I still remember the days when the bull market took off in 2021. The most mentioned name, besides Cathie Wood Wood, was Buffett. Of course, in the cryptocurrency industry, Buffett is more often scolded for his negative remarks. At the craziest time, people regarded ARK's Cathie Wood as a god, and looked down upon Buffett, thinking that he had failed to keep up with the times and could not understand new things. At that time, any child's income from Tesla in the US stock market could make I muttered to myself that Buffett was nothing more than that, let alone the exaggerated fluctuations of Altcoin.

How exaggerated were the market sentiments at that time? An internet celebrity's self-made "Warren Buffett's handwritten resignation letter" was actually published by major mainstream technology media without verification. People at that time were too willing to believe that the stock god was old and the new world had its own logic.

But when the bubble burst, liquidity tightened, and after the disaster, we looked at Cathie Wood's earnings and had retraced more than 60%, while Grandpa Buffett was still frighteningly stable. In the secondary market, retracement is the last thing that players want to happen. What can the stability of this god give us?

The emergence of price investing

If Benjamin Graham in the 1930s puts on the latest popular Apple Watch at the end of 2022 and opens the CeFi or DeFi platform for cryptocurrency trading, he may frown and smile. Don’t panic, I know this question.

In the United States in the 1920s, the stock market was far less mature than the bond market and was an emerging niche market. There are few investors in this market, mostly traders. There are professionals and ordinary people among traders. "Economists" are very popular, and "leeks" are also chasing the comments of star fund managers. There was no value investing at that time, and everyone's trading methods were basically "technical", looking at the trend and chasing the rising trend. Graham, who entered the financial market very early, became very comfortable in this market by analyzing company financial reports, and soon became a big V and star manager. The fund he managed once made a profit of over 100%, and the market value of the fund increased by 66% in 3 years. times.

In the Roaring Twenties, Gatsby was fascinated by Daisy, while many people relied on the myth of the stock market, hoping to become rich overnight.

Beginning on October 24, 1929, the U.S. stock market began to plummet, ushering in the infamous Great Depression, and even big V companies were not immune. The net worth of Irving Fisher and Graham shrank greatly. Although Graham's fund only lost 70% when the market lost 74%, this could not save his wealth that evaporated in a few days. Graham dismissed the servants from his New York mansion, divorced and remarried again, and lived through a relatively chaotic period. Afterwards, Graham learned from the painful experience, organized his value investment philosophy while teaching at Columbia University, and published "Securities Analysis", officially opening the era of value investment.

For more than half a century, Graham's disciple Buffett and others used the theory of value investing to invest, creating a generation of investment masters.

The stock market at that time was similar to today's currency market in some senses, so can the value investment used for stock analysis also be used to look at currencies?

Value investing is very simple, but the world is too complicated

Graham's value investing is very simple, and Buffett also follows the simplicity of the theory in his operations, often performing calculation exercises (napkin valuation) behind a napkin. Buffett himself has never done investment modeling and various sensitivity analyses, which can take several pages. When it comes to asset pricing and stock price arguments, the operation of the stock god has always been as simple as water.

The price investment calculation given by "Securities Analysis" is: V = EPS * [8.5 + (2*g)].

