Weekly recap of the crypto derivatives markets by BlockScholes.

Key Insights:

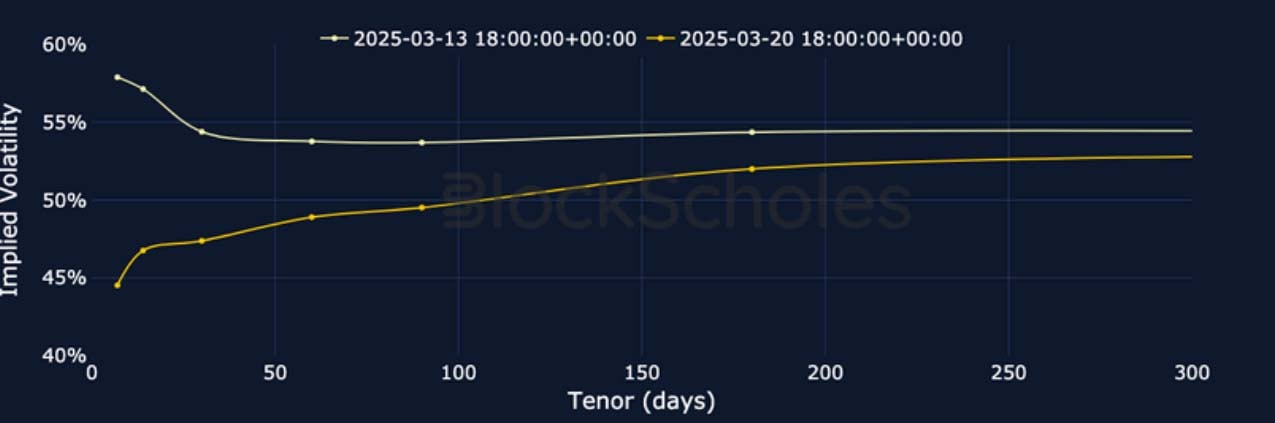

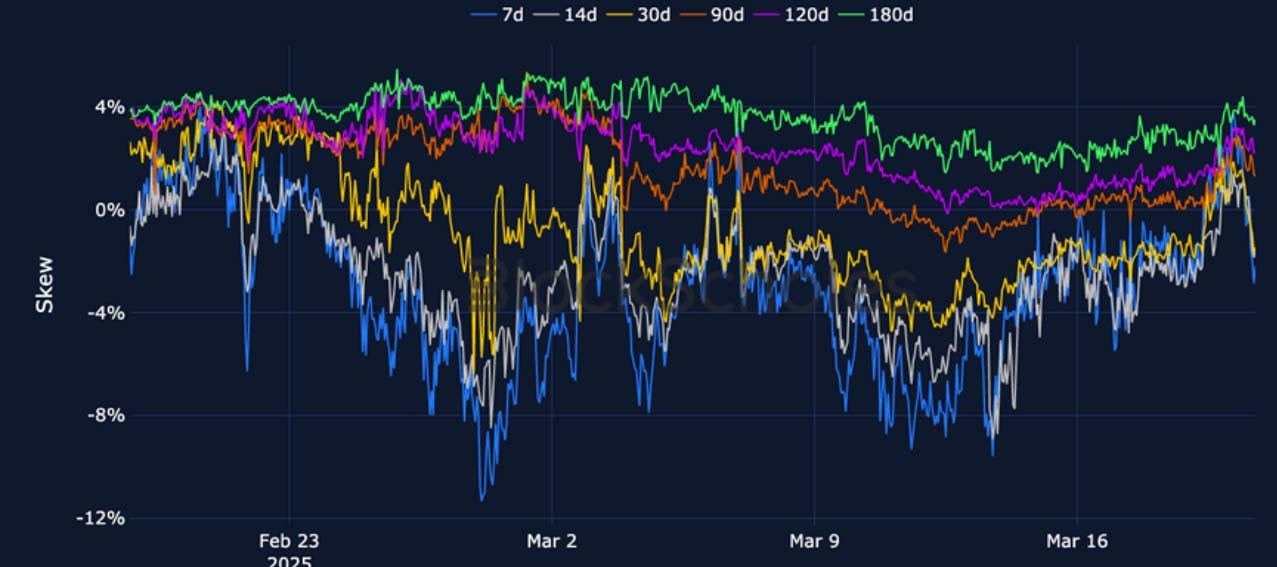

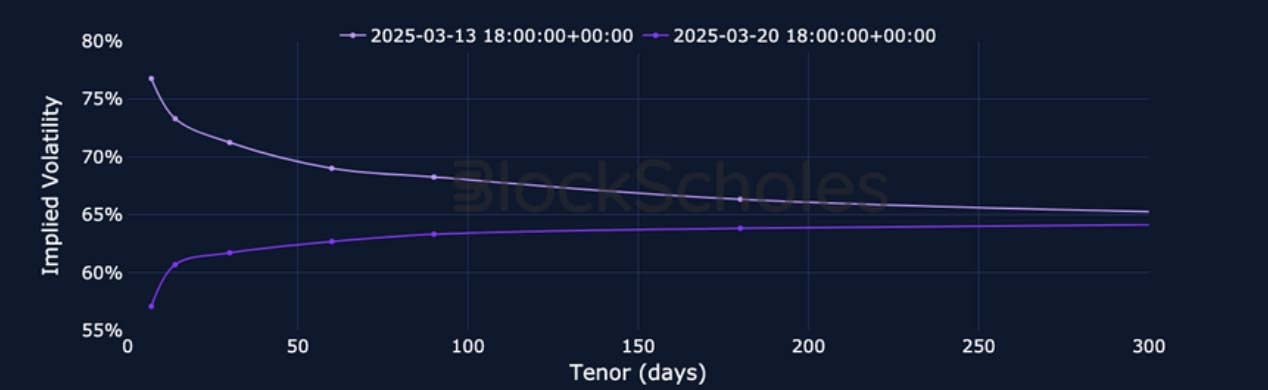

While not delivering a complete recovery rally back to January’s all-time high, this week has at least seen a pause in the intense and persistent collapse in risk appetite. Futures yields continue to fall and funding rates trade negative. However, the skew towards OTM puts priced- in by volatility smiles across the term structure was briefly erased as the lower level of delivered volatility has caused a dis-inversion in the term structure of at-the-money implied volatility. Front-end volatility levels for BTC and ETH trade below 45% and 60% respectively — the bottom of their respective ranges in March.

