This article is machine translated

Show original

Early this morning, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly released a document with significant implications for the future regulation of crypto.

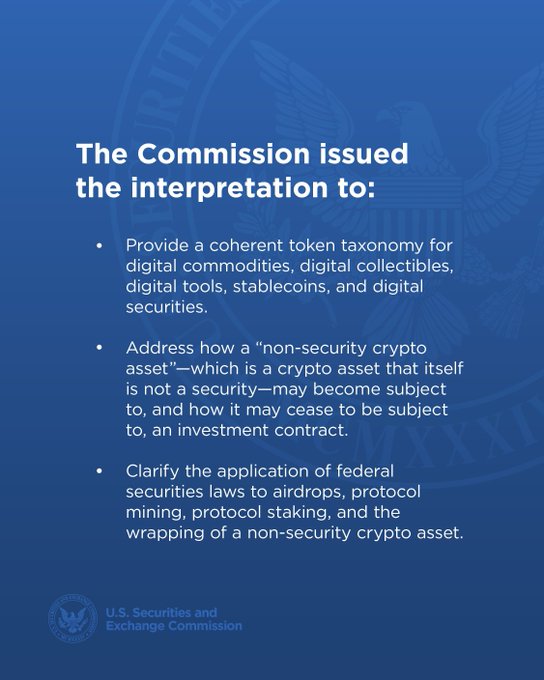

A quick look at the document reveals that this document categorizes crypto assets into five types:

1/ Digital Commodities

◦ These are assets closely tied to the programmatic operation of a functional cryptographic system. Their value is determined by supply and demand and the system's operation, not by anticipated profits generated from the managerial efforts of others.

◦ They are not securities ❌ and are regulated by the CFTC.

◦ Their characteristics are:

1) No intrinsic economic rights: They do not generate passive income, nor do they grant holders ownership of the future revenue, profits, or assets of a commercial entity;

2) System necessity: They are essential for participating in or using the relevant cryptographic system, such as as gas fees for transactions;

3) Functional purpose: They are used to incentivize transaction verification, maintain network security, promote network effects, or participate in system governance.

Typical examples include: BTC, ETH, APT, AVAX, BCH, ADA, LINK, DOGE, LTC, DOT, SHIB, SOL, XRP, and other public blockchain tokens.

2/ Digital Collectibles

◦ These are crypto assets designed for collection or use, such as NFTs (Non-Finite Tokens) like artwork, music, videos, sports cards, and game items, or meme coins and characters.

◦ Characteristics: No economic attributes; no passive income generation; value is primarily driven by supply and demand.

◦ Generally not considered a security ❌, regulated by the CFTC. An exception is if NFTs are fragmented and assigned rights, which may constitute "relying on the administrative efforts of others to generate profits" and be classified as securities.

3/ Digital Tools

◦ These are crypto assets that perform practical functions. Their value does not derive from investment expectations but from the practical functionality they provide.

◦ Not considered a security ❌, regulated by the CFTC.

◦ Characteristics: Function-oriented, such as membership, conference tickets, ownership certificates, etc. (possibly manifested as NFTs); even non-transferable; does not generate income or economic rights. For example, ENS identity domains.

4/ Stablecoins

◦ Are crypto assets that maintain a stable value relative to underlying assets such as the US dollar.

◦ Compliant stablecoins issued by "approved issuers" are not securities ❌, and are regulated by federal payment stablecoin regulators; an exception is whether they involve profit expectations or dividends to determine if they meet the definition of securities.

◦ Characteristics: Primarily used for payment or settlement; under the GENIUS Act, compliant issuers are prohibited from paying any interest or income to holders.

5/ Digital Securities

◦ Are financial instruments within the legally defined scope of "securities," but represented by crypto. Their ownership records are maintained, in whole or in part, on the blockchain.

◦ Are securities ✅, requiring registration with the SEC and regulated by the SEC.

The key features are: stablecoins can be issued natively on-chain or are tokenized versions of traditional securities; for tokenized stablecoins, the rights of the holders (such as voting rights) may differ from those of the underlying securities; they may also possess functions similar to digital commodities without altering their security attributes.

Previously, market participants had long criticized the SEC for its enforcement-style regulation, lacking a clear regulatory framework and hindering innovation in the crypto industry. Starting in 2025, the new SEC Chairman, Paul S. Atkins, announced the launch of Project Crypto; subsequently, the US passed the GENIUS Act, providing a legal framework for stablecoins.

The classification guidelines released today, compared to what Michael Saylor mentioned in a previous interview (x.com/Sea_Bitcoin/status/19327...…)分类更细,更有操作性。也标志着加密货币监管从「不透明的强力执法」转向「可预测的规则框架」。), mean that for project teams, a clearer classification translates to greater room for innovation, allowing them to work more freely and significantly reduce costs; for individual investors, it provides clearer information about the corresponding risks and regulations for their assets and projects. Those interested can view the full PDF file: sec.gov/files/rules/interp/202...…

SΞA

@Sea_Bitcoin

08-01

凌晨,4 月上任的新 SEC 主席 Paul S. Atkins 宣布了一个叫 Project Crypto 的计划。

核心是让更多金融活动能够迁移到链上,去掉过度监管,大力鼓励创新。

我认为其对市场的长期影响力不压于稳定币法案 (GENIUS Act)。

以下是对这个计划核心内容的整理和简单解读 ——

◦

Meme coins are categorized as digital collectibles, but Doge and Shib are categorized as digital commodities.

Why? Because Doge is a PoW public chain coin, and while Shib issued an L2 token, it wasn't widely used.

This indicates that in the eyes of US regulators, Doge and Shib no longer belong to the meme coin category. The current leading meme coin is $PEPE

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content