At 2 a.m. Beijing time on September 19, the Federal Open Market Committee (FOMC) of the Federal Reserve announced that it would cut the federal funds rate by 50 basis points to 4.75%~5.00%, exceeding market expectations and marking the first interest rate cut since March 16, 2020.

At this point, the Fed’s policy shift has been completed, and a new round of monetary easing cycle has officially begun.

The FOMC policy statement said that although inflation has made further progress toward the 2% target, it is still at a "slightly high" level, and the risks facing employment and inflation targets are in balance. After the Fed's interest rate decision was announced, U.S. stocks rose further. As of press time, the Nasdaq rose more than 1%, the S&P 500 rose 0.72%, and the Dow rose 0.74%. Spot gold continued to rise, reaching the $2,600/ounce mark, a record high.

The Fed's rate cut has a significant impact on global asset allocation, US dollar liquidity, US stocks, US bonds, commodity trends and other countries' economies. Which markets or sectors will usher in new investment opportunities? How will the US dollar, US stocks and US bonds perform? Will China's economy and capital markets be affected by the Fed's rate cut? How will investors "respond"?

In this regard, the reporter of "Daily Economic News" (hereinafter referred to as the reporter of "Daily Economic News") interviewed the chief economists, chief strategy analysts and research teams of many well-known institutions at home and abroad, and selected six representative judgments for reference by investors, economic researchers and policy and institutional system practitioners.

1 Brian Coulton, chief economist of Fitch Ratings: This round of easing cycle will last for 25 months, with 10 interest rate cuts, a cumulative reduction of 250 basis points

At 2 a.m. on the 19th, the Federal Open Market Committee of the Federal Reserve ended its two-day interest rate meeting and announced the interest rate decision, lowering the target range of the federal funds rate by 50 basis points to 4.75%~5.00%. This means that the Federal Reserve has officially joined the ranks of major central banks around the world, such as the European Central Bank and the Bank of England, and started an easing cycle.

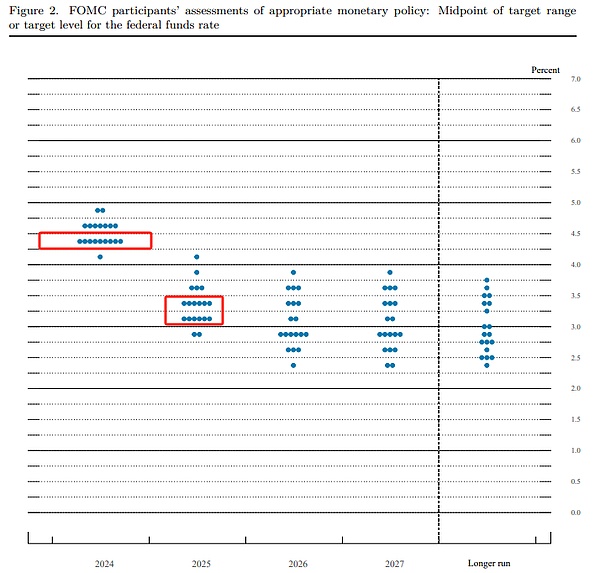

The press release issued by the FOMC showed that except for Director Bowman who believed that the interest rate should be cut by 25 basis points, all other voting members voted in favor of a 50 basis point cut. The "Summary of Economic Projections (SEP)" and "Dot Plot" released at the same time showed that the FOMC lowered its forecast for US GDP growth this year from 2.1% in June to 2%, lowered its forecast for core PCE at the end of the year from 2.8% to 2.6%, raised its forecast for the unemployment rate at the end of the year from 4.0% to 4.4%, and expected to cut interest rates by 50 basis points this year.

FOMC September “Dot Chart” Image source: Federal Reserve

With the first rate cut, the pace of subsequent rate cuts has become the focus of market attention. Most voting members believe that the federal funds rate will be lowered to 4.25%-4.50% at the end of this year, but the voting members disagree on whether the rate should be cut by a total of 100 basis points or 125 basis points in 2025.