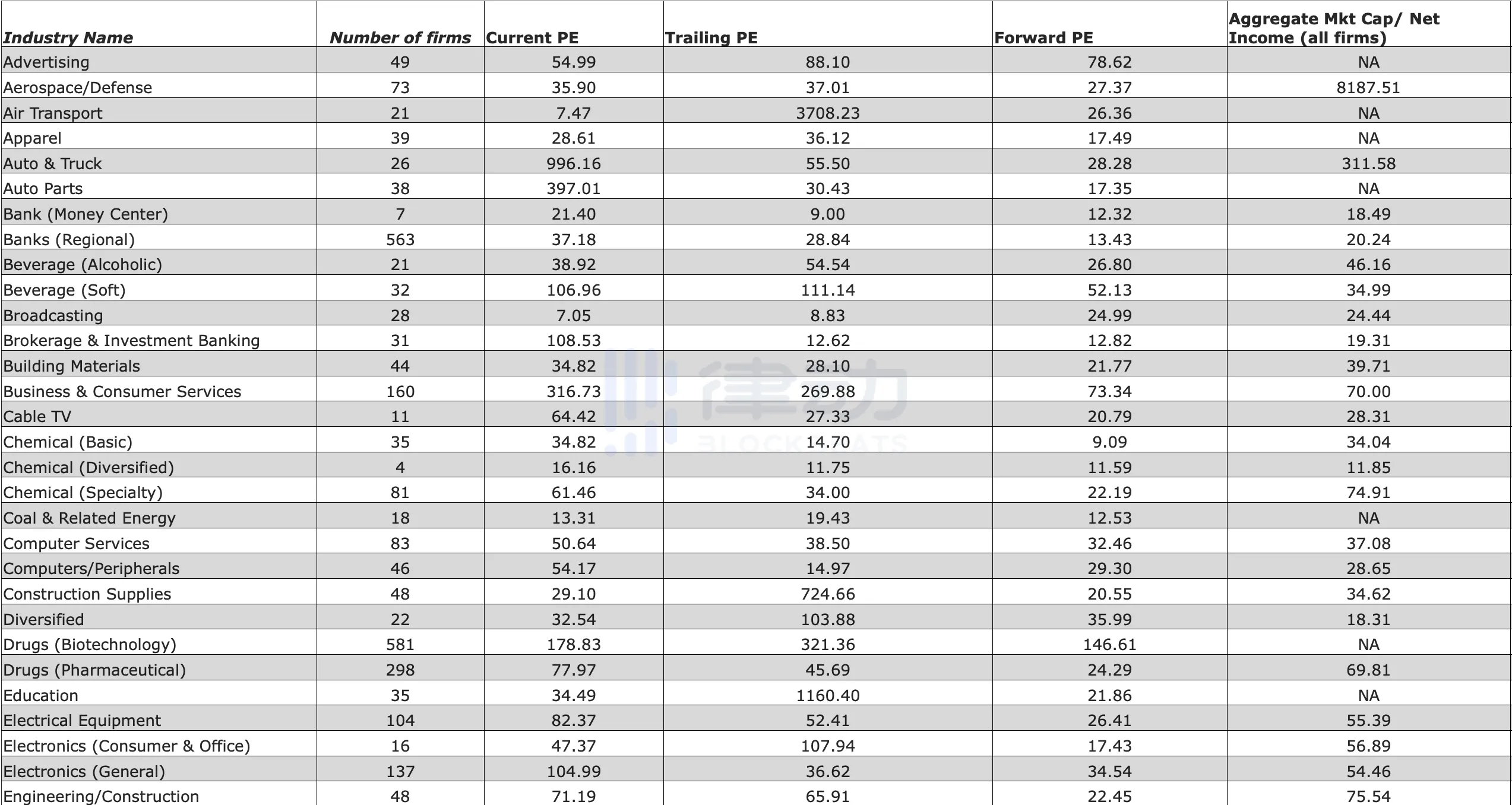

At that time, Graham's PE used 8.5, which was applicable to the PE value of companies with no growth rate in the era when the book was written. Later, it evolved and PE generally used the company value. There are not many reference company indicators for emerging companies. Aswath Damodaran, a well-known professor at New York University, has a list of roughly emerging industry PEs. This price investment calculation has also changed slightly.

The concept and practice of value investing have traveled through time with a generation of value investing masters, and based on ten years, it has become an iron rod that transcends bulls and bears. However, before the U.S. stock market plummeted in 2020, price investment investors had been squeezed by funds that advocated investing in emerging technology companies for a period of time, and their returns were far lower than those of growth funds. One of the most high-profile funds at the time, Cathie Wood’s ARK, and the rise of Tesla, one of the stocks with the highest returns at the time, used underlying logic that was very different from price investing. Many technology stocks in our era are not profitable before and after listing, with PEs of dozens or even hundreds of times, but this does not prevent these companies and stocks from explosive growth. The core logic of ARK is to invest heavily in technology stocks with explosive growth. In the era of technological explosion, such funds have indeed achieved extraordinary results in a short period of time. Companies with exponential growth are not within the margin of safety for value investment funds, so value investors may not look at such companies at all.

Even in China, Zhang Lei of Hillhouse, who advocates value investing, studied under Yale David Swenson. He did not completely follow the classic price investment operation. Instead, he re-expressed his views on "value" and believed that as long as it is "value", no matter how expensive the price is, You can also buy it, so Hillhouse has previously invested heavily in high-growth stocks such as Bilibili and Pinduoduo, which are not within the safety margin and have negative profits every year. At the same time, Zhang Lei emphasized that preliminary research is very important, which is somewhat similar to Li Lu, another person who insists on venture capital on the other side of the Taiwan Strait.

This feeling is similar to the logic of investing in Amazon twenty years ago. Amazon’s stock rose every year before the collapse of dot.com, so it was not a bad investment, although it did not turn a profit for the first time until 7 years after its founding. , and profitability is very weak.

