Original author: Terry

Original source: Vernacular Blockchain

On November 1, PayPal received a subpoena from the U.S. Securities and Exchange Commission (SEC) enforcement department regarding PayPal's U.S. dollar stablecoin. PYUSD, which had high hopes, seemed to be overshadowed by the troubles Facebook faced when it launched Libra.

At the same time, with the continuous diversified development of global stablecoins, various countries are also actively researching and launching central bank digital currency (CBDC). Among them, the regulatory trends in the United States have attracted global attention. However, not long ago, representatives of the U.S. House of Representatives Financial Services Committee Tom Emmer proposed a "CBDC Anti-Surveillance State Act" aimed at preventing the Federal Reserve from directly issuing central bank digital currency (CBDC) to individuals, and preventing the Federal Reserve from indirectly issuing CBDC through intermediaries.

The Fed and Congress: Regulation and privacy at odds

After Facebook (now Meta) released the white paper of its private digital currency project Libra in June 2019, it was a catalyst to some extent, forcing central banks to speed up their original digital currency projects, which greatly stimulated the The interest of central banks in various countries in CBDC and the global stable currency system.

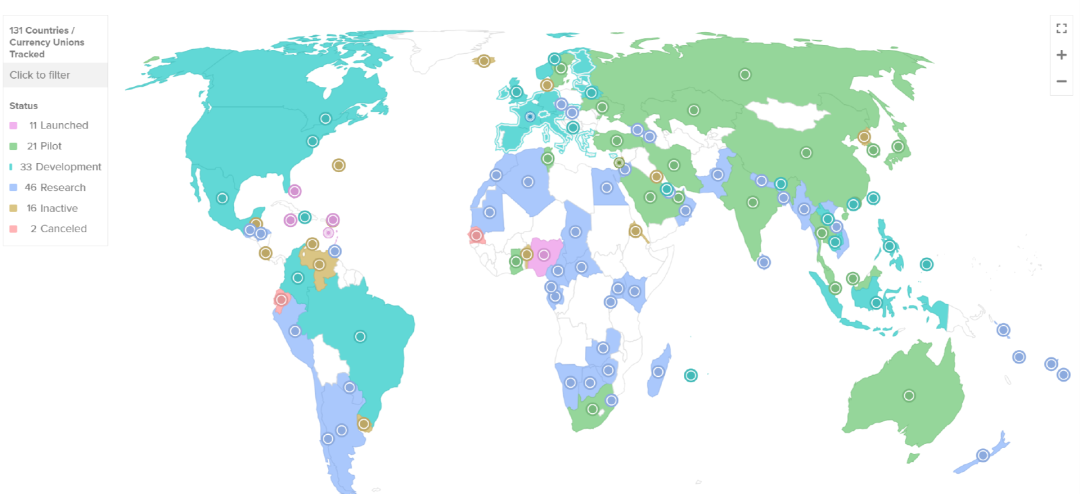

Atlantic Council statistics show that a total of 131 countries around the world (accounting for more than 90% of global GDP) are exploring CBDC , but among the 4 developed countries with the largest central banks (Federal Reserve, European Central Bank, Bank of Japan and Bank of England) , are relatively cautious, and the progress of CBDC in the United States is even more lagging behind.

In short, there is still no unified consensus at the regulatory level in the United States on whether to launch a CBDC. The biggest disagreement lies in the different positions:

U.S. congressmen expressed their opposition more from the perspective of privacy and financial freedom, saying many times that "CBDC is a government-controlled programmable currency. If it is not designed to imitate cash, it may give the federal government the ability to monitor and restricting U.S. transactions."

Regulatory agencies such as the Federal Reserve and SEC are more concerned about the significant impact that CBDC has on the payment and settlement system and the supervision of stablecoins on the chain.

As Federal Reserve Chairman Jerome Powell said at a recent congressional hearing on September 28: "There is a lot of private innovation, a lot of which is happening outside the scope of regulation, and when it comes to the public's money, we need Make sure there is appropriate regulation. And currently there is indeed no regulation in some cases."

At the same time, he said that the Federal Reserve is "actively evaluating whether to issue CBDC, and if so, in what form." He also said that reports on CBDC, stablecoins, and cryptocurrencies will be released soon, which means that the United States currently has no requirements for issuing its own CBDC . It is still in the early stage of evaluation and research, and no specific technical solution for the adoption plan has been determined yet.

However, although the U.S. official has not yet reached a unified opinion on the issuance of digital dollars, in fact, the digitization of the U.S. dollar chain has gone a long way with the help of U.S. dollar stablecoins. U.S. dollar stablecoins are now essentially U.S. dollar digitization tools .

Tether, Circle, the driving force behind the digitization of the U.S. dollar

The emergence of Libra made many people exclaim that the "digital dollar" era was coming, but most people did not expect that it was almost its only highlight moment.

Since then, Libra has continued to shrink and adjust its vision under regulatory pressure. The explosive growth of US dollar-centered stablecoins in 2020 can be regarded as a relay to another extent for Libra's large-scale "digital dollar" Experiment.

In particular, USDT and USDC have become the US dollar alternatives for many users in global application scenarios such as cross-border payments. As of November 3, Coingecko data shows that the total circulating market value of USDT has exceeded US$85 billion . A record high.

Even as USDT continues to grow, it not only has to serve the retail and consumer markets, but is obviously currently serving many mid-sized and large companies internationally.

