Author:donn

Compiled by: TechFlow

I've always been fascinated by novel token economics (tokenomics). Observing how crypto protocols adjust their incentive mechanisms is always intriguing, and sometimes they look very tempting - until they inevitably collapse. So when Bittensor launched its dynamic $TAO (dTAO) system on Valentine's Day, I was immediately drawn in.

The idea is simple: to provide a new, more "fair" distribution of TAO issuance across subnets.

But just a month later, the problems have surfaced. It turns out that the seemingly perfect design doesn't always work as intended in a free market.

How dTAO Works

Here's a simplified overview of how the dTAO mechanism works:

Each subnet has its own subnet token ($SN), which exists in the form of a native TAO-SN UniV2 type pool. Confusingly, while users are "staking" TAO to receive SN, this is functionally no different from "exchanging" TAO for SN. The only difference is that users cannot add liquidity to the liquidity pool, nor can they directly trade between subnet tokens (e.g., SN1 → SN2), but they can do so via TAO as an intermediary (SN1 → TAO → SN2).

The TAO issuance is proportionally allocated based on the price of the subnet SN tokens. To smooth price fluctuations or prevent price manipulation, the system uses a moving average price.

The SN tokens themselves also have a relatively high issuance, with a supply cap of 21 million, similar to TAO and BTC. A portion of the SN is allocated to the TAO-SN liquidity pool, and the rest is distributed to the subnet's stakeholders (miners, validators, subnet owners). The amount of SN allocated to the TAO-SN pool is to balance the TAO issuance in the pool, keeping the price of SN (in TAO terms) stable, while also increasing liquidity.

However, if the calculations show that the subnet requires more SN than the maximum SN supply (based on the SN issuance curve), the SN issuance will be capped at the maximum, and the price of SN (in TAO terms) will then rise.

The core assumption of this mechanism is that subnets with higher market capitalization create more value for the Bittensor network, and therefore they should receive a larger share of the TAO issuance.

However, the reality is that the highest-priced tokens in the crypto market are often those with the most hype, speculation, Ponzi-like features, and marketing resources. This is why L1 blockchains and memecoins tend to have the relatively highest valuations.

While the design intent is good, the assumption that subnets generating revenue will use some of that revenue to buy back SN tokens, thereby driving up the price and earning more TAO issuance, is perhaps a bit naive.

Meme-Infested Subnets and Runaway Token Economics

Before the dTAO launch, I had discussed with some crypto analysts the obvious flaws in the dTAO token economics - that higher market cap ≠ higher revenue or greater value creation.

But I didn't expect this theoretical flaw to be validated in practice so quickly. The free market has a "wonderful" way of operating.

Just before the upgrade, an anonymous individual took over subnet 281 and turned it into a meme-coin subnet called the "TAO Accumulation Corporation" (or "LOL subnet"), which is clearly unrelated to AI.

As written on the now-deleted Github page:

Miners don't need to run any code, and validators score miners based on the amount of subnet tokens they hold. The more tokens a miner holds, the higher their issuance.

What actually happened: Speculators buy SN28 tokens → SN28 price goes up → SN28 gets more TAO issuance → If exceeding the subnet token issuance cap, SN28 price continues to rise → SN tokens are proportionally distributed to "miners" holding SN → People buy more SN to get more TAO → Price goes up further → Ponzi cycle continues.

As a result, TAO issuance is officially starting to subsidize... memes! At one point, the SN28 subnet even became the 7th largest subnet by market cap.

But why didn't SN28 take over Bittensor? Centralization saved the day

Within a few days, the Opentensor Foundation used its root stake to run custom validator code, incentivizing people to sell off SN28 tokens, causing its price to crash by 98% in a matter of hours.

Source: Bittensor discord

The SN28 subnet token crashed by 98% after the Opentensor Foundation's actions

Essentially, the Opentensor Foundation played the role of a centralized entity, preventing the free market from exploiting the dTAO mechanism. This centralized intervention is currently feasible because we are in a slow transition period from the old TAO issuance mechanism to the new dTAO mechanism.

Transitioning from the Old TAO Mechanism to dTAO

The old TAO mechanism allowed up to 64 validators who had the most TAO staked on SN0 ("root subnet") to vote on who gets the TAO issuance.