Brian Coulton, chief economist of Fitch Ratings, said in an email to the reporter of Daily Economic News that the Federal Reserve is expected to cut interest rates twice this year, five times in 2025 and three times in 2026, and the federal funds rate will be reduced to 3% by September 2026. This means that during this easing cycle, which is expected to last 25 months, the Federal Reserve will cut interest rates 10 times, with a cumulative rate cut of 250 basis points.

Coulton explained: "If we exclude some very short-term rate cut cycles in the 1970s and early 1980s, the median rate cut and duration in the Fed's easing cycles since the 1950s would be 550 basis points and 18 months, respectively." He also pointed out that the reason why the Fed is expected to ease at a relatively moderate pace is that it still has work to do in fighting inflation.

2Barclays Research Team: Options trading can be an attractive tool to hedge against recession risks

The dollar has been under pressure in recent days as traders prepare for the Federal Reserve's first rate cut, which would theoretically reduce investors' incentive to buy U.S. Treasuries, weakening demand for the greenback.

Analyzing the impact of the Fed's previous interest rate cut cycles on the US dollar trend, Goldman Sachs believes that monetary policy coordination is the key, and the magnitude and speed of the Fed's interest rate cuts will not have a clear impact on the US dollar . Even during the Fed's interest rate cut cycle, the US dollar will not necessarily perform worse than other currencies. On the contrary, the coordination of interest rate cuts and the macroeconomic environment are more important.

Performance of U.S. and Chinese stocks, the U.S. dollar, and 10-year U.S. Treasury bonds in past interest rate cut cycles Image source: Meijing Charting (Data source: Haitong Securities)

The Barclays research team pointed out in an interview with the "Daily Economic News" reporter that the recent risk of a US recession has led to increased economic uncertainty and intensified foreign exchange market volatility, but from a historical standard, the current level of foreign exchange volatility is still low, and the risk premium of major currency options is still below the historical average. Therefore, option trading can be an attractive tool to hedge against recession risks .

Regarding the impact of interest rate cuts on US stocks and US bonds, Dr. Zhang Ling, chief economist of Huatong Securities International, believes that in the short term, the extent of the interest rate cut should be considered. A 25 basis point interest rate cut means that there is a high possibility of a precautionary interest rate cut, while a 50 basis point interest rate cut indicates that the Federal Reserve may believe that the possibility of a "hard landing" of the economy is high, which will bring uncertainty.

Lian Ping, Chairman of the China Chief Economist Forum: Interest rate cuts may push up gold prices together with a series of other factors

Since early June this year, as the expectation of the Fed's interest rate cut continued to rise, COMEX gold continued to rise. As of noon on September 17, COMEX gold had risen from $2,304.2/ounce to more than $2,600/ounce. After the Fed announced the interest rate cut, spot gold continued to rise, reaching the $2,600/ounce mark as of press time, setting a record high.

Lian Ping, president and chief economist of Guangkai Industrial Research Institute and chairman of China Chief Economist Forum, told the Daily Economic News that the Fed's interest rate cut will have an impact on the gold market in the short term , which may lead to a large increase or a certain degree of decline as the interest rate cut is implemented. Overall, there may be large fluctuations in the short term.

In the medium and long term, Lian Ping analyzed that this round of interest rate cuts may be relatively gradual and is expected to last from September this year to the end of next year or even longer . This is a preventive interest rate cut, mainly to prevent the economy from continuing to decline and go into recession, so the rate cut will not be too strong, and is expected to be between 150 and 200 basis points, unless the US economy shows a significant recession in the short term. Therefore, the stimulus of the Fed's interest rate cut on gold prices may be a gradual process of pushing up in the medium term, and the thrust is relatively mild.

Lian Ping further analyzed that, in fact, in the future, the Fed's interest rate cut is likely to push up the gold price together with a series of other factors. After the interest rate cut, inflation may gradually rise slightly, so the value-preserving function of gold will be revealed again. At the same time, in the complex environment of continuous geopolitical conflicts, "black swan" events may continue to occur in the future, promoting more obvious risk aversion demand.

