Author: Flip Research

Compiled by: TechFlow

The Retreat of American Exceptionalism

Warren Buffett often mentions the concept of the "American tailwind" in his annual letters, referring to the long-term advantage of the US economy on a global scale. His views have consistently proven to be correct, and this idea has helped him achieve astounding returns over multiple generations, making him one of the greatest investors of all time.

However, I believe this trend is rapidly changing. By the end of 2024, I will only hold a small amount of US stocks and cryptocurrencies. In this article, I will elaborate on the logic behind this trade and explain why I believe we may see a decline in the US Dollar Index (DXY) and continued underperformance of US stocks (and by extension, cryptocurrencies).

The Rise of AI: Global Competition and Value Shift

In the past few years, the rise of AI has undoubtedly been one of the most important trends. AI is rapidly changing the way we live, and the pace of this transformation is only accelerating. This trend is driven by a combination of factors:

Computing power growing exponentially according to Moore's Law, with the powerful parallel computing capabilities of GPUs further empowering this, and NVIDIA maintaining a leading position in this field.

Breakthroughs in scientific and technological advancements, such as the emergence of the Transformer architecture, laying the foundation for improved AI model performance.

Massive investments from both governments and private enterprises. For example, the global "Mag 7" tech giants are expected to invest over $300 billion in AI alone in 2025.

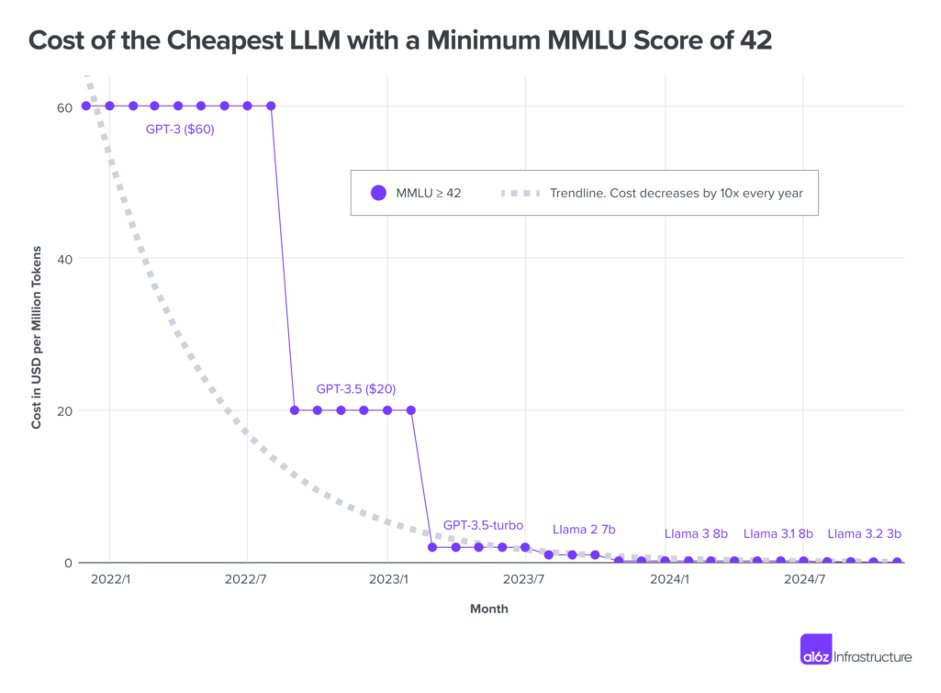

The combined effect of these factors has led to a significant reduction in the cost of AI model inference (the cost of using AI models). According to a16z's estimates, this cost has decreased by 1,000 times in the past three years.

Particularly, the release of DeepSeek r1 has accelerated this trend. Many have referred to it as the "Sputnik moment" of AI, similar to the technological race sparked by the Soviet Union's launch of the first artificial satellite in 1957. The difference is that this race is focused on building the most powerful large language models (LLMs) globally.

So, who will capture this value? In the short term, the value will flow down the value chain to the application layer, which are the companies and businesses built on top of LLMs. However, in the long run, as LLM performance continues to improve, competition among applications will intensify, development will become more accessible, and plug-and-play solutions will become more prevalent. Ultimately, this value will directly shift to individual users.

I believe the next 2-3 years will be a critical transformative period for the AI field, with an impact far exceeding most people's expectations. This is why I am convinced that AI-powered robotics will gradually demonstrate stronger competitiveness, as hardware interfaces have higher competitive barriers than software applications.

From an investment perspective, there is a clear mismatch in this area. Regardless of which country you are in, investment portfolios are typically concentrated in the S&P 500 index. With the proliferation of index funds, this trend has been further amplified - many ordinary households are directly investing their idle savings into S&P 500 ETFs (such as VOO), and investment forums commonly advise "putting all your money into the S&P 500 and never look back." The traditional 60/40 stock/bond portfolio has almost become a thing of the past. As a result, the S&P 500 currently accounts for more than half of the global stock market capitalization, with a total market value of around $55 trillion. This concentration of investment may overlook the new opportunities presented by the rise of AI.

Technological Transformation and Global Value Shift

Although global financial capital is highly concentrated in the US market, the most transformative technologies of our generation are redistributing value across the global population. This may be one of the most powerful "equalizers" we have seen - value gradually being reallocated according to the distribution of the world's population. So, what does this mean for the US? While the US holds over half of the world's financial capital, its population only accounts for 4.2% of the global total.

Of course, to convey the message more clearly, some of the above points have been simplified. For example, the Mag 7 companies have already recognized these potential risks. Companies like Meta have taken action by developing open-source models (such as Llama) to reduce inference costs, while also investing in robotics and the application layer. However, these facts do not change the core logic of the overall argument.