At the same time, Tether’s exposure to U.S. government bonds reached $72.5 billion, making it the top 22 buyers in the world, higher than the United Arab Emirates, Mexico, Australia, Spain and other countries. Circle also holds more than $30 billion in U.S. government bonds. Tether, Circle has almost become the Fed’s voice for the crypto industry.

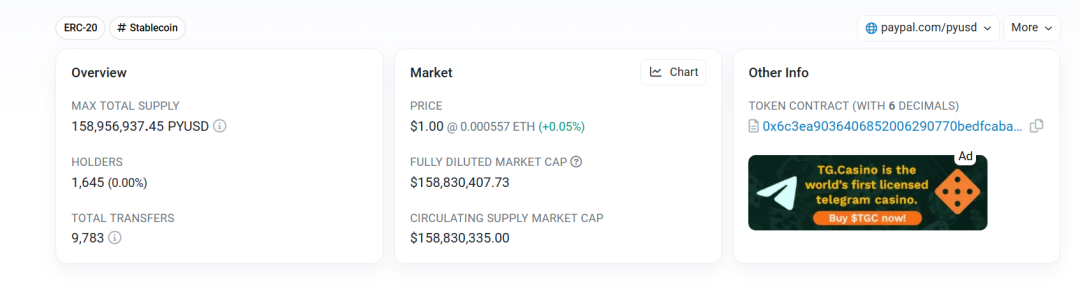

It is worth noting that the total issuance of the US dollar stable currency PYUSD launched by PayPal has been hovering around US$40 million for many days. It has also restarted money printing since October. As of the time of publication, it has exceeded 150 million and is traded on mainstream transactions such as Coinbase and Kraken. on line.

As a well-known traditional payment giant, PayPal’s every move in the stablecoin field not only brings new variables to the originally fixed stablecoin market, but also undoubtedly has a huge flow effect, and is also destined to change the regulatory level. The focus is once again on Facebook, just like Libra when Facebook failed midway.

Overall, as the largest third-party payment institution in the United States, PYUSD is destined to bring long-term benefits to the encryption market, especially the choice of issuance based on Ethereum, which further advances the vision of Ethereum as a global settlement layer. .

Stablecoins & CBDC?

However, the continuous expansion of stablecoins has both advantages and disadvantages for the digitization of the U.S. dollar, and may bring some potential risks and challenges:

On the one hand, as stablecoins are widely used, they have an increasing impact on the existing financial system. The combined volume of USDT/USDC has exceeded 100 billion U.S. dollars, and may even cause systemic risks;

On the other hand, stablecoins still lack direct supervision to some extent. If used as a tool for illegal activities such as money laundering and fraud, it may also cause certain damage to the financial order;

This leads to some underlying differences and characteristics between CBDC and stablecoins. First of all, it needs to be made clear that central bank digital currency (CBDC) may not have much to do with blockchain, because all CBDCs must be centralized systems.

Taking China's Digital RMB (DCEP) as an example, it is clear that it does not adopt the current mainstream public chain architecture, and adopts a two-tier operating model in terms of operating mechanism. The central bank is the first layer and first exchanges DCEP to specific businesses such as commercial banks. Institutions, and then commercial banks or specific commercial institutions serve as the second layer, responsible for meeting the public needs of individuals and enterprises to open digital wallets and exchange DCEP. This design is basically similar to the current centralized delivery mechanism of cash issuance.

Therefore, if the Federal Reserve Board issues CBDC in the future, it will be two different species from the existing on-chain stablecoins such as USDT, USDC, PYUSD or DAI - CBDC will rely more on the existing traditional financial system for issuance and operation, allowing Banks and financial institutions are connected to the digital currency system.

This actually means that CBDC is a more controllable and centralized digitization of the U.S. dollar. This will not directly cause competition with stablecoins on the chain to a certain extent, especially now that countries are vigorously researching and launching CBDC. , the cross-system exchange of CBDC between different countries is actually still in its early stages, and the convenience is definitely not comparable to stablecoins based on global public chains such as USDT.

Therefore, there may be a complementary relationship. For example, the stable currency on the chain is responsible for cross-border payment and settlement, and CBDC realizes the digital currency management of the financial system by forming various financial products based on digital currency.

But on the other hand, in the context of the continuous development of digital currencies such as stablecoins and Bitcoin, a more "controllable" CBDC can actually help the central bank cope with the challenges of third-party payments and private digital currencies, and better maintain the stability of the financial market. Stability and ensuring the international status of the dollar, in addition to increasing the transparency of the financial system and reducing the possibility of illegal activities.

Therefore, under this circumstance, the necessity for the Federal Reserve to launch CBDC has become increasingly apparent. In particular, how to balance the advantages and potential risks of stablecoins and how to formulate corresponding regulatory policies will be issues that need to be discussed in depth in the future.

summary

The issuance of CBDC by the Federal Reserve is still unknown, because if there is no legal definition, the central bank will only issue stable currency, not a true central bank digital currency, so this requires the Federal Reserve and the US executive and legislative levels to reach a consensus.

However, as the volume of stablecoins on the chain such as USDT and USDC continues to expand, and the giants behind Libra and PYUSD continue to make moves, I believe that financial regulatory agencies will take action soon, both for innovation and for the future.

(The above content is excerpted and reprinted with the authorization of partner MarsBit , original text link | Source: Vernacular Blockchain )

Statement: The article only represents the author's personal views and opinions, and does not represent the BlockCast. All contents and opinions are for reference only and do not constitute investment advice. Investors should make their own decisions and transactions, and the author and BlockCast will not be held responsible for any direct or indirect losses caused by investors' transactions.