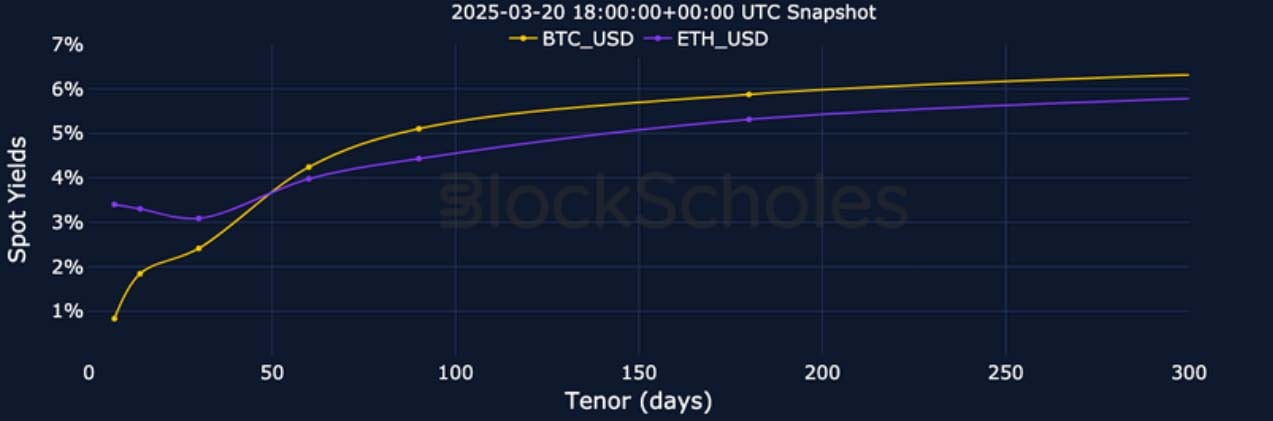

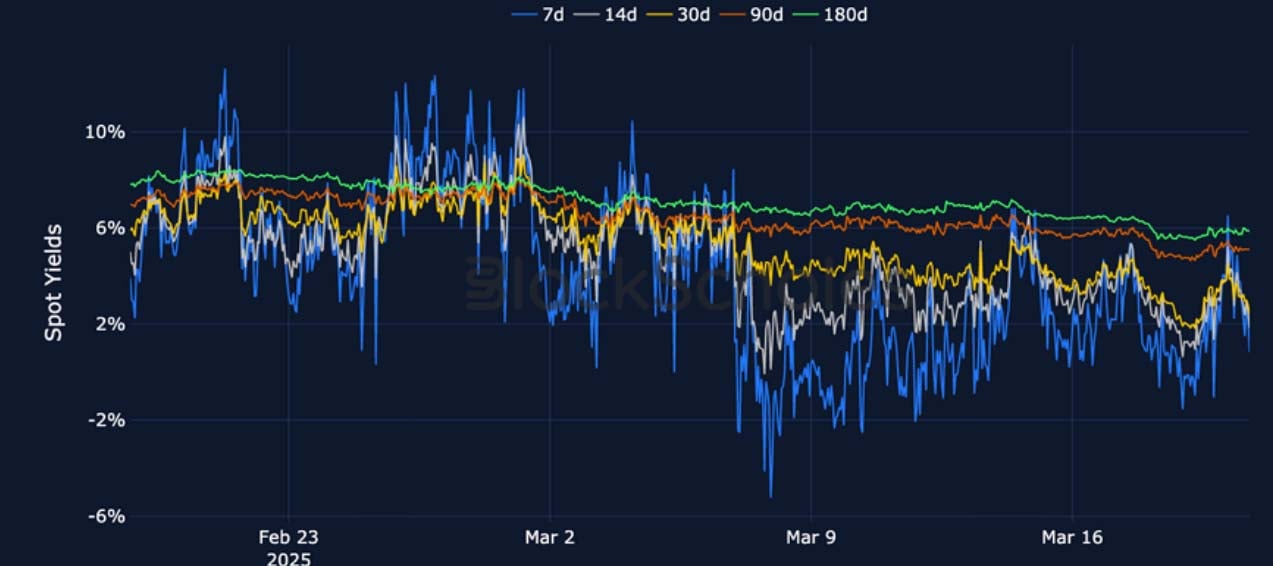

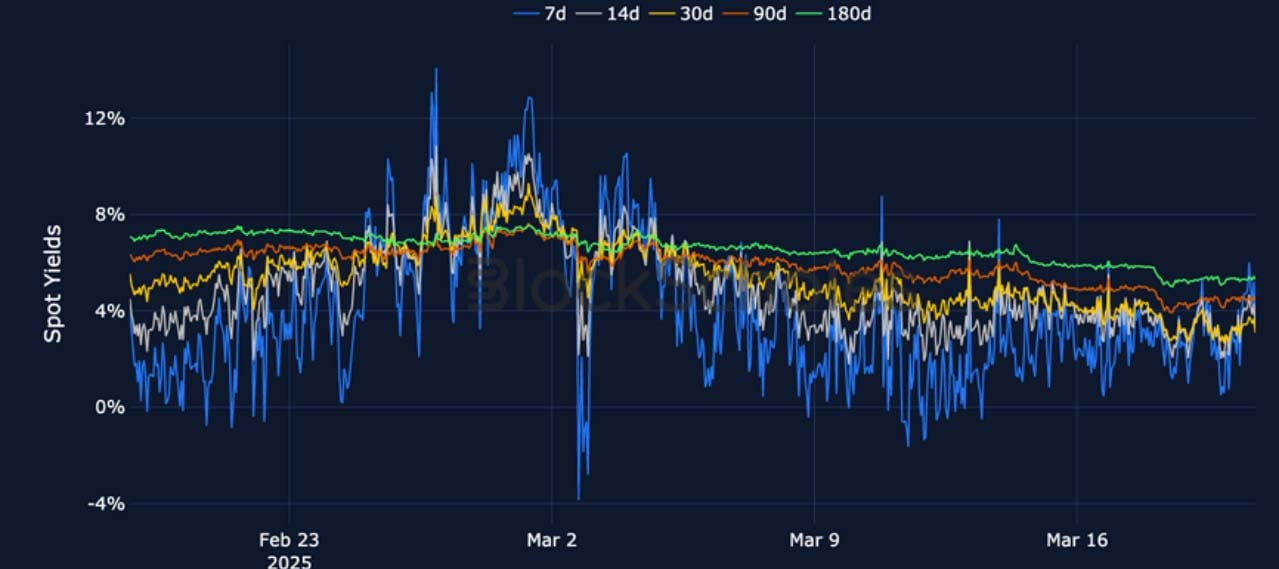

Futures Implied Yields

1-Month Tenor ATM Implied Volatility

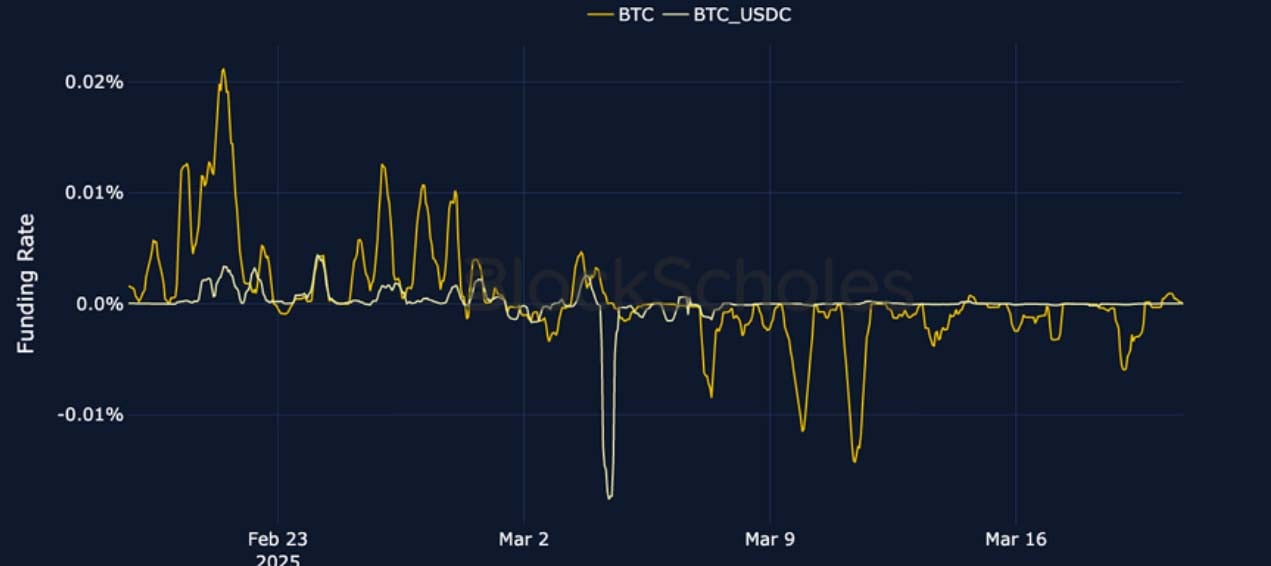

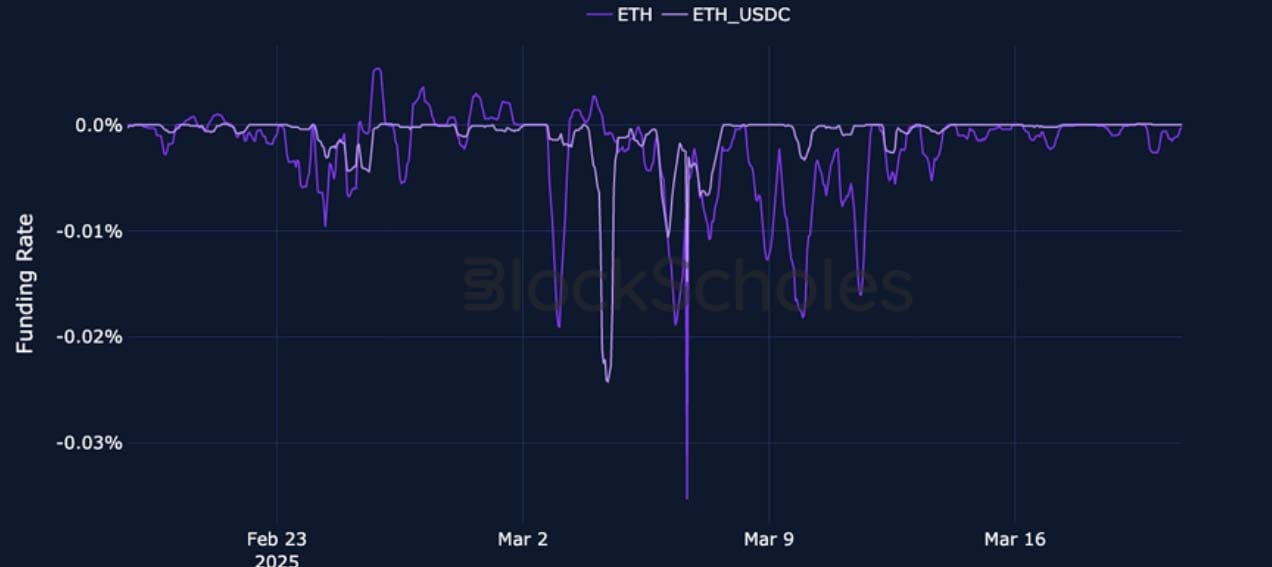

Perpetual Swap Funding Rate

BTC FUNDING RATE – Are reacting asymmetrically to moves in spot: selloffs see a negative rate, but recoveries do not result in a positive rate.

ETH FUNDING RATE – The past week has delivered a far less bearishly negative funding rate than did the selloff in spot prices in the week before.

Futures Implied Yields

BTC Futures Implied Yields – The term structure of futures yields is steepening once again after March’s volatility erased much of the premium.

ETH Futures Implied Yields – Futures with later expirations trade at a similar premium over spot as BTC’s, while the front-end of the curve is 2.5% higher.

