Author: CMed

In the past few days, the US stock market and the cryptocurrency market have all been dazzled by MSTR. In the latest round of the BTC market, MSTR not only led the rally, but also maintained a growing premium over BTC for a period of time, with its price soaring from $120 a week or two ago to the current $247.

Regarding MSTR's surge, most people in the market still interpret it as "leveraged BTC". However, this does not seem to explain why MSTR's premium suddenly soared when the "debt financing to buy BTC" fundamentals remained unchanged. After all, Microstrategy has been buying BTC for so many years, but has never seen such a surge in premium.

In fact, the recent surge in MSTR's premium, in addition to "debt financing to buy BTC", is also due to another secret weapon of Microstrategy, which not only has a huge impact on MSTR's fundamentals, but is also called by many analysts as Microstrategy's "infinite money printing machine", making MSTR "the more you sell, the more valuable it becomes".

Leveraged BTC? An old story

Microstrategy, as a company focused on business intelligence software, has adopted a radical strategy since 2020: to raise funds through debt issuance to purchase BTC. This strategy was implemented starting in August 2020, when the company announced that it would convert $250 million of its treasury reserve assets into BTC. The motivation behind this strategy is mainly to address the challenges of declining cash returns and dollar depreciation in the global macroeconomic environment.

To further expand its BTC holdings, Microstrategy has raised funds in the capital markets through some long-term bonds in recent years. These bonds typically have longer maturities, mostly maturing between 2027-2028, and some are even zero-coupon bonds. This allows the company to maintain a lower financing cost in the coming years, and after obtaining the bond financing, quickly use it to purchase BTC, adding it directly to the company's balance sheet.

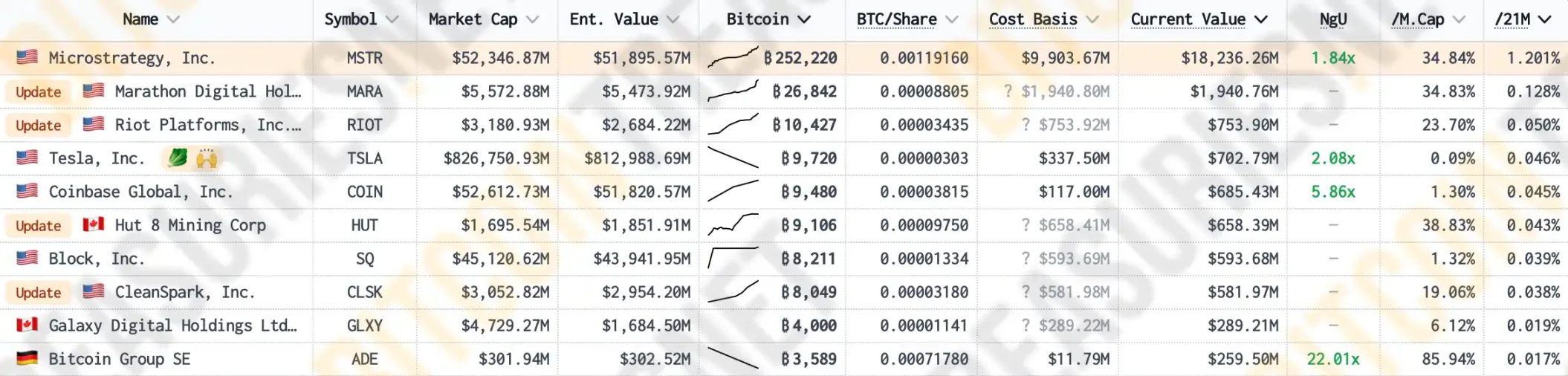

According to data from Bitcoin Treasuries, as of now, Microstrategy already holds 1.2% of the total circulating supply of BTC, making it the public company with the largest BTC holdings, far exceeding crypto-native companies like Marathon, Riot, and the leading crypto exchange platform Coinbase.

By financing through debt, MSTR has been continuously increasing its BTC holdings, which not only increases the amount of BTC on its balance sheet, but also exerts a clear driving force on the market price of BTC. As the proportion of BTC in MSTR's asset portfolio continues to increase, the correlation between the company's stock value and the BTC price has further strengthened. According to MSTR Tracker, the correlation coefficient between MSTR's stock price and BTC price has recently surged to 0.365, reaching a new high.

