatory risk are expected to attract native capital and new institutional investors to DeFi, boosting the returns of smaller projects in the asset class.

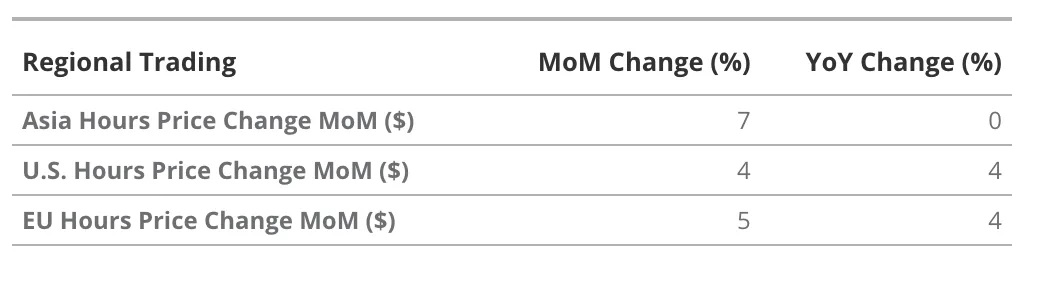

Regional Trading Dynamics

At first glance, traders in the Asian market trading session appear to have significantly increased their Bit holdings this month, contrary to the trend in recent years where Asian traders have typically been net sellers while European and U.S. traders have been net buyers. However, the surge in Bit price on election night occurred during the Asian trading session, which was likely due to a large number of U.S. investors trading around the election. This specific event makes it difficult to fully attribute such price movements to regional dynamics. Consistent with historical behavior, traders in the U.S. and European trading sessions continue to increase their Bit holdings, maintaining the price performance trend observed in October.

Source: glassnode, 11/18/24 (Past performance does not guarantee future results.)

Key Indicators

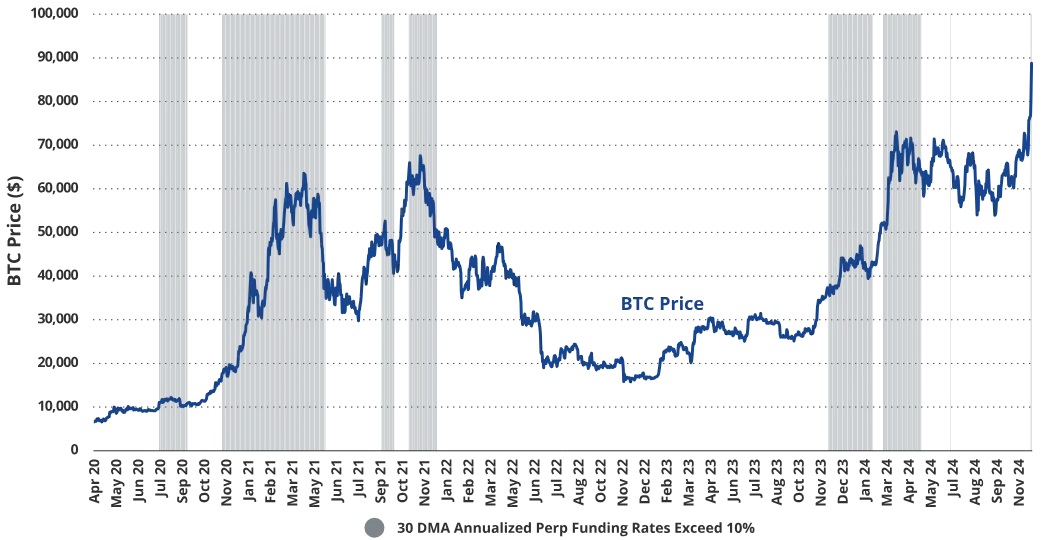

To assess the potential upside and duration of this bull market, we analyzed several key indicators to evaluate the market's risk level and potential price tops. This month, our analysis starts with perpetual contracts (perps), where the performance of the funding rate provides insights into market sentiment and helps gauge the likelihood of market overheating.

