I saw a news report today : Polygon laid off about 30% of its employees.

Although Polygon has not issued an official statement in response, CEO Marc Boiron acknowledged the layoffs in an interview, while saying that the total number of employees would remain stable due to the addition of newly acquired teams.

The posts from laid-off employees on social media indirectly confirm this fact.

But in the same week, Polygon announced it would acquire two companies for $250 million. Isn't it a bit strange to be laying off employees while simultaneously spending a lot of money?

If it were simply a contraction, they wouldn't simultaneously spend 250 million on acquisitions. If it were an expansion, they wouldn't cut 30% of the staff. Looking at the two together, it seems more like a complete overhaul.

The layoffs were made up of people from the original business lines, and the positions were given to the acquired teams.

The 250 million yuan was spent on licenses and payment channels.

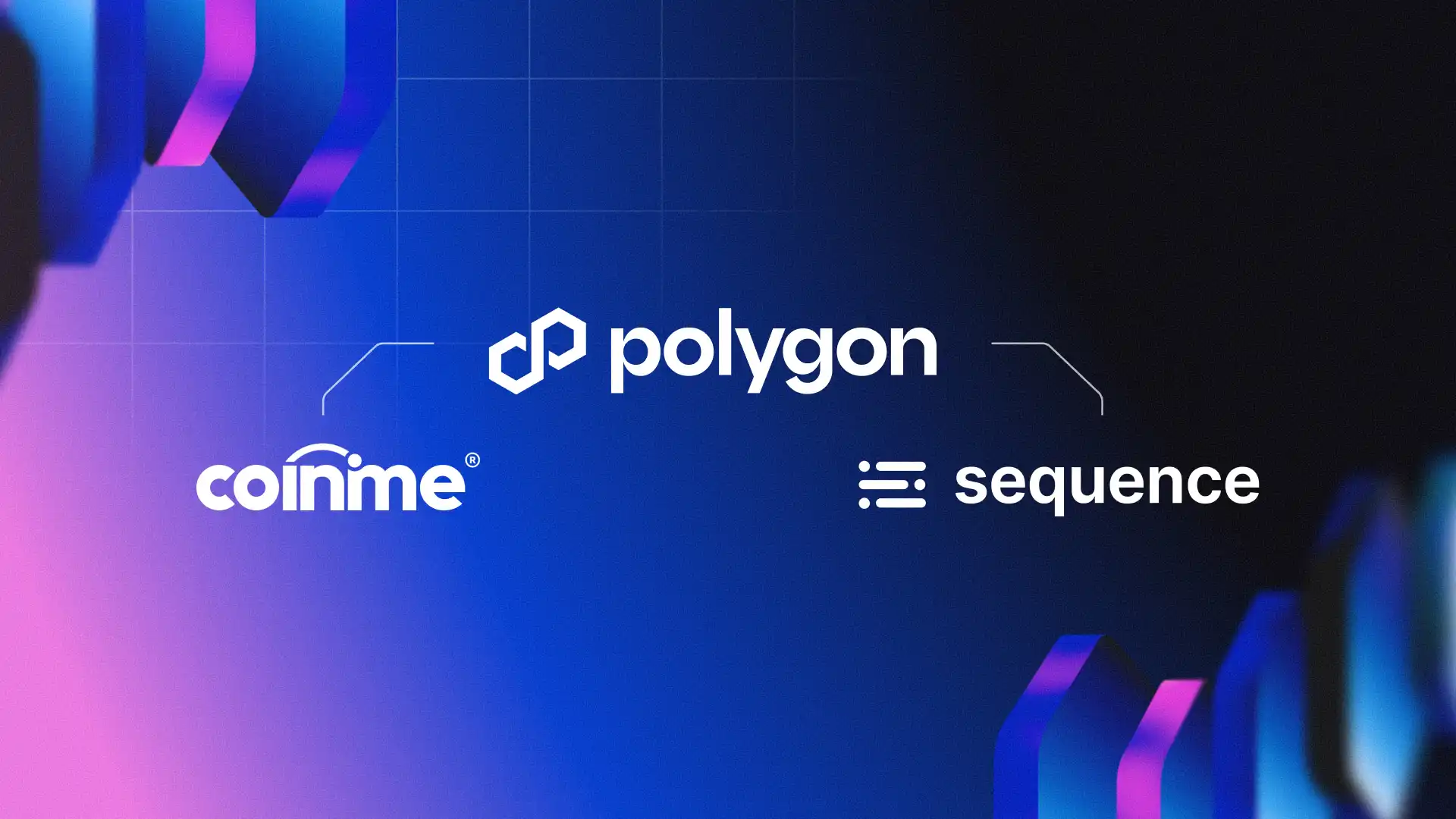

The two companies that were acquired were Coinme and Sequence.

Coinme, founded in 2014, is an established company that acts as a gateway between fiat currency and cryptocurrency, operating crypto ATMs at over 50,000 retail locations across the United States. Its most valuable asset is its licenses, holding money transfer licenses in 48 states. These are extremely difficult to obtain in the US; companies like PayPal and Stripe spent years acquiring them.

Sequence provides wallet infrastructure and cross-chain routing. Simply put, it allows users to transfer funds across chains with a single click, eliminating the hassle of bridging and gas switching. Its clients include chains like Polygon, Immutable, and Arbitrum, and it also has a distribution partnership with Google Cloud.

