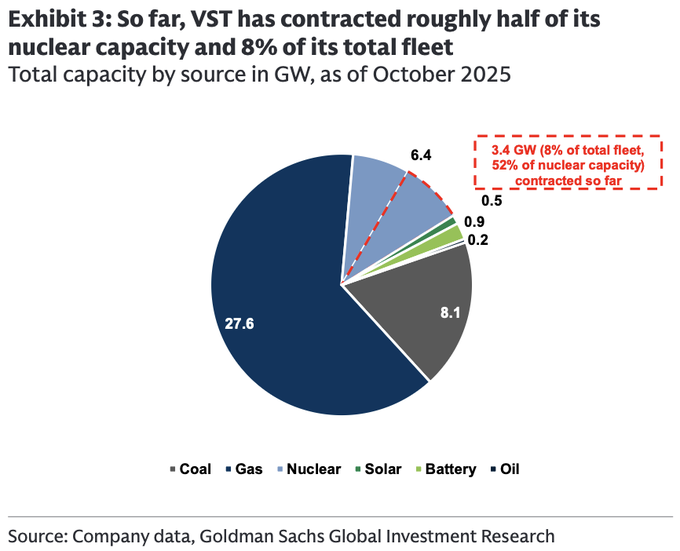

Goldman on $VST "We upgrade Vistra from Neutral to Buy after incorporating the Meta PPA into our numbers and following the pullback in shares" "potential upside of 3-9% to our 2028 EBITDA if Vistra contracts the rest of its nuclear generation in a similar price range" "Vistra has contracted roughly half of its nuclear fleet through PPAs. However, it still has a sizeable ~3.1 GW left to contract: 1,872 MW from units I and II of its Beaver Valley facility in PA and 1,200 MW from the remaining Comanche Peak unit. We estimate an additional 3-9% impact on 2028 EBITDA (Exhibit 2) if the remaining nuclear fleet gets contracted, assuming an $85-$100/MWh range for PPA power price"

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share