Bit price typically exhibits signs of overheating when the 30-day moving average of perpetual funding rates (30 DMA Perp Funding Rates) exceeds 10% and persists for 1 to 3 months.

Comparison of BTC Average Returns and Perpetual Funding Rates (January 4, 2020 - November 11, 2024)

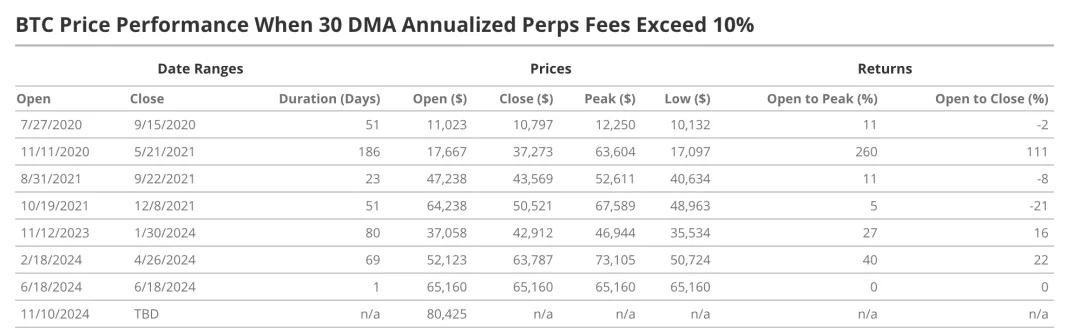

BTC Price Performance When 30 DMA Annualized Perps Fees Exceed 10%

Source: glassnode, as of November 12, 2024

Starting from April 2020, we analyzed the periods when the 30-day moving average of perpetual contract funding rates exceeded 10%. The average duration of these periods was about 66 days, with an average return from open to close of 17%, although the duration of individual periods varied significantly. The only exception was the single-day spike on June 18, 2024, reflecting short-term market sentiment. Other instances persisted for weeks, highlighting a structural bullish sentiment that typically leads to significant short-to-medium-term gains.

For example, the high capital cost rate phase that began on August 31, 2021 lasted for 23 days, followed by a 28-day cooling period, and then resumed for another 51 days on October 19. If this brief interval is included, the total duration of the high capital cost rate in 2021 reached 99 days. Similarly, the current high capital cost rate phase that began on November 12, 2024 lasted for 80 days, followed by a 19-day interval, and then resumed for another 69 days of high capital cost rate, totaling 168 days, comparable to the 186 days from November 11, 2020 to May 21, 2021. It is worth noting that when the capital cost rate exceeds 10%, the average return rate for BTC purchases within the 30-day, 60-day and 90-day time frames is higher than on days with lower capital cost rates.

However, the data shows that there is a pattern of underperformance over a longer time frame. On average, BTC purchased on days when the capital cost rate exceeds 10% starts to lag the market from 180 days onwards, and this trend becomes more pronounced within the 1-year and 2-year time frames. Given that market cycles typically last around 4 years, this pattern suggests that sustained high capital cost rates are often associated with cycle tops and may serve as an early signal of market overheating, indicating a higher risk of long-term downside.

Source: glassnode, as of November 13, 2024

As of November 11, BTC has entered a new phase, with the capital cost rate exceeding 10% again. This shift indicates stronger short-term to medium-term momentum, as historically higher capital cost rates have been associated with higher 30-day, 60-day and 90-day returns, reflecting higher bullish sentiment and demand. However, as the capital cost rate remains elevated, we may depart from the stage where long-term (1-2 year) returns are equally favorable. Given the current supportive regulatory environment for BTC, we expect another high-performance period to emerge, similar to the one following the 2020 US elections, when sustained capital cost rates above 10% drove 260% growth in 186 days. With BTC currently trading around $90,000, our $180,000 target price remains viable, reflecting a potential cycle return of around 1,000% from trough to peak.