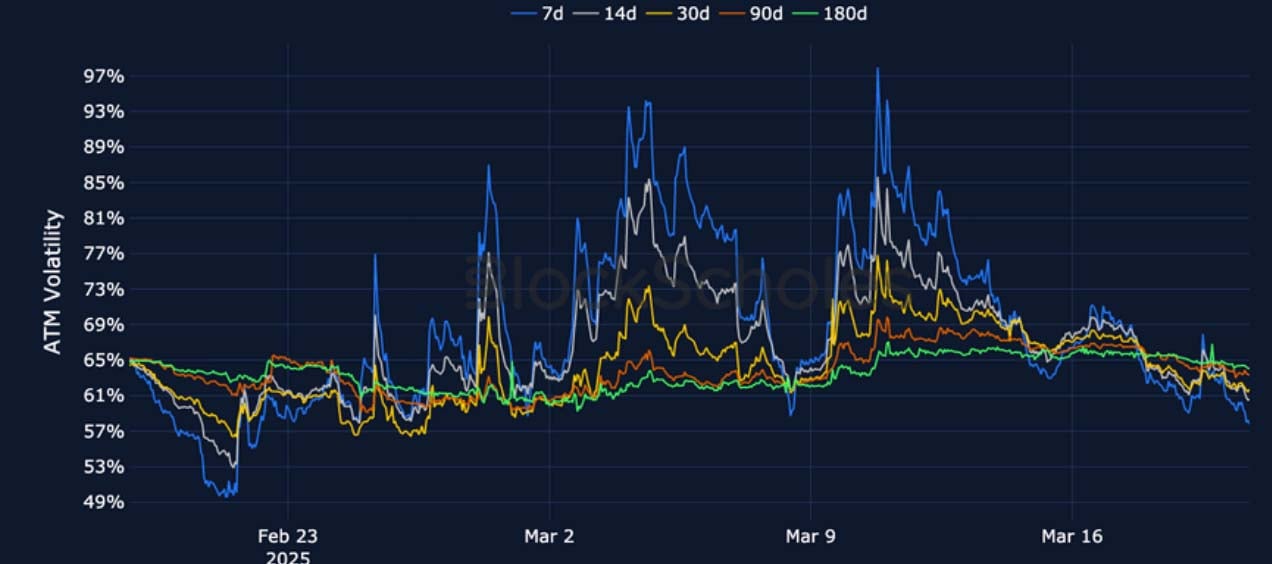

BTC Options

BTC SVI ATM IMPLIED VOLATILITY – Short dated volatility levels fall to 45%, their lowest levels since the period of repeated inversion began in March.

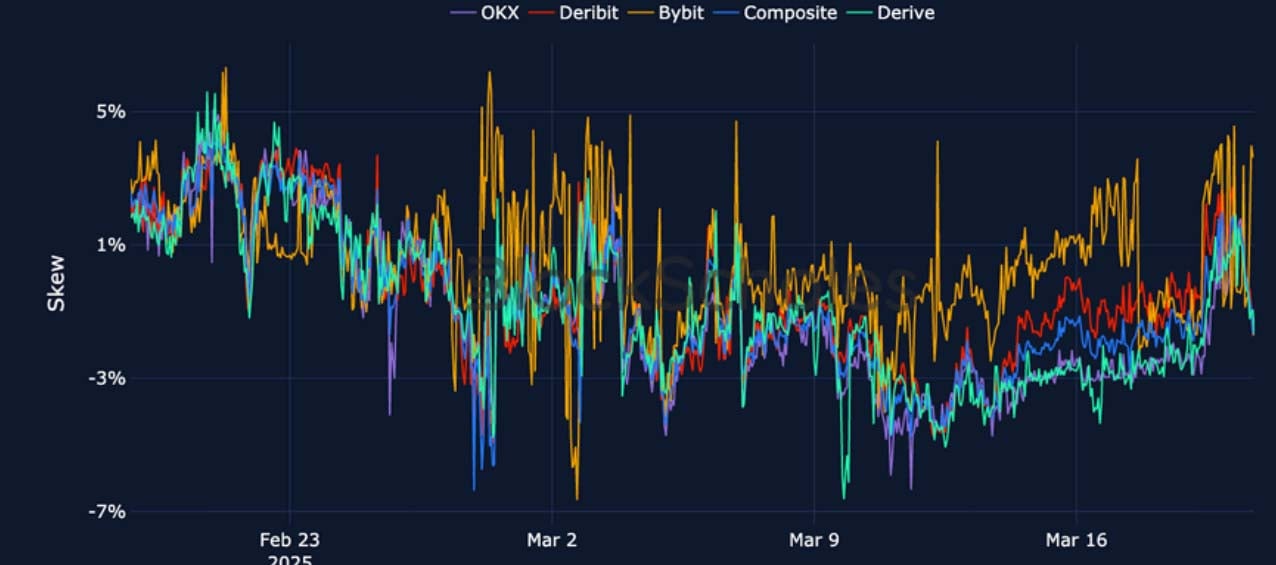

BTC 25-Delta Risk Reversal – BTC’s skew briefly traded positive, in favour of OTM calls, before reversing direction after spot slips back below $85K.