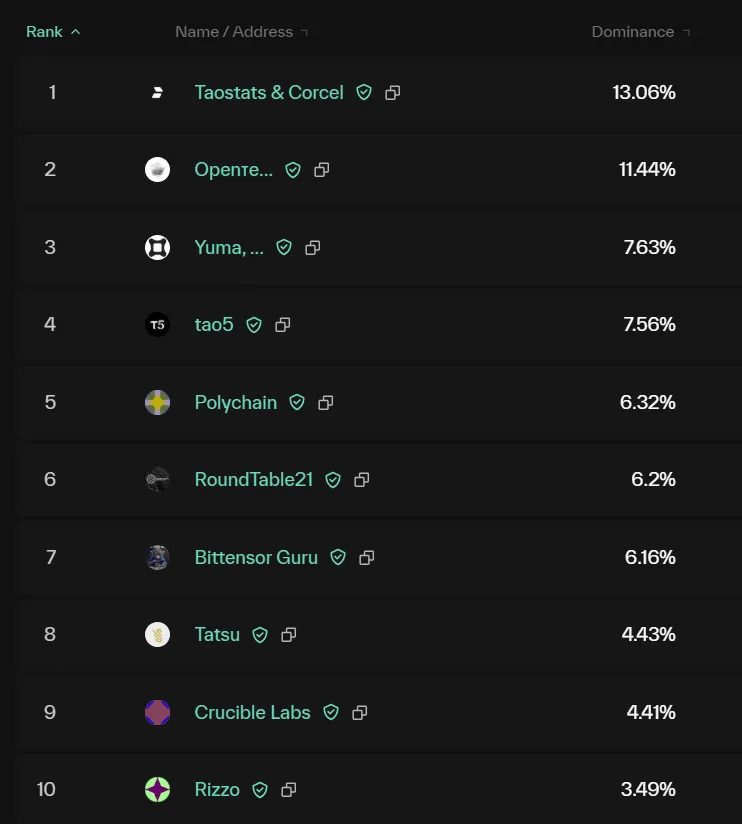

This mechanism itself raised a series of incentive issues due to the power being controlled by large validators (such as the Opentensor Foundation, DCG Yuma, Dao5, Polychain, etc.). For example, theoretically, they could direct the TAO issuance to the subnets they invest in or incubate, or to the subnets where they run validator nodes and earn TAO rewards.

Top validators shown on taostats.io/validators

Therefore, moving away from this mechanism is a good step towards decentralization. I appreciate the team's choice of a more decentralized reward mechanism, even if it means they may lose some issuance control.

