Two figures are pointing to the direction of the current crypto market.

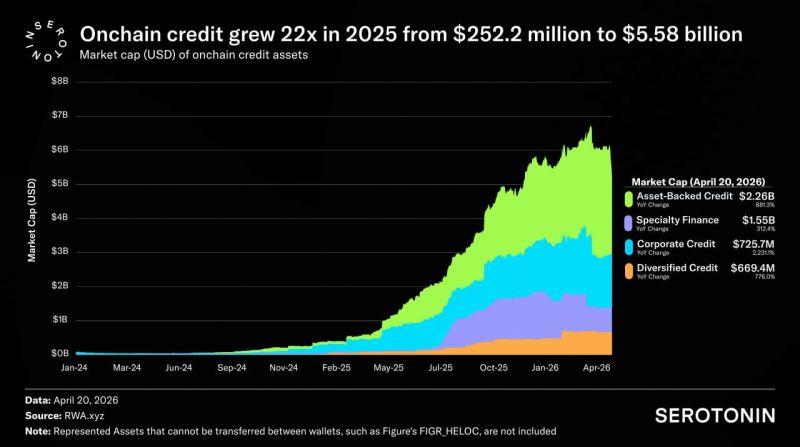

Monthly crypto card payments reached $600 million. The on-chain credit market reached $5.58 billion. One indicator shows how quickly consumers are using blockchain assets to purchase physical goods, while the other shows how quickly dormant stablecoins on the blockchain are transforming into a source of credit for the real economy. These two flows are moving in the same direction. We are now at a turning point where stablecoins are transitioning from speculative tools to operational financial infrastructure.

Encrypted cards: 500% growth within two years

Back in early 2023, monthly payments for crypto cards were virtually zero. Starting in September 2024, the curve changed. In the following eight months, payments surged by over 500%, exceeding $600 million per month by March 2026. By blockchain, TRON and BSC held a significant share, followed closely by Ethereum, Solana, Base, and Arbitrum.

The key is that Visa controls 90% of this market share. Visa's strategy is clear: reduce reliance on traditional card issuers and instead establish direct partnerships with emerging blockchain infrastructure providers. Payment networks are reshaping themselves by integrating with stablecoins.

The most notable recent example is Jupiter Global. This service offers crypto card users 4% to 10% cashback, and transaction volume in April increased by over 660% month-over-month. This marks the moment when traditional financial card rewards structures are being migrated to the blockchain. For consumers, the disadvantages of crypto cards compared to traditional credit cards are disappearing.

An empirical study published by the International Monetary Fund (IMF) in March 2026 (WP/26/52) indicates that the total market capitalization of companies focused on cross-border payments declined by approximately 27% after the passage of the GENIUS Act. The market is already betting that stablecoin-based payment infrastructure will replace existing players. Data from cryptocards is demonstrating how quickly this bet is becoming a reality.

$300 billion in stablecoins are looking for a way out.

The problem is that far less stablecoin is used for payments than is left unused. Currently, the total value of stablecoins on-chain is approximately $300 billion. The majority of this is idle and has not generated any productive returns.

Looking back at the early revenue structure of DeFi, the reason becomes clear. It involved token incentives, leverage, liquidity mining, and a cycle of borrowing funds using already mined assets as collateral and reinvesting them in mining. The revenue source was internal demand within the crypto market, funds circulating within the crypto space, rather than revenue linked to the external real economy.

On-chain lending has transformed this structure. The source of returns is no longer crypto speculation, but rather the credit needs of the real economy. Businesses, funds, fintech companies, and lending institutions borrow stablecoins for real-world business purposes. In 2025, the on-chain lending market grew from $252 million to $5.58 billion, an increase of approximately 22 times. This currently represents 17.3% of the entire RWA (Real Asset Tokenization) market, which is projected to reach $4 trillion by 2030.

This is a matter of scale. A market capable of accommodating $300 billion in stablecoin capital for productive allocation doesn't exist within the crypto space. The only market capable of absorbing this scale is the physical lending market. On-chain lending is precisely that channel.

The next challenge for DeFi: Making liquidity truly work.

The first generation of DeFi created liquidity. Capital accumulated on-chain at an unprecedented rate. However, this liquidity was largely self-circulating. The second generation of DeFi poses a different question: can this liquidity be made to function within the real economy?

Cryptocurrency cards offer an answer at the consumption level. On-chain lending, on the other hand, attempts to answer the same question at the capital allocation level. The simultaneous growth of these two markets is no coincidence. Stablecoins are being used as a means of actual payment and as a source of real credit—and the market has begun to prove this is feasible.

The data speaks for itself: monthly payments of $600 million have grown 22-fold in the credit market. $300 billion in stablecoins are searching for a way out, and their destination is gradually becoming clear.