The two acquisitions totaled $250 million. Polygon named this system "Open Money Stack," positioning it as a middleware for stablecoin payments, and intended to sell it to B2B clients such as banks, payment companies, and remittance merchants.

My understanding of the logic is as follows:

Coinme provides compliant fiat currency deposit and withdrawal channels, Sequence offers a user-friendly wallet and cross-chain capabilities, and Polygon's own blockchain provides the settlement layer. Together, these three form a **complete stablecoin payment infrastructure**.

The question is, why would Polygon do this?

Polygon is finding it very difficult to navigate the L2 road.

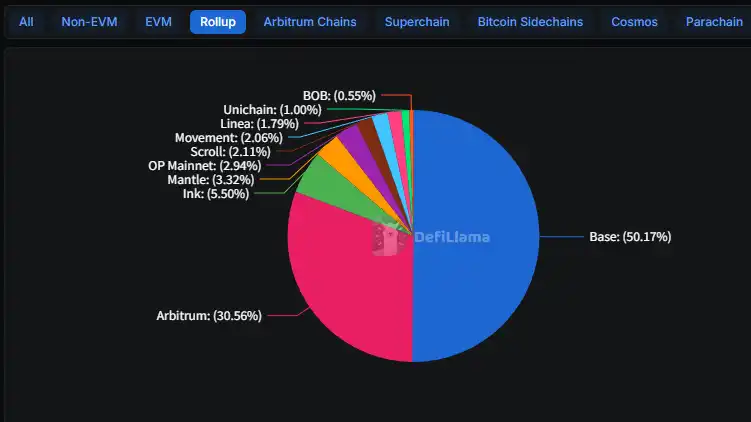

The situation in 2025 is clear: Base has won.

Coinbase's L2 pipeline saw its TVL (TVL) rise from $3.1 billion at the beginning of last year to $5.6 billion, accounting for 50% of the entire L2 pipeline market. Arbitrum maintained its 30% share but saw virtually no growth. The remaining dozens of L2 pipelines were largely abandoned after their airdrops.

What makes Coinbase a winner? Coinbase has hundreds of millions of registered users, so when any product or feature is launched, users naturally come.

For example, the Morpho lending protocol's deposits on Coinbase have increased from $354 million at the beginning of last year to $2 billion now. The main reason is that it has been integrated into the Coinbase app. Users can use it simply by opening the app; they don't need to know what L2 or Morpho is.

Polygon doesn't have this kind of entry point. It also laid off 20% of its staff in 2024; that was during a bear market contraction when everyone was cutting jobs.

