Right now, RWA is truly on fire.

From the Hong Kong Web3 Carnival in early April to recent Web3 legal circles, everyone is talking about RWA. And not without reason, as RWA is a relatively reliable and safe way of "issuing tokens".

A few days ago, Mankun Lawyer discussed new RWA projects in China, such as "Mankun Research | Decoding Mainland China's Unique RWA: Practical Characteristics, Risk Analysis, and Optimization Paths", and shared current RWA practices, like "Mankun Lawyer | The Fragmented Web3 World, with at Least Three Types of RWA".

However, when it comes to RWA pioneers and leaders, we must turn our gaze to the United States. Among them, Ondo is probably the most representative. Especially in the past few days, the U.S. Securities and Exchange Commission (SEC) even met with them to discuss compliant tokenized securities issuance plans, which undoubtedly added another big "S" to Ondo's report card.

*Image source: SEC document screenshot

Therefore, in this article, Mankun Lawyer will discuss the RWA practices in the United States based on Ondo's RWA model.

Ondo RWA Model Breakdown

Mankun Lawyer believes the most important reason why Ondo is considered the RWA leading project is that while most projects were still thinking about "what real-world assets to tokenize and raise funds", Ondo had already moved U.S. Treasury bonds and money market funds onto the chain and integrated them with DeFi practices.

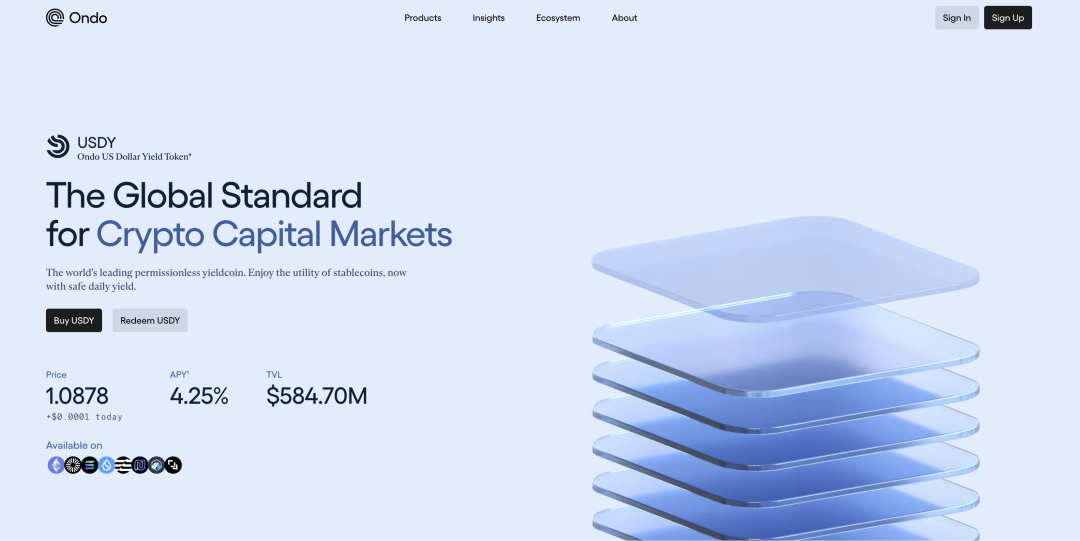

Take the USDY (Ondo US Dollar Yield Token) issued by Ondo, for example. Its underlying real-world assets are short-term U.S. Treasury bonds and bank deposits, which means:

First, the asset has real earnings support. USDY is essentially a yield-generating stablecoin, and investors can enjoy daily returns from U.S. bonds or bank deposits;

Second, transparency and safety are guaranteed. The asset's underlying logic, such as custody, audit, and revenue distribution, still follows traditional financial compliance standards.

Additionally, USDY uses a bankruptcy isolation architecture, with reserve assets completely separated from the issuing entity. In extreme situations, investors have priority claim rights to reserve assets. Besides USDY, Ondo has also issued OUSG, which is anchored to U.S. short-term Treasury bond funds, with similar logic.

Therefore, Mankun Lawyer believes that to some extent, Ondo is more like bringing traditional financial wealth management products and clearing mechanisms onto the chain, ensuring returns and risk control while giving assets on-chain liquidity.

Speaking of asset liquidity, we must mention another product by the Ondo team, Flux Finance.

If token issuance is just the first step of RWA, then how to make RWA tokens flow on the chain is the key to value-added. Thus, Flux Finance was born - a lending protocol specifically for RWA.

Unlike common lending protocols (Compound, Aave), Flux allows users to use these tokenized government bonds (like OUSG) as collateral to borrow stablecoins such as USDC.

So, the question arises: Would these 100% securities be considered non-compliant in DeFi?

Ondo's solution is a permissioned approach: Not just anyone can use OUSG for lending; they must pass a compliance review to ensure they are qualified investors. In other words, through centralized review, they avoid the disorderly state of "any asset can be used as collateral" in DeFi, ensuring that on-chain lending activities also occur within a compliant framework.

This design is tantamount to establishing a template for the overall compliance of on-chain RWA+DeFi in the future.