This correlation makes investors willing to buy MSTR's stock while being bullish on BTC, further driving up the company's market value. Of course, after 4 years of market and time testing, MSTR's "leveraged BTC effect" has long been an old story, and whenever MSTR's price rises, people always use the logic of "debt financing to buy BTC" to explain it.

However, in the recent BTC market, MSTR's market price not only rose before BTC, but also maintained an increasingly high premium over BTC for a period of time. This has left many investors puzzled: the fundamentals haven't changed, so why did the premium suddenly go up?

Premium issuance: "the more you sell, the more valuable it becomes", MSTR's cheat code

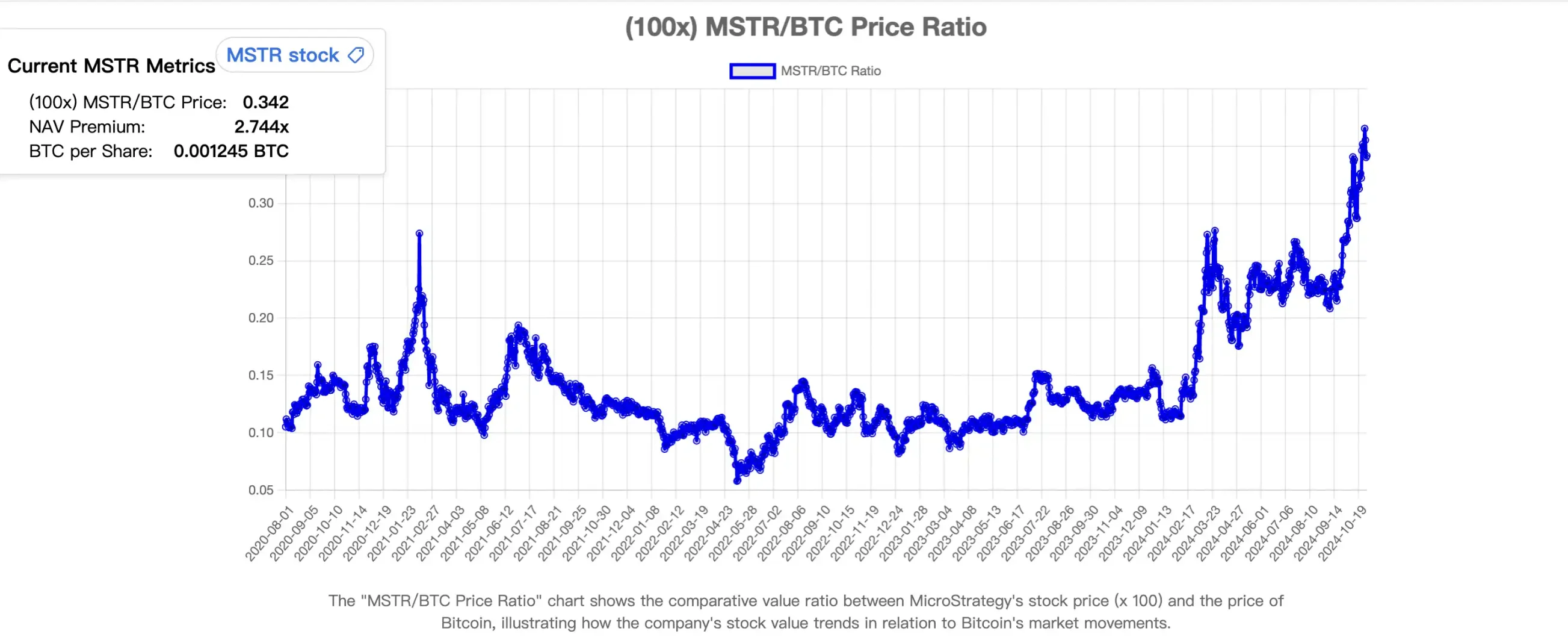

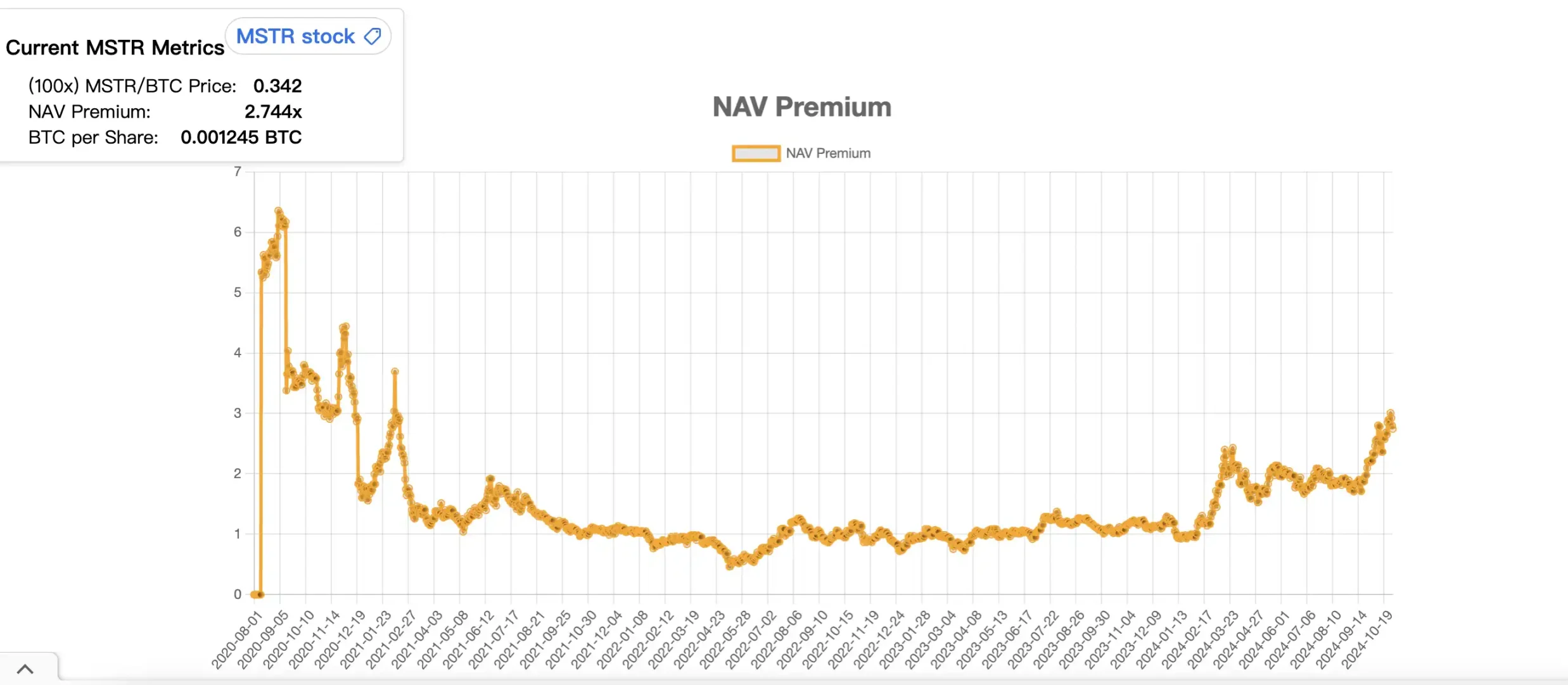

First, let's take a look at how outrageous MSTR's recent premium has been. According to MSTR Tracker, MSTR's premium over BTC has experienced a sharp increase from around 0.95 to 2.43 and then fallen back to around 1.65 in the period from February to March this year. The second rapid growth began on the eve of the recent BTC price increase, growing from around 1.84 to a peak of 3.04, and is currently maintained at around 2.8.

It can be seen that although Microstrategy has been accumulating BTC for the past 4 years, its NAV (Net Asset Value) premium has not shown a clear growth, but has remained in a 1:1 state for a relatively long period of time.

So what is the reason behind the rapid surge in MSTR's premium? Has the fundamentals of Microstrategy's "debt financing to buy BTC" changed?