The Trump Effect: Concerns over America's Global Standing

There is no doubt that Donald Trump is reshaping the global political landscape - the "Make America Great Again" (MAGA) movement represents a radical departure from traditional political discourse. However, while Trump claims his policies will make America great again, I believe his policies are significantly undermining America's influence on the global stage and may ultimately lead to a gradual decline in America's prospects.

To understand this, we first need to understand why the US dollar has become the global reserve currency. On the surface, this can be attributed to the strong driving force of the US economy: the US economy accounts for around 26% of global GDP and has a robust, open, and highly liquid capital market.

However, this does not fully explain the global dominance of the US dollar. If it were solely based on economic factors, we should see the usage of other currencies proportional to their economic size. Yet, the reality is that the US dollar is involved in nearly 90% of global transactions. What truly underpins the US dollar is America's political and military power. Whenever a country becomes too powerful, the US imposes sanctions on it and demands that its allies take the same action. The recent policy of banning the export of high-performance GPUs to China is a clear example of this. This pattern is not new - historically, the British pound was the global reserve currency, relying on the military might of the British Empire, until the decline of the British Empire led to the loss of this status.

However, Trump is rapidly changing America's traditional position in the political and military realms. His "America First" philosophy, which prioritizes domestic affairs over traditional alliances and global military commitments, is having a significant impact:

Broad-based tariff threats: Trump has launched broad-based tariff threats against all trade partners, including long-standing allies. This has not only exacerbated anti-American sentiment (for example, in countries like Canada, there are already boycotts of American products), but also forced trade partners to turn to other countries and build closer economic ties.

Isolationist military policy: Trump's isolationist military policy has weakened the influence of NATO, while demanding that NATO member countries increase their defense spending to 5% of GDP. This policy has already prompted many European countries to compromise, increase their defense budgets, and reduce their dependence on the US, undoubtedly diminishing Trump's influence in Europe.

Europe's independence tendencies: This trend is unfolding in real-time. Today, the winner of the German election, Friedrich Merz, has openly stated that he will quickly push for European unity and "achieve independence from the US." This statement highlights the gradual weakening of Europe's dependence on the US under Trump's policies.

Reduction in foreign aid: The Trump administration has significantly reduced the United States' foreign aid program, which has long been an important tool for the US to exert influence globally. At the same time, China has taken a completely different strategy, especially in expanding its presence in Africa, ensuring access to valuable resources and critical supply chains through initiatives such as the "Belt and Road."

Tilt towards Russia: The Trump administration appears to have focused on "ending the war in Ukraine at all costs," leading to a deepening of US-Russia relations - even though Russia's GDP ranks only 11th globally. This policy choice not only alienates the US's traditional allies, but also risks weakening its strategic position globally.

The Fed's Dilemma

The current political and fiscal policies in the US have put the Federal Reserve in a difficult position. Many of the isolationist policies pursued by the Trump administration do not have economic rationality. The academic community has long proven that autarkic economic policies are far less effective than global cooperation. For example, the principle of comparative advantage clearly demonstrates the advantages of international division of labor.

Although the US market as a whole remains strong, some signs of weakness are beginning to emerge. The labor market is gradually cooling, and business investment is also declining. This is mainly because businesses tend to reduce long-term investment in an uncertain policy environment. The GDP growth forecast for 2025 is 2.2%, a moderate level of growth.

At the same time, inflationary pressures remain. The Consumer Price Index (CPI) rose 3% year-on-year in January, and has been on a continuous upward trend over the past 6 months. This conflicting trend of rising inflation and slowing economic growth forces the Fed to find a balance between the two. As of now, the market generally expects the Fed to only cut interest rates once or twice this year.

Observing capital flows has always been an important way to understand the market. Last year's market rally was mainly driven by expectations of deregulation and increased liquidity. However, this year's market sentiment is the opposite, more affected by tightening policies. However, it is worth noting that the Fed's Quantitative Tightening (QT) plan will be gradually relaxed in the first half of this year, which will inject additional liquidity into the market.

Conclusion

The "American exceptionalism" trade may be coming to an end, for complex reasons. But as the saying goes: "The market's irrationality may last longer than the investor's solvency."

So why now? In my view, the Trump administration is the catalyst for this change. He has changed the global political landscape in a way that has not been seen for decades, forcing traditional allies to re-evaluate their positions and seriously damaging the US's position on the international stage.

The current situation is already very fragile, and a small trigger could spark a huge transformation. For example, the EU leadership could simply say "no" to Trump's stance on the Ukraine issue, which could unite EU countries; or allies could start forming new trade alliances to cope with the uncertainty of US policies. In fact, we are already seeing the beginnings of this trend in the policies of Germany's new leadership.

However, the US economic situation cannot provide much confidence. At the same time, the impact of the AI transformation is also beginning to emerge. For example, the performance of the Chinese stock market this year has been significantly better than the US stock market, which may reflect the different development paths of the two countries in the technology field.

As for cryptocurrencies, I believe institutional investors view them as high-risk assets on the risk spectrum, and will adjust their capital flows accordingly based on the aforementioned trends. In the crypto space, institutional investors are often given a "halo," and many members of the crypto community (especially the crypto Twitter community, CT) have unrealistically high expectations for their investment behavior. However, these institutions actually do not have any inside information (and may even know less than the CT community). Therefore, when the market experiences violent adjustments, their losses may be as severe as those of ordinary investors. As for whether MicroStrategy (MSTR) is a Ponzi scheme, that is another topic worth exploring in depth.

Disclaimer: All the above views are my personal opinions, reflecting my own portfolio positioning. The content has been highly condensed to cater to the reading habits of the crypto Twitter community (CT focus points are relatively short). Please always do your own research (DYOR) and draw your own conclusions based on your own judgment.