Furthermore, a series of new changes have also occurred in the international monetary system, with the credit of the US dollar shaken and the euro performing weakly. In the context of de-dollarization, the RMB has gained development opportunities. However, the RMB is still in the early stages of internationalization. In this case, central banks of various countries may pay more attention to maintaining and increasing their gold reserves for the sake of reserve function. In summary, Lian Ping pointed out that in the medium and long term, gold still has room for further appreciation.

Image source: Meijing Mapping

4 Guan Tao, Global Chief Economist of BOC Securities: Interest rate cuts will help expand China's monetary policy autonomy

From the perspective of the economic cycles of China and the United States, Guan Tao, global chief economist of BOC Securities, pointed out in an interview with a reporter from the "Daily Economic News" that, given that other conditions remain unchanged, the Federal Reserve's interest rate cut will help converge the divergence between the economic cycles and monetary policies of China and the United States , ease China's capital outflow and exchange rate adjustment pressure, and broaden China's monetary policy autonomy, but we should not expect too much from this .

First, in his view, China has always insisted on "self-centered" monetary policy . Before 2022, in response to the epidemic, China's monetary policy was first-in-first-out, playing the role of a leader rather than a follower. The Fed's interest rate cut in the future does not mean that China will necessarily follow the reserve requirement ratio and interest rate cut , because China also needs to take into account the long-term and short-term, internal and external balance, stable growth and risk prevention.

Secondly, after the first rate cut, market focus will shift to the timing and magnitude of the Fed’s next rate cut. Market expectations will continue to switch between a “soft landing,” “hard landing,” and “no landing” of the U.S. economy, and international financial turmoil is inevitable.

Guan Tao pointed out that no matter what happens to the US economy, it will have both advantages and disadvantages for the Chinese economy. The key for China is to do its own thing well . If the US economy does not decline, it is possible that the Federal Reserve will not cut interest rates significantly, and the US dollar will not weaken in a trend. This will continue to form external constraints on China's monetary policy, but will help stabilize external demand and support the smooth operation of the Chinese economy. If the US economy falls into recession, it may trigger a sharp interest rate cut by the Federal Reserve. After the market's risk aversion sentiment subsides, the US dollar will weaken in a trend. This will help open up space for China's monetary policy and ease the external pressure of China's capital outflow and exchange rate adjustment, but it will not be conducive to stabilizing external demand and affect the smooth operation of the Chinese economy.

As for China, Guan Tao finally pointed out that it is necessary to make contingency plans based on scenario analysis and stress testing to be prepared for any eventuality.

Regarding other emerging markets, the Barclays research team also pointed out in an interview with a reporter from China Business Network that the Fed's influence on emerging market policies has declined. Barclays believes that with the Fed's monetary policy restrictions lifted, global growth slowing and global commodity inflation under control, emerging market central banks may give priority to more relaxed policies rather than strong currencies. The bank believes that most central banks relax policies as much as possible under low inflation, but maintain high real interest rates to protect their currency exchange rates.

5 Zhang Ling, Chief Economist of Huatong Securities International: Emerging markets are likely to receive more international capital inflows

As the Fed begins to cut interest rates, changes in exchange rates will not only affect the settlement costs of international trade, but may also trigger the acceleration of capital flows and changes in foreign exchange reserves. In theory, the Fed's monetary easing cycle will lead to a decline in US dollar interest rates, driving international capital to emerging markets with higher returns.

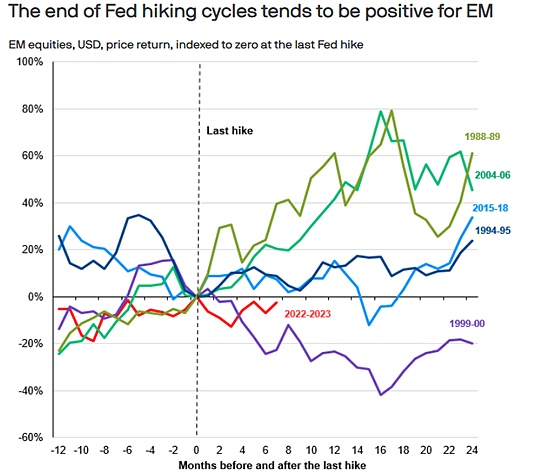

In an article recently published, JPMorgan Asset Management stated that in four of the past five interest rate hike cycles of the Federal Reserve since 1988, emerging market stocks have performed positively two years after the Fed's last rate hike, with an average return rate of 29%, even 17 percentage points higher than the return rate of developed market stocks in the same period.