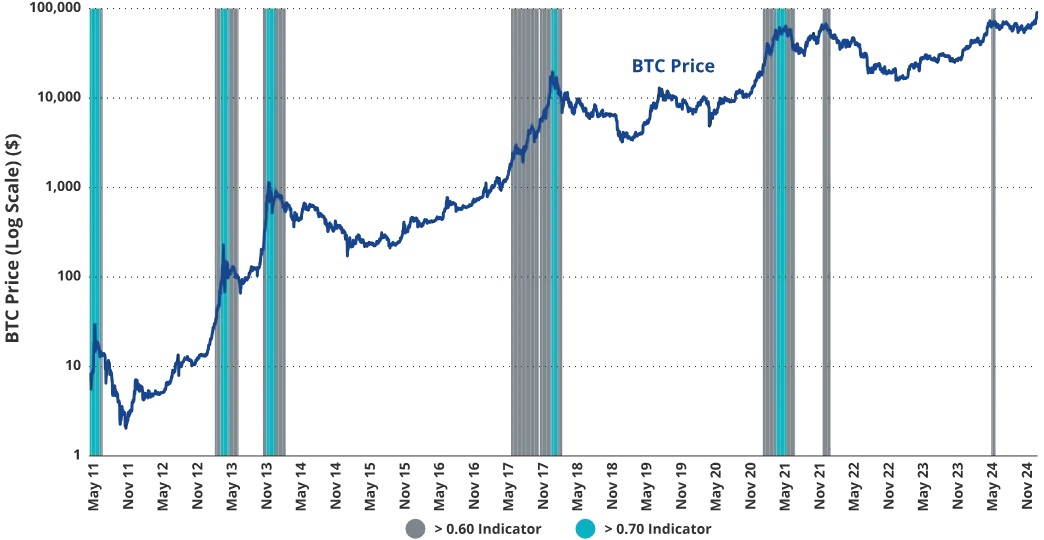

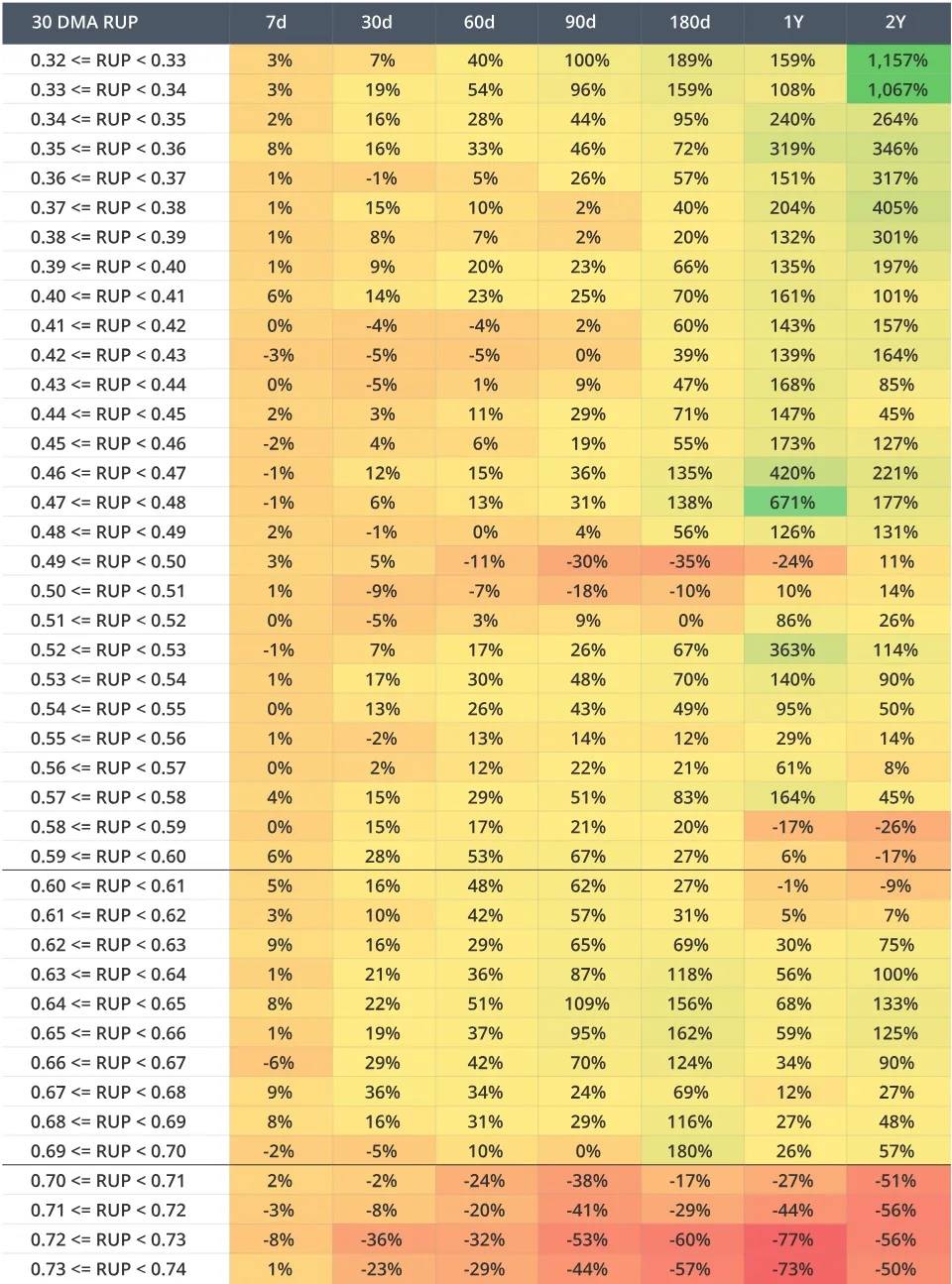

Higher 30-day moving average (DMA) relative unrealized profit (RUP) levels (>0.60 and 0.70) have historically often signaled BTC price tops.

BTC Average Earnings vs. 30-day Moving Average Relative Unrealized Profit (RUP) (November 13, 2016 - November 13, 2024)

Source: glassnode, as of November 13, 2024

BTC Average Earnings vs. 30-day Moving Average Relative Unrealized Profit (RUP) (November 13, 2016 - November 13, 2024)

Source: glassnode, as of November 13, 2024

Next, we focus on Relative Unrealized Profit (RUP), another important metric for assessing whether the BTC market is overheated. RUP measures the proportion of the total BTC market capitalization that is comprised of unrealized gains (i.e., paper profits that have not yet been realized through selling). As BTC prices rise above the average purchase price of most holders, this metric rises, reflecting more of the market entering a profitable state and thus exhibiting bullish sentiment.

Historically, high 30-day moving average (DMA) RUP levels (especially above 0.60 and 0.70) have often signaled strong and potentially overheated market sentiment. As shown by the red zones in the chart, when the 30-day DMA RUP exceeds 0.70, it has often coincided with market tops, as the high proportion of unrealized profits triggers more profit-taking. Conversely, when RUP levels fall below 0.60, it indicates more favorable market conditions for long-term buying, with historical data showing higher 1-year and 2-year returns when buying below this threshold.

Analysis of the past two market cycles suggests that 30-day DMA RUP levels between 0.60 and 0.70 have typically delivered the highest short-term to medium-term returns (7 days to 180 days). This range often reflects the mid-stage of a bull market, where bullish sentiment is rising but has not yet reached excessive levels. In contrast, when RUP exceeds 0.70, returns across all time frames exhibit a negative correlation, reinforcing its role as a strong sell signal.

As of November 13, BTC's 30-day DMA RUP is around 0.54, but the daily value has exceeded 0.60 since November 11. According to our detailed data, risks start to rise when RUP approaches 0.70, underscoring the importance of short-term trading within the 0.60 to 0.70 range. However, if the 30-day DMA RUP rises closer to 0.70, it may signal market overheating, warranting caution on long-term positions.