In fact, the RWA practice is already a closed loop at this point. But Ondo continues to expand in the RWA field - since RWA is so hot, and various projects want to do RWA, how to issue and where to circulate? There must be basic infrastructure.

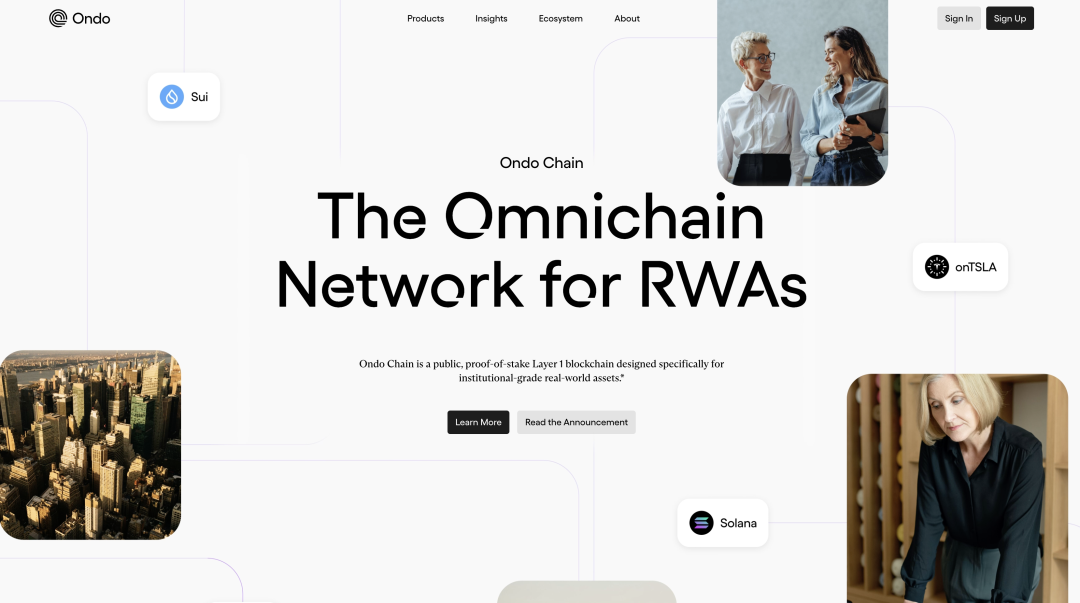

Yes, Ondo has not been idle in the infrastructure layer. They built their own Ondo Chain, specifically tailored for RWA, with core practices being:

- Permissioned validator nodes, with traditional financial institutions like Franklin Templeton and WisdomTree serving as network nodes, ensuring network security and compliance;

- Open application layer, where any developer can issue RWA tokens and create dApps;

- Built-in oracle and cross-chain bridge, with asset prices and interest rates directly fed by verification nodes.

This architecture can satisfy institutional requirements for security and regulation while ensuring Web3's native openness.

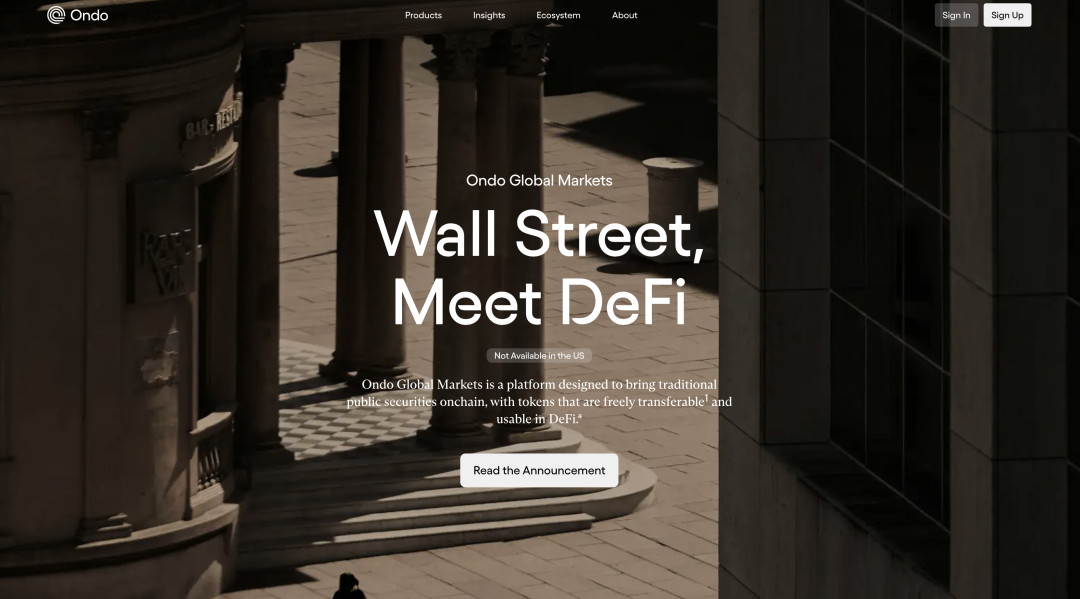

Of course, with infrastructure for token issuance, token standards must also be arranged. Thus, Ondo announced plans to build Ondo Global Markets (Ondo GM) in 2024.