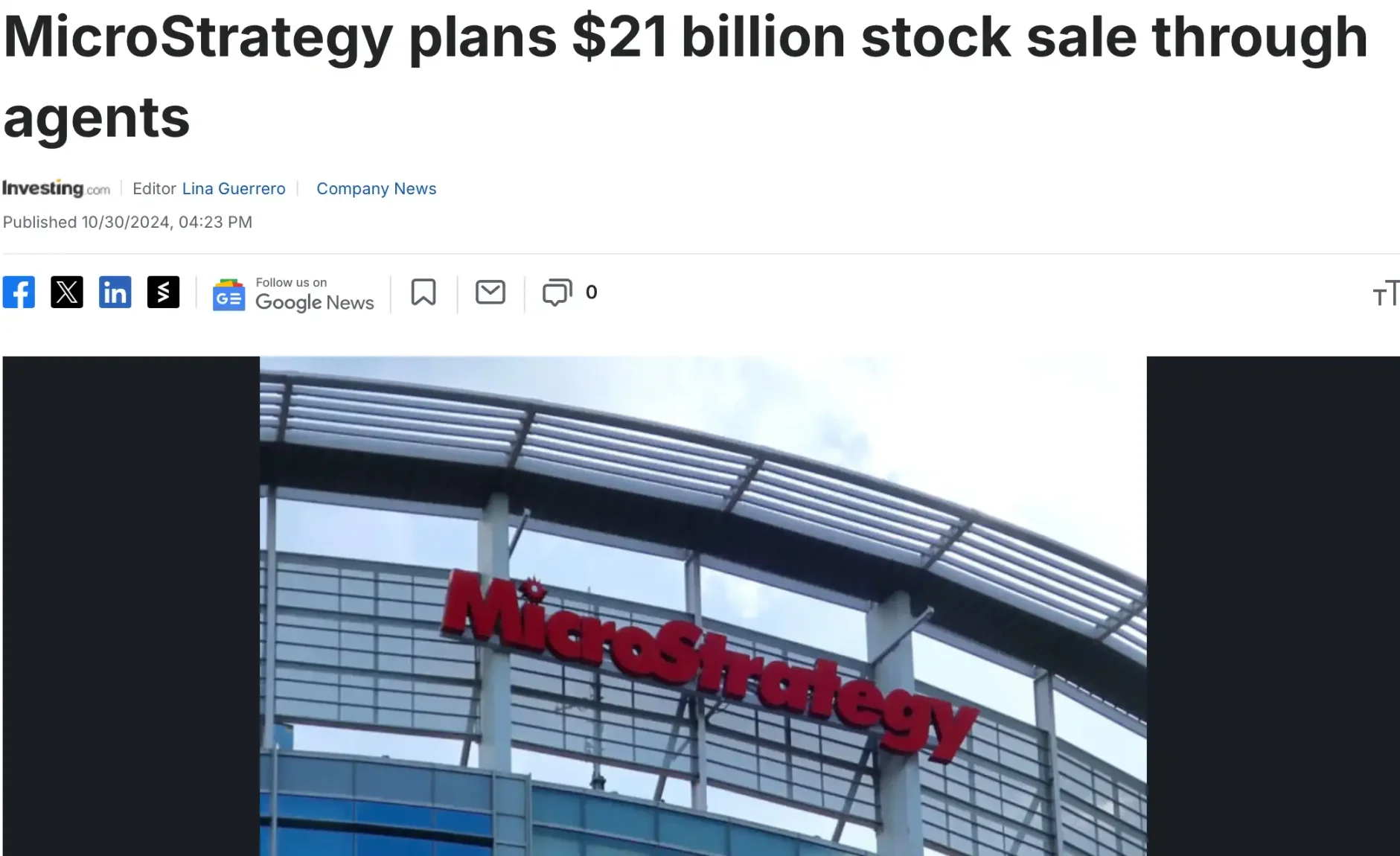

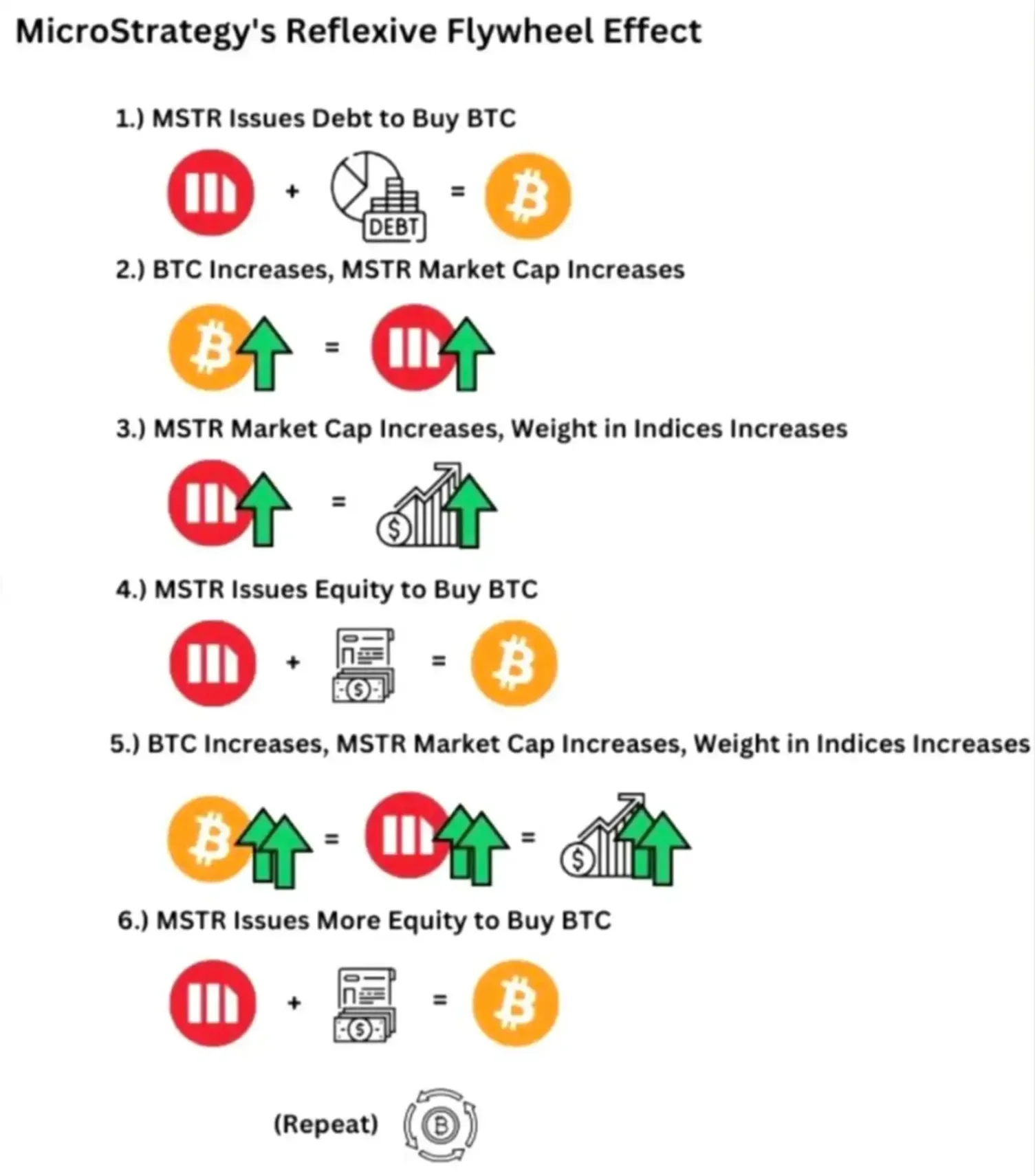

The answer is yes. This change in fundamentals is called "premium issuance". Since the middle and late part of last year, Microstrategy has adopted a new way of buying BTC, which is to purchase more BTC by issuing and selling its own MSTR shares. This "sell shares to buy BTC" strategy may seem very stupid at first glance, as it could not only hurt the stock price, but also threaten MSTR's market position as a "leveraged BTC".

However, when you analyze the logic chain carefully, you will find that this new "sell shares to buy BTC" model is simply MSTR's super flywheel and Microstrategy's infinite money printing machine.

First, we need to explain the concept of "net asset value premium" (NAV). Since MSTR holds a large amount of BTC through debt issuance, and the market has strong expectations for the future rise of BTC, the value of MSTR's stock often exceeds the value of the BTC it holds, and this premium is called the "net asset value premium". This "net asset value premium" reflects the market's expectation of the company's future expansion of BTC holdings, and has become the support point for MSTR's continuous issuance of shares to purchase more BTC.

On the other hand, when the price of BTC rises, Microstrategy's market value will also grow accordingly, which in turn forces various index funds to increase their purchases of MSTR based on weight considerations, further driving up its price and market value.