Crypto Search Trends in the US

Source: Google Trends, as of November 18, 2024

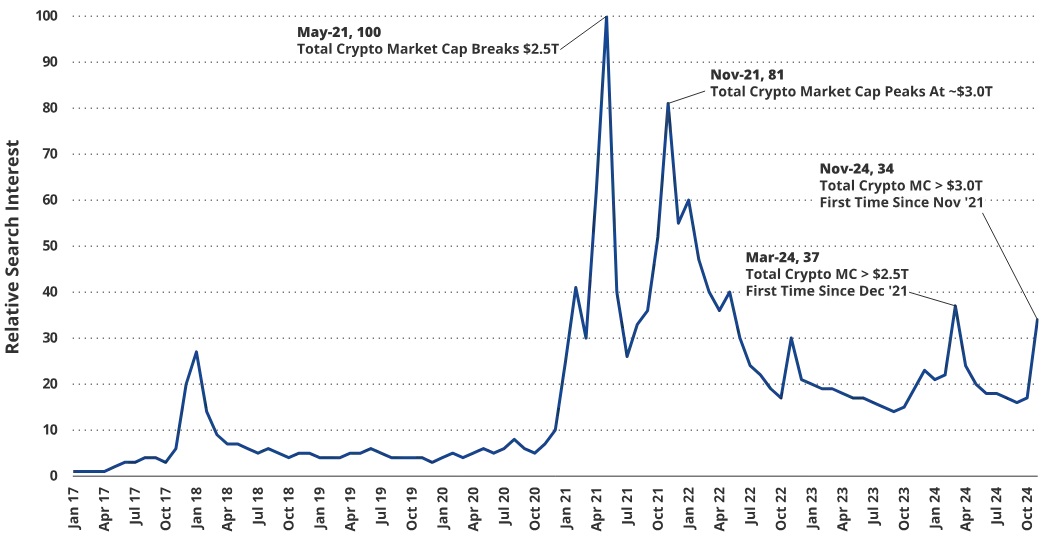

The search interest for 'Crypto' as a Google search term is an important indicator of retail investor interest and market momentum. Historical data shows that peaks in search interest have typically coincided with peaks in the overall crypto market capitalization. For example, the search interest reaching all-time highs in May and November 2021 were followed by significant market declines: a roughly 55% correction over about two months after the May peak, and a bear market of around 12 months and 75% decline after the November peak.

Currently, the search interest is only 34% of the May 2021 peak, slightly lower than the 37% local peak observed in March 2024 (when BTC reached the highest price of this cycle). This relatively low search interest suggests that BTC and the broader crypto market have not yet entered a speculative frenzy stage, leaving room for further growth without reaching the mainstream attention levels typically associated with market tops.