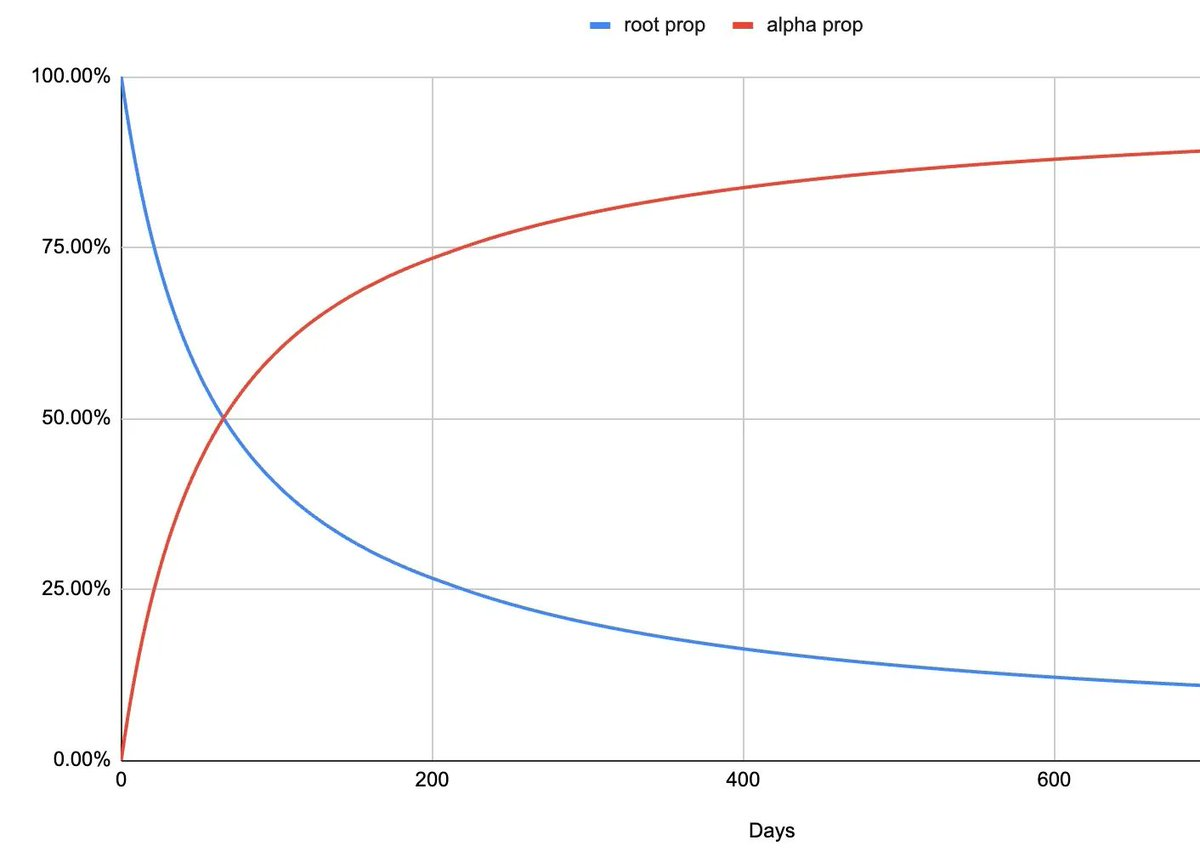

When the SN28 event occurred, dTAO had been live for about a week, so SN0 (the blue line in the chart below) still controlled around 95% of the issuance, allowing the Opentensor Foundation to intervene.

However, in about a year, SN0's control over the issuance will drop to around 20%. This means that if a similar SN28 event happens again, it will be almost impossible to intervene through SN0. In this case, Bittensor may evolve from a "decentralized AI" project into a meme-coin incentive network.

During this transition period, the power to control the emissions is shifting from the old mechanism (SN0 or "root property") to the new dTAO mechanism ("alpha property")

Admit It, This Is More Than Just Memes

Even if we assume people are rational enough during a bear market to not dive headfirst into meme-coin hype, Bittensor could still evolve into a completely AI-unrelated general incentive network.

Imagine a thought experiment: someone launches a subnet specifically for decentralized Bitcoin mining (although this is not a novel idea). The goal of this subnet is to efficiently incentivize Bitcoin mining, while using the mined BTC as a recurring revenue stream to buy back the subnet token SN, in order to earn more TAO issuance.

In this case, TAO would have transformed from a decentralized AI project into a general incentive project, where the TAO issuance is just used to subsidize various random operational expenses (OpEx) of businesses, rather than working towards a specific goal.

Technically, this could be said to be in line with the original intent of the Yuma consensus mechanism, as Yuma consensus aims to reach consensus around any "subjectivity", not necessarily limited to AI. However, this lack of a clear purpose makes the whole system seem... meaningless.

Final Thoughts

The dTAO model has been launched for only one month, and cracks have already appeared.

The incentive mechanism of the free market indicates that without any centralized force, Bittensor may no longer be an AI project, but a "attention network" dominated by meme coin subnets, or a "universal incentive network" dominated by revenue-generating enterprises that use TAO issuance to subsidize operating costs, without substantially improving the Bittensor network.

I believe the network needs a true "objective function" to unify the goals of all subnets. However, it is clearly very difficult to find a clear objective in the field of AI (especially general artificial intelligence, AGI) - as we have encountered various challenges in running a fair large language model (LLM) evaluation framework... This is also the reason why the Yuma Consensus was created to work on "subjectivity".

As the famous saying goes: "Tell me the incentive mechanism, and I will tell you the result."

Best regards!

Note

In the previous version, I had mentioned that the issuance of TAO is proportional to its market capitalization, but in fact it is proportional to the price. This error has been corrected, thanks to @nick_hotz for the correction.

Disclaimer

This article is for general information reference only and does not constitute investment advice, nor is it a recommendation or invitation to purchase or sell any investment, and should not be used as a basis for evaluating any investment decision. This article should also not be regarded as accounting, legal or tax advice or investment advice. The views expressed in the article reflect the author's current views and do not necessarily represent the views of the author's employer. The views expressed in this article may change without further notice.