This time it's different. They have money in the account but are still cutting jobs, which means they're actively choosing to change direction.

I remember that Polygon used to tell stories about enterprise adoption, such as accelerators with Disney, Starbucks' NFT membership program, Instagram casting on Meta, Reddit avatars, and so on.

Four years have passed, and most of those collaborations have fallen silent. Starbucks' Odyssey project also shut down last year.

In the L2 arena, Polygon has virtually no chance of winning against Base. The technological gap can be closed, but the user entry point cannot. Rather than wasting time in a battle it can't win, it's better to look for new opportunities.

Stablecoin payments are a good direction, but they're very crowded.

Stablecoin payments are indeed a market that is rising.

In 2025, the total market capitalization of stablecoins exceeded $300 billion, 45% more than the previous year. Their uses are also changing, expanding from mainly arbitrage between trading platforms to scenarios such as cross-border payments, corporate finance, and payroll.

But this market is already very crowded.

Stripe spent $1.1 billion last year to acquire stablecoin infrastructure company Bridge, and recently acquired the rights to issue the USDH stablecoin on Hyperliquid. PayPal's PYUSD already accounts for 7% of the stablecoin market share on Solana.

Circle is promoting its own Payments Network. Major banks like JPMorgan Chase, Wells Fargo, and Bank of America are forming an alliance to launch their own stablecoins.

In an interview with Fortune, Polygon founder Sandeep Nailwal said that the acquisition puts Polygon and Stripe in competition.

To be honest, that's a bit of an overstatement.

Stripe spent $1.1 billion to acquire Polygon, while Polygon spent $250 million. Stripe has millions of merchants, while Polygon's clients are mainly developers. Most importantly, Stripe has accumulated over a decade of payment licenses and banking relationships.

In a head-on confrontation, they are not even in the same league.

But Polygon may be betting on a different strategy. Stripe wants to integrate stablecoins into its closed loop, allowing merchants to still use Stripe, but with the settlement layer replaced by stablecoins for faster and cheaper transactions.

Polygon aims to create an open infrastructure that allows any bank or payment company to build its own business on top of it.

One is vertical integration, and the other is horizontal entry. These two models may not directly compete, but they are vying for the attention of the same group of customers.

A different way of life, the future is uncertain.

Finally, it's not uncommon for the crypto industry to lay off employees in the past two years.

OpenSea cut 50% of its workforce, and Yuga Labs and Chainalysis are also downsizing. ConsenSys laid off 20% last year and is doing so again this year. Most of these downsizings are involuntary; they're short of cash and just trying to survive.

Polygon is different. They have money in their accounts and can even come up with $250 million for acquisitions, but they still chose to lay off 30% of their staff.

A blood transfusion can change your way of life, but it also carries risks.

Coinme, which was acquired by Polygon, had a core business of crypto ATMs, with machines deployed at more than 50,000 retail locations across the United States, allowing users to buy crypto with cash and exchange crypto for cash.

The problem is that this business ran into trouble last year.

California regulators fined Coinme $300,000 for allowing ATMs to allow users to withdraw more than the daily limit of $1,000. Washington state went even further, issuing a ban that was only lifted last December.

Polygon's CEO once said that Coinme's compliance "exceeded requirements." But regulatory penalties are in black and white, and empty words cannot change that.

When these events are mapped onto the token, the narrative of the $POL token changes.

Previously, the more the blockchain was used, the more valuable POL became. After the acquisition, Coinme takes a commission on every transaction, which is real revenue, not just tokenized revenue. The official estimate is that this will generate over $100 million annually.

If this can be achieved, Polygon could transform from a "protocol" into a "company," with revenue, profit, and a valuation anchor. This is a rare species in the crypto industry.

However, the pace of traditional financial institutions entering the market is clearly accelerating, and the window of opportunity for crypto-native companies is narrowing.

There's a saying in the industry: build during a bear market, reap during a bull market.

The problem with Polygon now is that it's still under construction, but it may no longer be the bull market harvester.