Coinbase App Store Ranking

Source: openbb.co, as of November 15, 2024

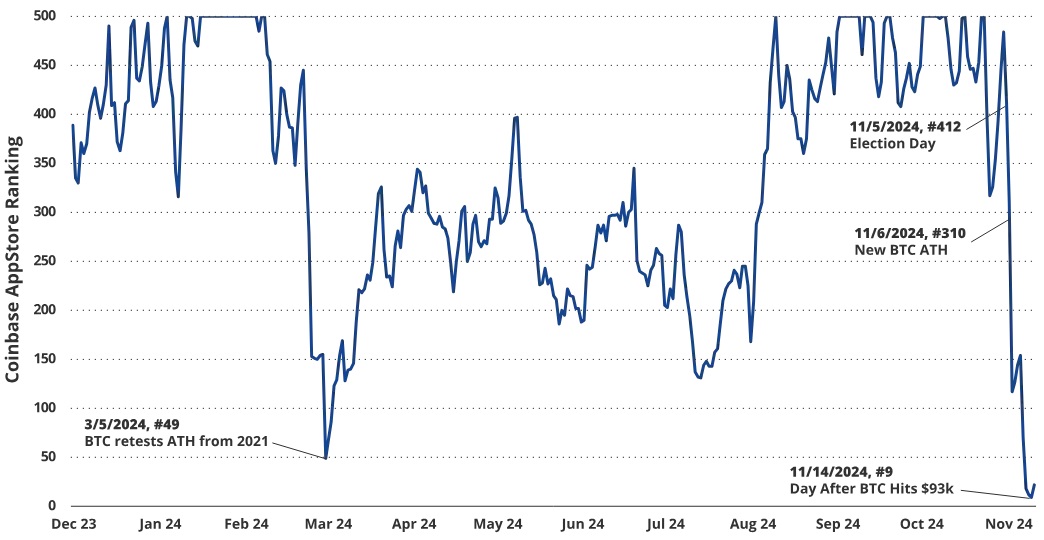

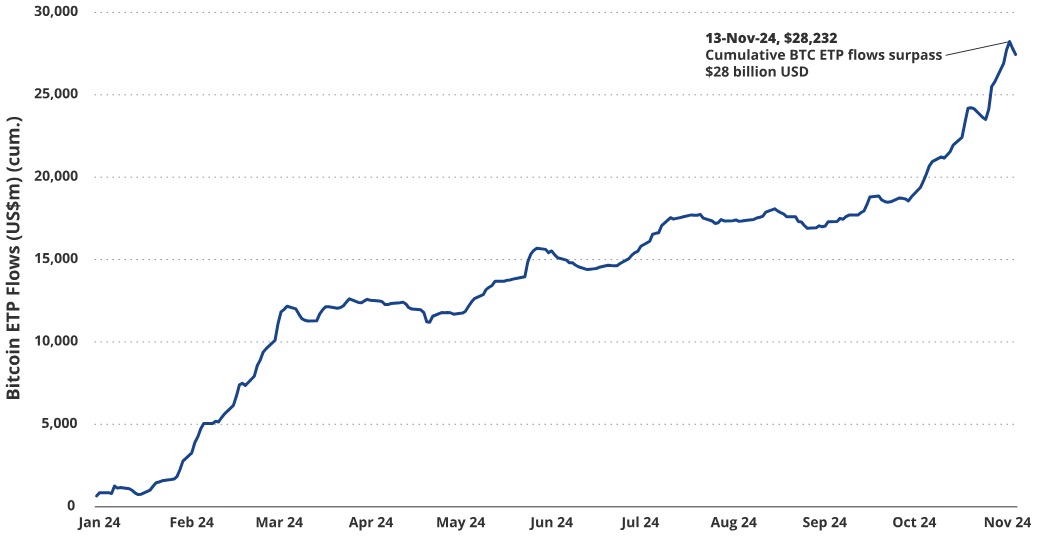

Similar to the Google search interest in 'Crypto', the Coinbase app store ranking is another important indicator of retail investment interest. On March 5th, after BTC prices surged around 34% in 9 days and retested the 2021 all-time high around $69,000, Coinbase re-entered the top 50 app store rankings. Although BTC reached a new high of around $74,000 later that month, as price volatility subsided into the summer doldrums and public attention shifted to the presidential election, retail interest waned. However, BTC's breakout on election night reignited retail interest, with Coinbase's app store ranking soaring from #412 on November 5th to #9 on November 14th. The surge in engagement drove further price appreciation and set a new record for BTC ETF inflows.