ETH Options

ETH SVI ATM IMPLIED VOLATILITY – The dis-inversion of the term structure continues as 7d tenor volatility falls below 60%.

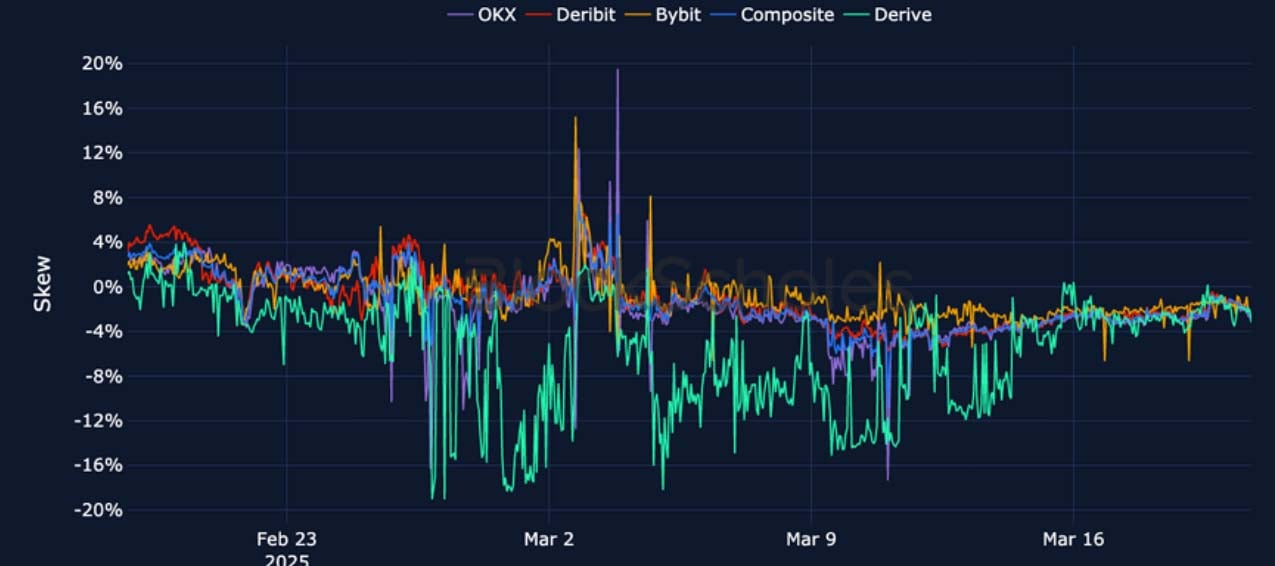

ETH 25-Delta Risk Reversal – Skew recovers from its steeper skew towards OTM puts, but remains tilted towards downside protection.

