Written by: Dong Jing, Wall Street Insights

The market's interpretation of Federal Reserve Chairman Powell's latest "hawkish" remarks may be a miscalculation. Barclays believes that what Powell really wants to do is correct the market's overconfidence that "interest rate cuts are a foregone conclusion."

Following the October FOMC meeting, the Federal Reserve Chairman stated at a press conference that inflation still faces upward pressure in the short term, employment faces downside risks, and the current situation is quite challenging. The committee remains significantly divided on whether to cut interest rates again in December, and a rate cut is not a certainty. The market interpreted this statement hawkishly, leading to a sell-off in 2-year Treasury bonds, a sharp rise in yields, and a decline in US stocks.

On October 31, according to TrendFocus, Barclays Bank issued a strong objection in its latest research report, arguing that the market panic may be a misjudgment and that Powell's real intention was not to turn hawkish, but to manage the market's overly "certain" expectations of interest rate cuts.

The bank's analyst team, led by Anshul Pradhan, believes this is a communication strategy aimed at dispelling the market's assumption that a rate cut is a foregone conclusion regardless of the data. The latest economic data shows continued slowing labor demand and underlying inflation not far from the 2% target, all of which support the Fed continuing to cut rates.

In its research report, Barclays pointed out that current market pricing is too hawkish and fails to fully reflect the risk of a significant weakening of the labor market and the possibility that the new Federal Reserve Chairman may adopt a more dovish stance.

This is not a shift in hawkish sentiment, but rather a departure from established market consensus.

Barclays noted in its report: "We believe the primary motivation is to refute the market assumption that a December rate cut is a foregone conclusion, rather than a hawkish shift in the Fed's approach to data."

In other words, the Federal Reserve wants to reiterate that its decisions are based on data, not market expectations. Powell made it clear that the Fed will respond to the slowdown in labor demand, which is precisely what is happening now.

The report emphasizes that the latest economic data not only does not support a hawkish stance, but also provides a basis for further interest rate cuts.

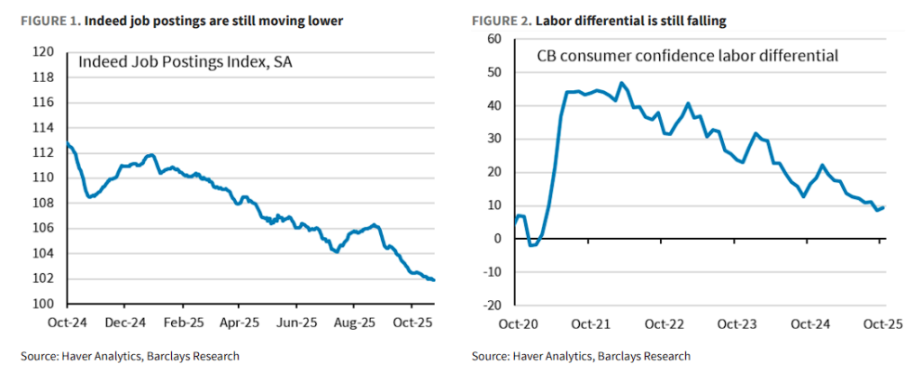

In the labor market, leading indicators, including Indeed job postings and the labor gap (jobs plentiful vs hard to get), suggest that demand is slowing.

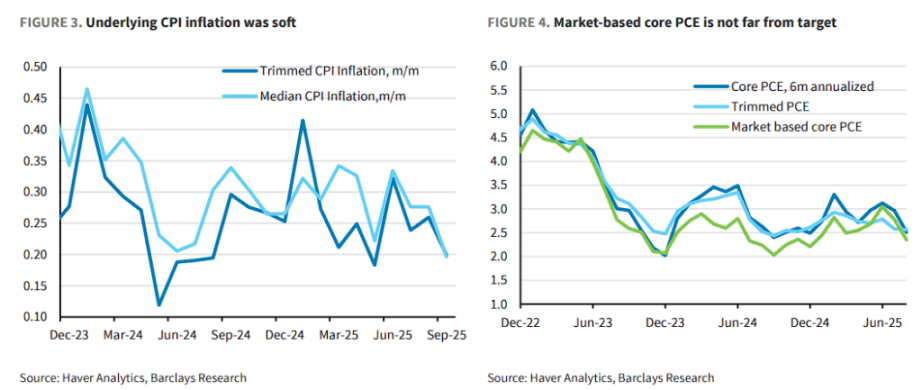

Regarding inflation, Powell also acknowledged recent weak data. Core inflation indicators have shown a downward trend. Barclays analysis suggests that once the impact of tariffs is removed, market-based core PCE inflation is close to the 2% target.

"Overall, if underlying inflation is only a few tenths of a percentage point above the target and the unemployment rate is only a few tenths of a percentage point above the natural rate of unemployment (NAIRU), then the policy setting should be neutral."

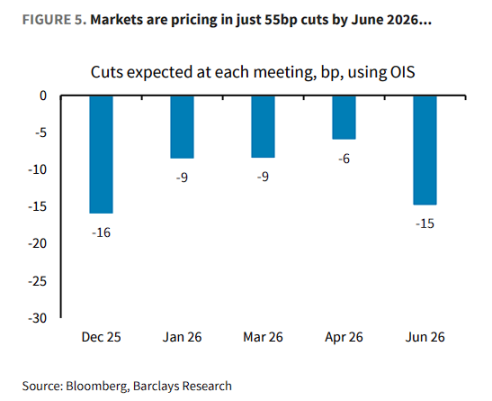

This means that, given the current data context, restrictive monetary policy is no longer necessary. Barclays observes that the market is currently pricing in only a cumulative 55 basis point rate cuts by June 2026, a view that is "too one-sided."

Current market expectations are for only a 35 basis point rate cut by March 2026 and only a 55 basis point cut to 3.3% by June. Implied distribution in the options market shows a divergence of opinion regarding the number of rate cuts in March and June, with the modal expectation being only one rate cut by June.