BTC Network Activity, Adoption, and Fees

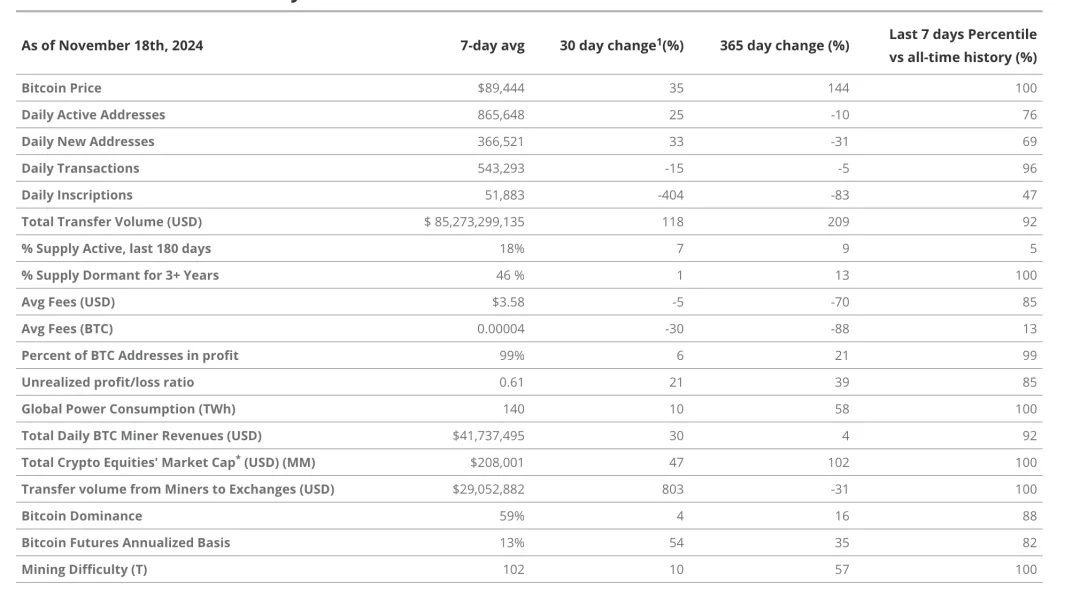

Daily Transactions: The 7-day moving average of daily transaction volume is around 543,000, down 15% quarter-over-quarter. Despite the decline, activity remains robust, at the 96th percentile of BTC's historical range. While transaction counts have decreased, larger transaction loads have offset this impact, as evidenced by the rise in transfer volumes.

Ordinals Inscriptions: Daily Ordinals (NFTs and meme coins on the BTC blockchain) transaction volume grew 404% quarter-over-quarter, reflecting a resurgence of speculative fervor driven by price appreciation and favorable regulatory developments.

Total Transfer Volume: BTC transfer volumes grew 118% quarter-over-quarter, with a 7-day moving average of around $85 billion.

Average transaction fee: Bitcoin transaction fees decreased by 5% quarter-over-quarter, with an average fee of $3.58, and an average transaction value of approximately $157,000, corresponding to a transaction fee rate of around 0.0023%.

Bitcoin Market Health and Profitability

Profitable address ratio: As BTC price reached new all-time highs, currently around 99% of BTC addresses are in a state of profitability.

Unrealized Net Profit/Loss: This ratio has increased by 21% over the past month, reaching 0.61, indicating a significant improvement in the relative balance between unrealized profits and unrealized losses. As a market sentiment indicator, this ratio is currently in the "Belief-Denial" zone, corresponding to the rapid expansion and contraction phase between the peak and trough of the market cycle.

Bitcoin On-Chain Monthly Dashboard

Source: glassnode, VanEck Research, as of October 15, 2024

BTC Miners and Crypto Market Capitalization

Mining Difficulty (T):

The BTC network difficulty has increased from 92 T to 102 T, reflecting miners expanding and upgrading their equipment fleet. The BTC network automatically adjusts the difficulty every 2,016 blocks (approximately two weeks) to ensure the mining time for each block is around 10 minutes. The increase in difficulty indicates intensified competition among miners, which also represents a robust and secure network.

Miners' Daily Total Revenue:

Miners' daily revenue increased by 30% quarter-over-quarter, benefiting from the rise in BTC price, but BTC-denominated transaction fees decreased by 30%, impacting the total revenue to some extent.

Miners' Transfers to Exchanges:

On November 18th, miners transferred approximately $181 million worth of BTC to exchanges, which is 50 times the previous 30-day average, driving a 803% quarter-over-quarter increase in the 7-day moving average. This extreme movement is the highest level since March, similar to the period before the last BTC halving. While the sustained high miner-to-exchange transfer volume may indicate an overheated market, this peak occurred after the summer miner sell-off at lower levels, suggesting it is for operational and growth purposes, rather than a signal of a market top.

Crypto Equities Total Market Cap:

The 30-day moving average of the MarketVector Digital Assets Stock Index (MVDAPP) increased by 47% quarter-over-quarter, outperforming BTC. Major index constituents like MicroStrategy and Bitcoin mining companies, through their BTC holdings or mining operations, directly benefit from the rise in BTC price. Meanwhile, companies like Coinbase also capitalize on the broader crypto market gains, as the price appreciation drives expectations for increased trading fees and other revenue sources.

Source: farside.co.uk, as of November 18, 2024