By contrast, Buffett's position in the company has remained consistent for decades. Several stocks that Buffett outperformed the market: Coca-Cola in the 1980s, Apple in 2016, and TSMC in 2022, all have the following characteristics: low PE in comparison, industry leader, huge profits, safety margin, and good Dividends.

For the stock gods, there is nothing outstanding about buying and selling stocks. The most important thing is to have a high-quality business with long-term profits. Stock gods usually have cash in hand and believe that crisis is an opportunity. If there is no cash to purchase high-quality assets at the right time, it is tantamount to investment failure.

Buffett is not against technology, but whether technology can match his indicators. Apple, managed by the stock god, is one of the investment classics. In 2021, Berkshire Hathaway invested in Brazilian FinTech disruptor bank Nu Bank, and Nu Bank plans to launch its own cryptocurrency in 2023.

Buffett and his partner Munger openly scorned cryptocurrencies, believing that there is no actual value behind the assets, although the stock god is not opposed to the technology and logic of blockchain.

Since the top price investment practitioners of our era do not recognize the crypto market, is it possible that the concepts and operations of price investment can still be applied to cryptocurrency project analysis?

Defining cryptocurrencies is hard, and so is pricing

First of all, it may be important to define the investment object before investing, because only in this way can we know what kind of properties and laws the investment object has.

Which asset class a cryptocurrency should belong to is something that regulators, investors, and users have yet to figure out, or maybe it should have its own asset class. In the eyes of regulators, led by the Bank for International Settlements and major central banks, cryptocurrency is called "cryptoasset" (cryptoasset), so central government mothers and financial fathers do not recognize the existence of cryptocurrency as a circulating currency. The arrival risks of cryptocurrency do make it unable to meet some of the most basic requirements of currencies. This is not only reflected in the documents issued by the central government, but also in the government’s definition of cryptocurrency. For example, documents filed by the US SEC against FTX show that the SEC believes that FTT should actually be regarded as a security through its earlier buy and burn activities. If FTT is defined as a security, then BNB may have similar properties. Securities are subject to SEC regulation, while commodity contracts are not. Currently, the United States has adopted a legal Commodity Exchange Act that defines virtual currencies such as Bitcoin and Ethereum as commodities.

Cryptocurrencies do have commodity properties and also have foreign exchange market properties. Trading prices in commodity and foreign exchange markets are determined by supply and demand for the asset. Similar to commodities, the price of commodities is the unit expression of a certain raw material (gold, oil, etc.) and has a one-to-one relationship. Each token of a cryptocurrency is also a unique expression of a certain value. Both commodities and token transactions need to be conducted in pairs, and are currently cyclical. Moreover, in the context of high inflation, bulk and cryptocurrencies are considered by investors to be anti-inflation in a sense. Cryptocurrencies, which currently exist as commodities, are also relatively loosely regulated. If cryptocurrency is defined as a security, cryptocurrency needs to provide more transparent financial reports so that its price rise and fall can truly reflect the value expected by investors.

Even so, cryptocurrency cannot be strictly called "electronic gold", although the rise and fall of cryptocurrency is not entirely consistent with the similar movements of commodities from time to time. Some scholars (Lawuobahsumo et al., 2022) claim that this correlation is very It may be the spillover effect of other environmental factors in the market.

So as a currency, can cryptocurrency "currency" use FOREX logic?

After all, the core logic of cryptocurrency from its inception is to theoretically solve the lag of centralized currencies, make transactions faster, more convenient, and resist inflation. Later, various encrypted "currencies" appeared, although many of them did not have the attributes of circulating currencies and were more like "stocks" of a company or project. Just like the legal currency itself, to some extent, it is also the value of national sovereignty. Reflection, although national debt would be a better analogy.

However, after comparison, some scholars (Liang et al., 2019) found that the current encryption market is more similar to the stock market and not very similar to the FOREX market, except that both are traded 24 hours a day. This is easier to understand. After all, the transactions in FOREX are all national legal currencies and legal currency derivatives. Each legal currency is essentially a liquid tool for trade in a certain country and region. On the contrary, the actual uses behind each cryptocurrency are different.

Based on this, can we say that cryptocurrencies are more suitable for analysis by the logic used to analyze securities, because we can see with the naked eye a very high correlation between cryptocurrencies and US stocks. But but but, Isah and Raheem (2019) pointed out that the underlying logic of this correlation is the release of water (QE) from the US central bank, so the water for the rise and fall of the stock market and crypto market comes from the tightening of the US dollar.

