Although we've liquidated our positions, I remain very optimistic about BTC's performance next year.

First, let me explain why it's falling: The main reason for the poor market sentiment is the rapid decline—a drop of $30,000 in three weeks, coinciding with the four-year cycle's peak reversal pattern. This has led to widespread market despair and rapidly spreading pessimism.

Since July 2025, Bitcoin has essentially been consolidating for nearly five months. If we extend the timeframe, the period since breaking $100,000 in November 2024 can be considered a year-long period of high-level consolidation. Why is this happening? We believe there's a crucial asset pricing factor at play: Bitcoin is a barometer of the endogenous liquidity of the US dollar.

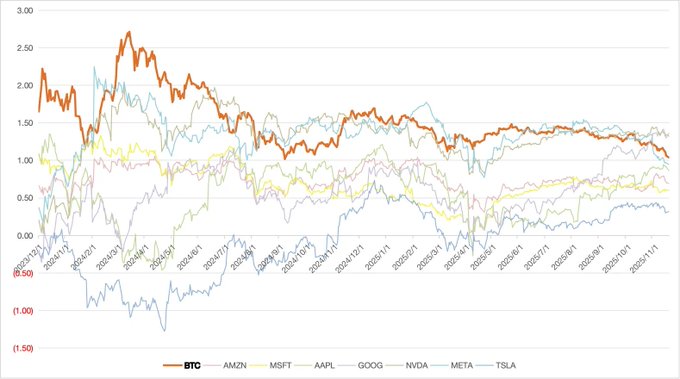

We previously made the mistake of believing there was a strong correlation between BTC and global liquidity, but the recent divergence between BTC and Global M2 has proven this assumption wrong.

Looking back at the new purchasing power of BTC over the past three years, it's clear that the main new purchasing power for Bitcoin comes from US domestic dollar institutions (ETFs, DAT, etc.). In contrast, gold's purchasing power is more diversified (global central banks), while facing less marginal supply (selling pressure).

Recent government shutdowns and the Treasury's continuous replenishment since April have ultimately drained the dollar's endogenous liquidity. However, global liquidity has remained generally stable and improving. Therefore, we have observed a continued disconnect between global assets like gold and leading US AI stocks, and Bitcoin and the Russell 2000.

To answer your question about the future market outlook:

We firmly believe that balance sheet expansion will be the true driving force behind Bitcoin's subsequent price movements, not the halving. Therefore, we are not referring to a four-year cycle.

In fact, since the ETF was approved, Bitcoin's status as the best Sharpe ratio asset in the dollar system has not been disproven. In the first quarter of 2025, Bitcoin also experienced a significant correction before the core US AI stocks, largely in sync with fundamentally questionable, liquidity-driven assets like META. Although recent negative factors, including the potential removal of MSTR from the MSCI index, have continued to dampen market sentiment, Bitcoin's core asset definition will not change since 2024. Before the asset definition is disproven, every decline represents future profit.

The market's extreme panic is approaching that of April. However, we do not believe a reversal will occur immediately. Specifically: the December rate cut does not constitute a true turning point in liquidity; the market has entered a cycle of accelerating rotation without actual balance sheet expansion.

Looking ahead at liquidity, we believe the Fed's return to balance sheet expansion is only a matter of time. Our core understanding includes three points:

First, the US unemployment problem is exacerbated by AI development. As Powell recently stated, the labor market cannot withstand higher interest rates, and the characteristics of a K-shaped economy have never been more pronounced;

Second, Sino-US relations are easing, with both sides showing a stronger dovish tendency in monetary and fiscal policy. The so-called "TACO" incident has occurred repeatedly, and everyone is increasingly aware that a real conflict between the two countries is unlikely;

Finally, the high-interest-rate environment within the US is unsustainable. By 2026, a large portion of the private credit market will face concentrated renewal pressure. Current interest rate levels are unsustainable for both the real economy and the financial system. With the new Federal Reserve Chairman in office, the market widely expects the Fed's policy to further shift towards easing.

Meanwhile, the US fiscal system is nearing its limits. As Trump's domestic election prospects become increasingly challenging, easing is the only solution. However, easing is like an addiction; Powell's short-term suppression will only embolden his successor. We have very positive expectations for potential QE in the first half of 2026.

Therefore, the current sideways movement and short-term pressure are not signs of fatigue, but rather a preparatory phase for a new bubble cycle. Liquidity is re-accumulating, but has not yet been fully released. In this prelude to asset repricing, Bitcoin remains the purest and most acute mirror of the dollar bubble era.

So here we only need to patiently wait for specific signals of QE activation, and then, based on BTC's price movement, choose opportune moments to build positions.

At this moment, concerns about currency stability, sovereign stability, financial stability, and asset security are precisely the scenarios envisioned when Bitcoin was born nearly 20 years ago, and also the best window for investment. If we must look for potential buying opportunities from a technical perspective, the support level around 68,000-75,000 is worth observing.

twitter.com/0xBFRuby/status/19...