The end of the Fed’s rate hike cycle tends to be good for emerging markets Image source: JPMorgan Chase

“Of course, the broader fundamental backdrop is also important, but U.S. interest rates do play a disproportionate role in driving capital inflows and outflows from emerging markets. As a riskier asset class, emerging market assets tend to benefit when the Federal Reserve completes rate hikes, global economic sentiment improves, and risk appetite is higher,” the article noted.

Dr. Zhang Ling, chief economist of Huatong Securities International, also pointed out to the reporter of "Daily Economic News" that based on the long-term performance of the Federal Reserve's multiple interest rate cut cycles in the past few decades, emerging markets have generally performed well during the interest rate cut cycles . It can be seen that in the past two weeks, the prices of assets that are closely related to the US dollar and US stocks have increased significantly.

"However, how international capital flows during the interest rate cut cycle still depends on whether the U.S. economy can generally reflect people's expectations and whether its fundamentals are strong enough. If interest rates are cut too quickly, it may cause people to worry about the global economy. At present, we remain cautiously optimistic. As far as the current global economy, especially the performance of economies with a high degree of correlation with the United States, overall asset prices are at a low level. In the case of the Fed's interest rate cut, it is highly likely that more international capital will flow into emerging markets. " Dr. Zhang Ling added to reporters.

However, some studies have pointed out that in past monetary easing cycles, capital inflows into many emerging and developing markets have proved to be relatively resilient, thanks to their sound policy frameworks and healthy foreign exchange reserves.

6 Gui Haoming, chief market expert at Shenyin & Wanguo Securities Research Institute: From an investment perspective, dollar holders are unlikely to sell immediately, and there will not be a big direct reaction on the domestic capital market.

How can we strategically respond to the allocation of major asset classes under the influence of the Federal Reserve’s interest rate cuts?

Gui Haoming, chief market expert at Shenyin & Wanguo Securities Research Institute, pointed out in an interview with the "Daily Economic News" reporter that in terms of equity assets, the Fed's interest rate cut will help improve market risk appetite , especially in terms of triggering capital outflows from the U.S. capital market and then flowing into other markets. However, the current continued adjustment of the A-share market has its own internal logic, and the focus is not on the relatively high interest rate gap between China and the United States.

According to his analysis, it will take some time for the interest rate gap between China and the United States to eventually close , and we cannot expect a single rate cut to fundamentally change the direction of capital flows, as this is a gradual process. Therefore, for domestic risk assets, it is difficult to expect a major shift in direction due to the Fed's rate cut.

In general, Gui Haoming said that the Fed's interest rate cut will bring certain benefits to domestic economic activities, but it is more based on a long-term perspective . Since we are at the end of the transmission of this effect, the short-term effect will not be great. As for A-shares, it is more of a psychological effect. In terms of low-risk asset allocation, Gui Haoming analyzed that low-risk investors pay more attention to safety. At present, although domestic interest rates are relatively low, investors value relatively stable returns. In this case, it is difficult to say that domestic fixed-income asset trading behavior is based on the US dollar interest rate as a reference.

From the perspective of US dollar allocation, he believes that one or two interest rate cuts will not change the relatively high level of US dollar interest rates. From an investment perspective, the US dollar is still more attractive, and US dollar holders are unlikely to sell immediately just because of this interest rate cut .

However, Gui Haoming emphasized that the greater significance of the Fed's interest rate cut this time is that it has opened the channel for the US dollar to cut interest rates. The trend of the US dollar interest rate rise for several consecutive years has been substantially changed. In the future, there is a high probability that the US dollar interest rate will gradually decline, and the impact on the operation of the international economy will become more and more apparent, but this requires a process. Therefore, for now, the US dollar interest rate cut will not have a big direct impact on the domestic capital market.