At this point, the author believes that although cryptocurrencies have some characteristics of bulk, foreign exchange, and US stocks (note that US stocks are not other stocks), they cannot be simply attributed to one group. If it must be attributed, it has the greatest correlation with the US stock market and is deeply affected by macroeconomic policies. When there is no way to quantify the financial reports of crypto projects, it may not necessarily be possible to use micro value investing, but is more suitable for following up on macro operations. Therefore, price investing is unlikely to be used in the crypto market.

Asset Pricing in Crypto: What can you do if you can’t do price investing?

It is very difficult to do price investment research on cryptocurrency. First, there is no mature quantitative system. Currently, no major player has provided a calculation tool that can model it. Second, cryptocurrency data is also worrying. Unlike financial reports in the U.S. stock market, which generally cannot be falsified, people can trust the financial data provided by the company, and the rest of the things that are not on the report can be traced, but in crypto Currency, 6 million users may be just a boast, and the actual ARPU per user is only known by the company itself.

If there is no reliable hard data to measure specific projects, how can calculations and value investments be made?

At present, some scholars have given some hard indicators for asset pricing modeling for your reference.

Hubrich (2017) applied the French-Fama model to cryptocurrency, using only 3 attributions. Scholars use the currency's market value, trading volume, and market value/trading volume as indicators to measure the market, and use the "spillover" effect of per-coin inflation to measure the relationship between attributions (i.e., the conversion rate of each coin mined, carry). Wait, the final conclusion is that the biggest reason for the project's performance is the market, which has a little relationship with the currency (carry), and the alpha is extremely small.

EY has also issued a report stating that CAPM and others can be used by cryptocurrency valuation portfolios, but it did not give detailed guidance on how to use it.

The author is very interested in this topic, and readers who are interested in modeling or doing related work are welcome to contact the author. If we can develop some asset pricing systems for cryptocurrency, whether it is price investment style or French-Fama style, it will be of great benefit.

Why value investing (in cryptocurrencies)?

Graham proposed value investing, but he himself was not a master of value investing. Although the rewards are not bad, he just has too many other interests and hobbies. He even participated in the drafting of the Bretton Woods system and considered his achievements in monetary theory to be his most awesome contribution. In the following decades, as the U.S. stock market gradually matured, Buffett, who had a relatively simple hobby and only liked investing and making money, put this theory into practice.

In Graham's system, net is the core, which means that worthy stocks must be bought cheaply and in groups. If they go up, they will rise a lot, and if they fall, they will not fall much. Then, we can grasp the two points of price investment: safety margin + high value and low valuation. Based on this, although there are many excellent assets, Buffett may not invest in them because they are expensive. In 2020, Buffett repeatedly stated that he did not intend to invest because the projects on the market at that time were too expensive. When everyone is at their wits' end, the stock gods with strong cash flow will start buying stocks.

But you may think this is a bug. "Cheap" is a relative term. US$600 is expensive compared to US$100, but US$60,000, which has increased in relative valuation, is very cheap. I believe it is absolutely cheap. Not relatively cheap. When Buffett invested in Apple, its average cost was about $37, and today's Apple is already over $100.

Transferring these principles to cryptocurrency "investment", the author believes that we can learn some feelings. That is to say, don't usually follow the market's rise and fall. Don't chase the market when it's high. When the project is relatively small, buy some stocks that are already generating positive cash flow in a diversified manner without adding leverage. Technology may not necessarily work, because you are not buying explosive technology based on logic. You must check whether there are positive funds, and this is a difficult point. Specifically, you may want to check whether gas/arpu+ users are a profitable business. Even if it falls, it won’t fall much. When the market rises, it will naturally increase the value of the currency in hand. In a bear market, buy a few more coins, but you should also keep enough cash. Meme coins don’t touch. Don't short.

We don’t know if cryptocurrencies will continue to mature like the stock market or if they will one day cease to exist. And the above summary only supports friends who want to uphold the belief in price investment in cryptocurrency. It is not just words, but actually abiding by the core logic of price investment.

At least Buffett has used his investment career to prove that price investing is still an evergreen tree. Although ARK reached a 152% return in 2020, Tesla also reached a 695% return at its peak. By 2022, ARK's retracement reached 65%. Berkshire Hathaway's retracement due to stock declines in 2020 was only 19%. It continued to be brilliant in the next two years. In 2020, it held approximately US$48 billion in cash and swept the world. By 2022, Berkshire Hathaway's stock price fell by 19%. Servi's stock price reached a new high. This is the closest operation to us by the stock god. In fact, Buffett's operations are the same every ten years. Stock gods tell everyone time and time again, buy cheaper, buy good companies, hold on to it, and don’t do messy operations. But everyone thinks this method is too simple, so simple that without trade, it does not reflect the complexity of finance and the understanding of the market. understand.