At this time, due to the existence of the "net asset value premium", MSTR can start its own "premium issuance" operation. By continuously issuing shares, it can obtain more funds to purchase BTC, drive up the price of BTC, and the rise of BTC will further increase the company's market value and financing capacity, so that this cycle can continue. This strategy creates a "reflexive flywheel effect".

The most ingenious point in Microstrategy's "reflexive flywheel effect" is that the issuance not only does not have a negative impact on MSTR's price, but actually makes MSTR more valuable.

When Microstrategy issues shares to purchase BTC, the newly issued shares are usually traded at a price higher than their net asset value. Leveraging this premium, Microstrategy can buy more BTC with the proceeds from selling each MSTR share than the BTC actually represented by the individual stock.

For example, based on the correlation coefficient between MSTR and BTC, 36% of the value of each MSTR share represents the BTC backed by the company. Without a premium, when Microstrategy sells MSTR, it can only exchange for about 36% of BTC. However, currently MSTR's premium over BTC is around 2.74, which means that when Microstrategy sells one MSTR share, it can exchange for about 98% of BTC.

This means that the company can use funds higher than the net asset value of BTC to increase its BTC holdings on the balance sheet. The core of this strategy is that MSTR can finance at a high premium, thereby increasing the speed and scale of its BTC holdings, which far exceeds the speed of the previous "debt financing to buy BTC".

After the flywheel appeared, MSTR, whose market value has been increasing, has also been included in the investment scope of the US stock index, which has brought in more incremental funds and generated more asset net value premium. One of the reasons why MSTR and BTC decoupled in the third quarter is that the market had pre-priced MSTR's inclusion in the NASDAQ 100 index, which would bring a large influx of passive funds.

US stock index investors will be "forced" to invest in MSTR, and then return to the reflexive flywheel, resulting in a greater asset net value premium, which can enable MSTR to raise more funds to increase its holdings of BTC, driving up the price of BTC, improving market optimism about MSTR, and the company's weight in the index may increase, triggering further buying demand from index funds, forming a self-reinforcing positive feedback loop, overall forming an index buying pressure flywheel.

From a larger time dimension, the amount of BTC held by each MSTR shareholder is constantly increasing, which not only enhances the market's recognition of MSTR as a "BTC alternative investment tool", but also improves the pricing expectation for MSTR.

"There will be more MSTR in the US stock market"

In the past few weeks, MicroStrategy CEO Michael Saylor has become increasingly high-profile, shouting on major podcasts and news programs that "there will be more MSTR in the US stock market" and that "MSTR's mechanism is simply a 'infinite financial banknote glitch'."

Saylor believes that MSTR's "reflexive flywheel" model has strong capital operation potential, which not only can continuously accumulate BTC, but also maintain its own growth through financing and stock price rise, demonstrating how a listed company can use asset premium and capital market financing capabilities to achieve long-term expansion. This model is not just a traditional "buy and hold" strategy, but a way to actively leverage the advantages of the capital market to expand the balance sheet. This mechanism may become an object of imitation for other companies, especially in resource-intensive or capital-intensive industries. In fact, there have been many companies that have imitated MSTR to carry out partial asset operations.

Currently, this "left foot on the right foot" model seems to be quite feasible, according to current data statistics, MSTR will use $1 to purchase BTC for every $2.713 of stock issued. Many believe that he is doing a high-leverage long on BTC in order to "outperform" BTC to a large extent, but in fact MSTR's health is very high, and it is estimated that only when the price of BTC falls below $700 per coin will MSTR have the risk of being liquidated.

At present, this mechanism seems to be running smoothly, with MSTR continuously increasing its holdings of BTC, but as this mechanism is used more and more widely, it will undoubtedly make the US stock index more affected by crypto assets and their related derivatives. This mechanism is like a rope, binding the crypto currency market and the US stock market together, which will bring about deep-seated changes in the market. For the crypto currency market, it undoubtedly introduces a large amount of liquidity overflow from the US stock market (mainly absorbed by BTC), while for the US stock market, it seems to exacerbate the volatility risk.

According to Sailor's (MSTR's founder) vision, by 2050, the price of BTC will reach $500,000 per coin, and he hopes that by then, MSTR will become a trillion-dollar company, better applying crypto currencies to deeper integration into people's lives, which sounds like a "perfected version of the Ponzi scheme" - whether this model can run until then remains to be tested by the market.