Initially, Ondo GM's design was relatively traditional, following a "brokerage instruction model" where tokens represent investors' positions under traditional brokerage, overall leaning towards a permissioned and closed approach.

However, according to Ondo's blog post in February 2025, after in-depth communication with developers, TradFi institutions, and U.S. regulatory officials, Ondo GM is redesigning the tokenization framework to create RWA tokens similar to stablecoins - tokens that can flow freely, but with compliance permissions embedded in the distribution layer. This way, any token issuer can issue compliant and flexible RWA tokens through Ondo GM.

In summary, while others are still studying how to issue RWA assets, Ondo has already developed a full-chain system for smoothly bridging RWA assets from the traditional financial world to the blockchain.

Ondo and U.S. RWA

After discussing Ondo's RWA model, let's zoom out and see what problems Ondo has solved and what progress it has driven in the U.S. RWA industry.

Mankun Lawyer believes this can be approached from two perspectives:

Market Perspective

Currently in the industry, when people discuss RWA, the narrative is often stuck at "helping traditional enterprises issue tokens for fundraising". However, Mankun Lawyer believes the true value of RWA has never been just about issuing a token. For quality assets, exploring RWA is about providing higher liquidity opportunities and usage efficiency, with relatively lower barriers compared to ABS or REITS, and potentially using token programmability to find more ways to activate assets in the future.

In this regard, Ondo's design can be considered an industry standard.

Whether it's the two RWA tokens already issued or the Ondo GM being built, they are constructing a new financial market that circulates 24/7, can be minted and redeemed at any time, breaking traditional finance's "only open during working hours" rule.

Of course, circulation is just the first step. Traditional financial products can also circulate, but their liquidity is often limited to specific times and platforms, with cross-market and cross-asset practices essentially locked. Like buying gold ETFs or bond funds, these assets might be "flowing" in your account, but what can you do? At most, wait for price changes or switch platforms, with virtually no access to lending, yield, or derivative practices.

Ondo's RWA design breaks down these "walls". Especially with DeFi practices, these tokenized traditional financial assets can be pulled into various on-chain application scenarios. Simply put, it's about allowing assets that could only "earn while lying down" to be recombined and increased in value on-chain, which might be the true direction of exploring RWA's value.

Compliance Perspective

The market-level logic is actually easy to implement with technology and funds. But in the U.S. market, moving securities assets on-chain requires compliance, which is the key barrier, especially under the SEC's tight scrutiny in recent years.

Therefore, for Ondo to grow and thrive under such circumstances, the compliance aspect must have something significant to say.

First, Mankun Lawyer discovered when accessing the Ondo platform that many products cannot be used under US IP, such as token-related ones. This means that Ondo actively limits US users in product design to avoid the high-pressure regulatory area of the United States.

Of course, simply blocking US IP is not enough. Because the anchored assets come from the US market, Ondo must strictly follow US compliance standards in custody, audit, and bankruptcy isolation processes directly linked to funds, even for overseas users. Therefore, Ondo has adopted measures such as: entrusting assets to US-regulated trust institutions (like Ankura Trust), strictly conducting licensing and qualification reviews for lending, designing bankruptcy isolation mechanisms, and ensuring investors' priority claim rights.

But the question is, with overseas markets in place, what about the US market?

In 2025, Ondo collaborated with Davis Polk Law Firm to negotiate token security compliance with the SEC, resulting in the "wrapped security token" scheme mentioned by Mankun Lawyer. By embedding permission control in the distribution layer, they explore registration exemptions and market structure exemptions, attempting to find a legal landing space for tokenized securities in the US market.

In other words, Ondo is simultaneously running non-US markets using existing compliance frameworks while proactively dialoguing with US regulators to explore the possibility of RWA asset compliance in a high-pressure environment.

Mankun Lawyer's Practical Advice

After discussing all this, let's return to the most critical question: How to approach RWA in the United States?

Mankun Lawyer's advice is: Don't fantasize about instant success; avoidance + exploration, balance + step-by-step is the most realistic approach:

First, the market lacks "survival paths", not products. The US securities market is large with high-quality assets, indeed an ideal RWA pool. However, regulatory barriers are high, with "mine fields" at every step from securities law to market structure, brokers, and anti-money laundering. Although a crypto-friendly SEC chair is currently in office, no one knows which direction regulation will turn. So, prioritize non-US market landing with regulatory-compliant assets.

Second, while wanting to design more approaches, be mindful of boundaries. Especially in DeFi, although approaches are rich, US market regulators are more sensitive to complex methods. Also, stop constantly thinking about decentralization; in fact, compliance requires centralized participation, particularly in high-risk scenarios like lending and derivatives, where centralized restrictions make approaches safer and more transparent.

Third, engage more with regulators and pave the way in advance. Don't try to bypass them—you can't. With strong US market regulation, growing requires a compliance layout, including early collaboration with law firms, building an internal legal team, and proactively dialoguing with the SEC to explore compliance paths.

In summary, first dig deep market and compliance moats, then slowly find breakthrough paths—don't try to become fat in one bite.