Volatility by Exchange

BTC, 1-MONTH TENOR, SVI CALIBRATION

ETH, 1-MONTH TENOR, SVI CALIBRATION

Put-Call Skew by Exchange

BTC, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

ETH, 1-MONTH TENOR, 25-DELTA, SVI CALIBRATION

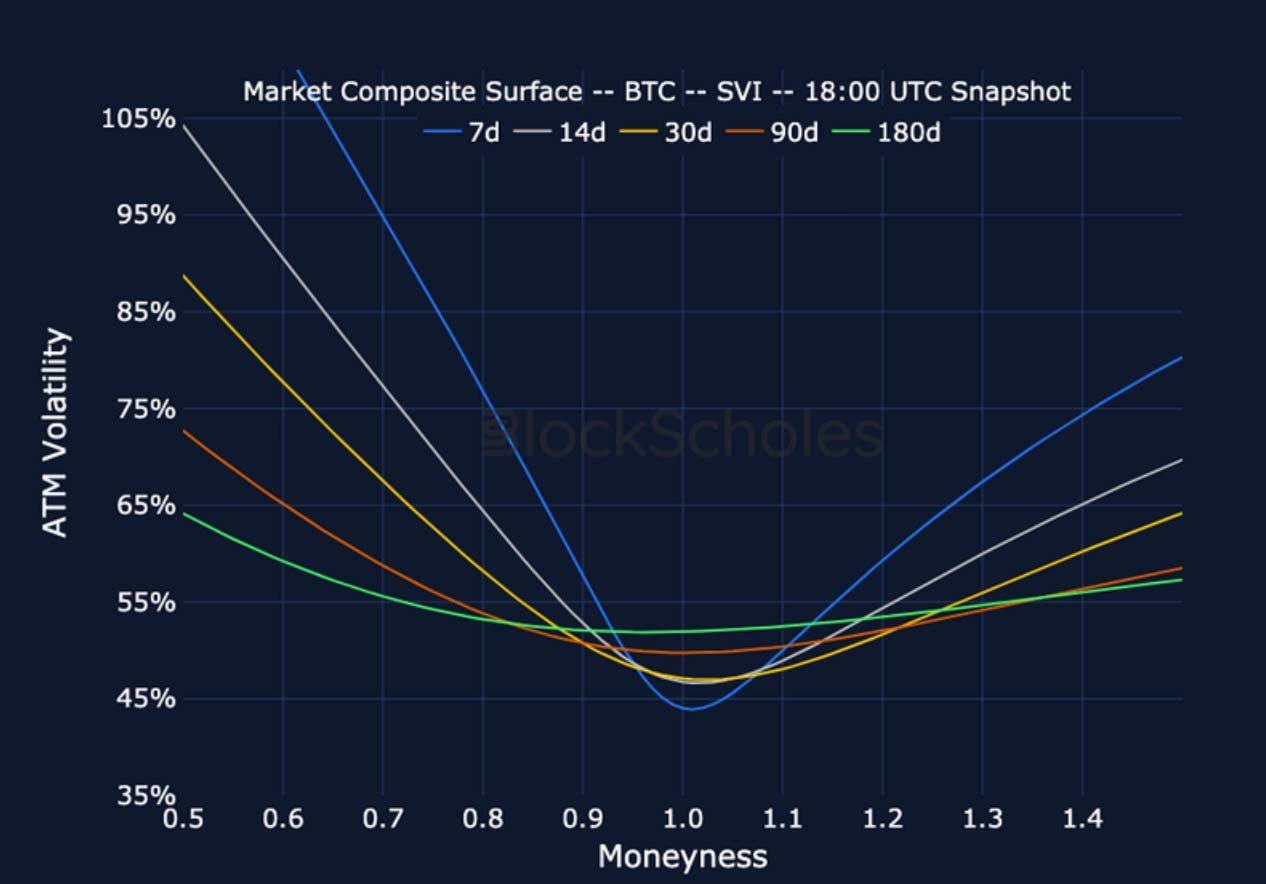

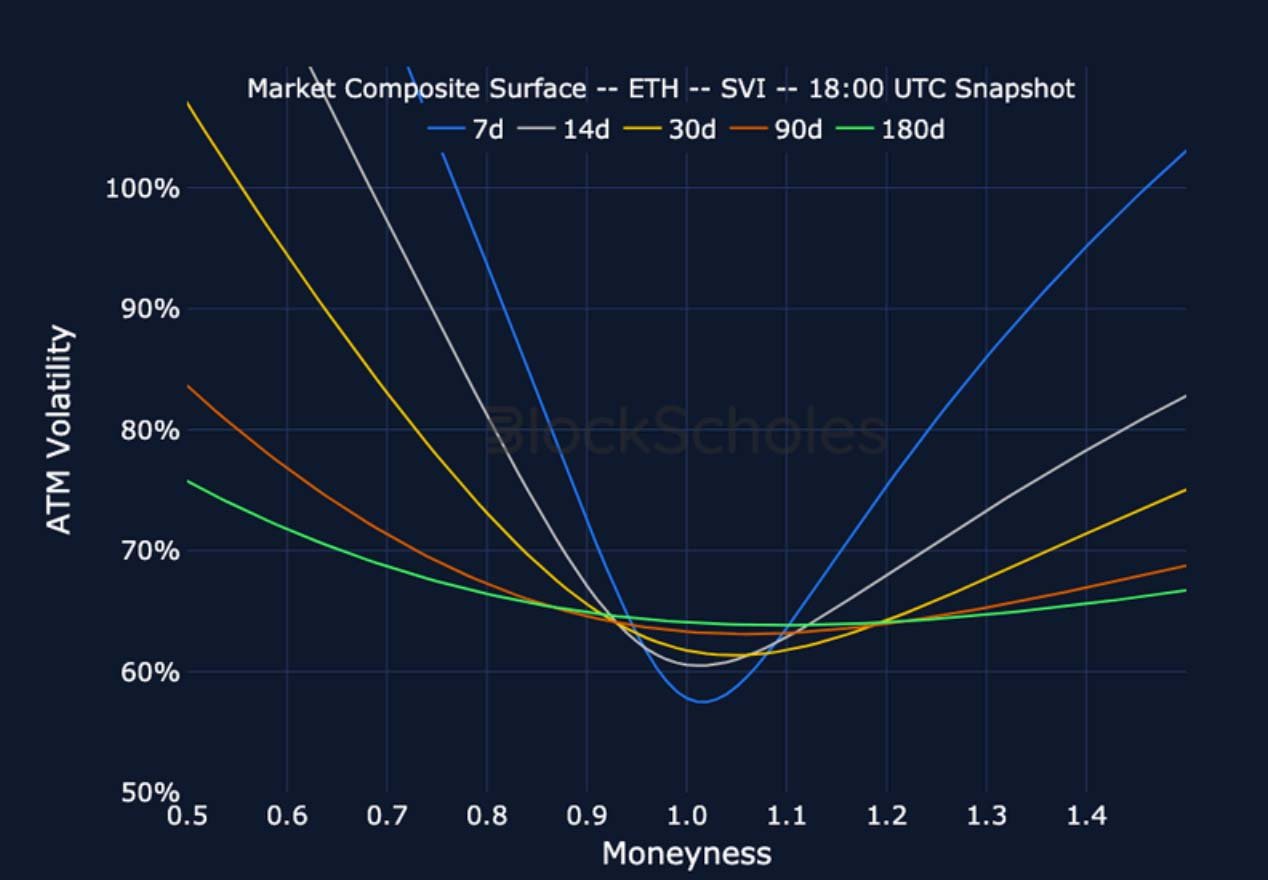

Market Composite Volatility Surface

CeFi COMPOSITE – BTC SVI – 9:00 UTC Snapshot.

CeFi COMPOSITE – ETH SVI – 9:00 UTC Snapshot.

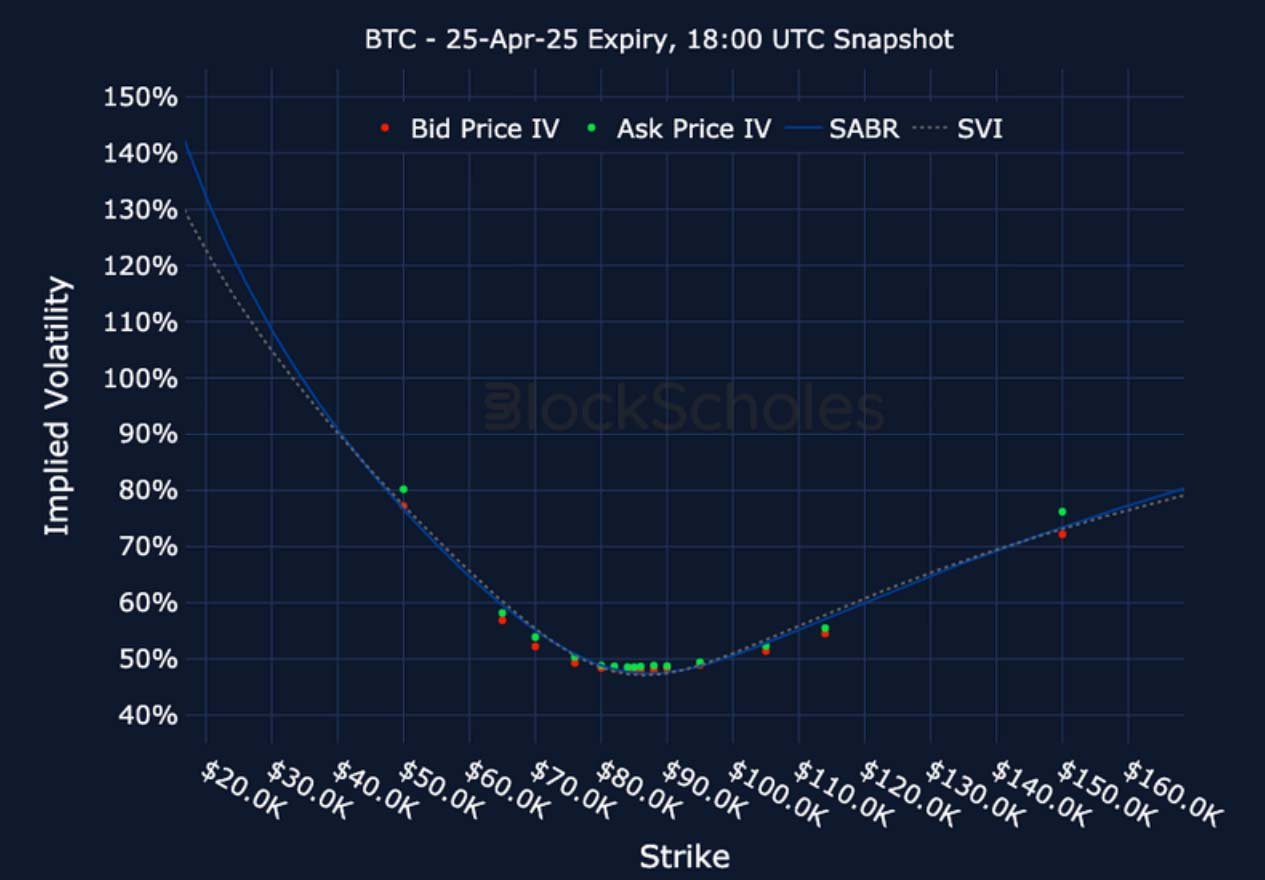

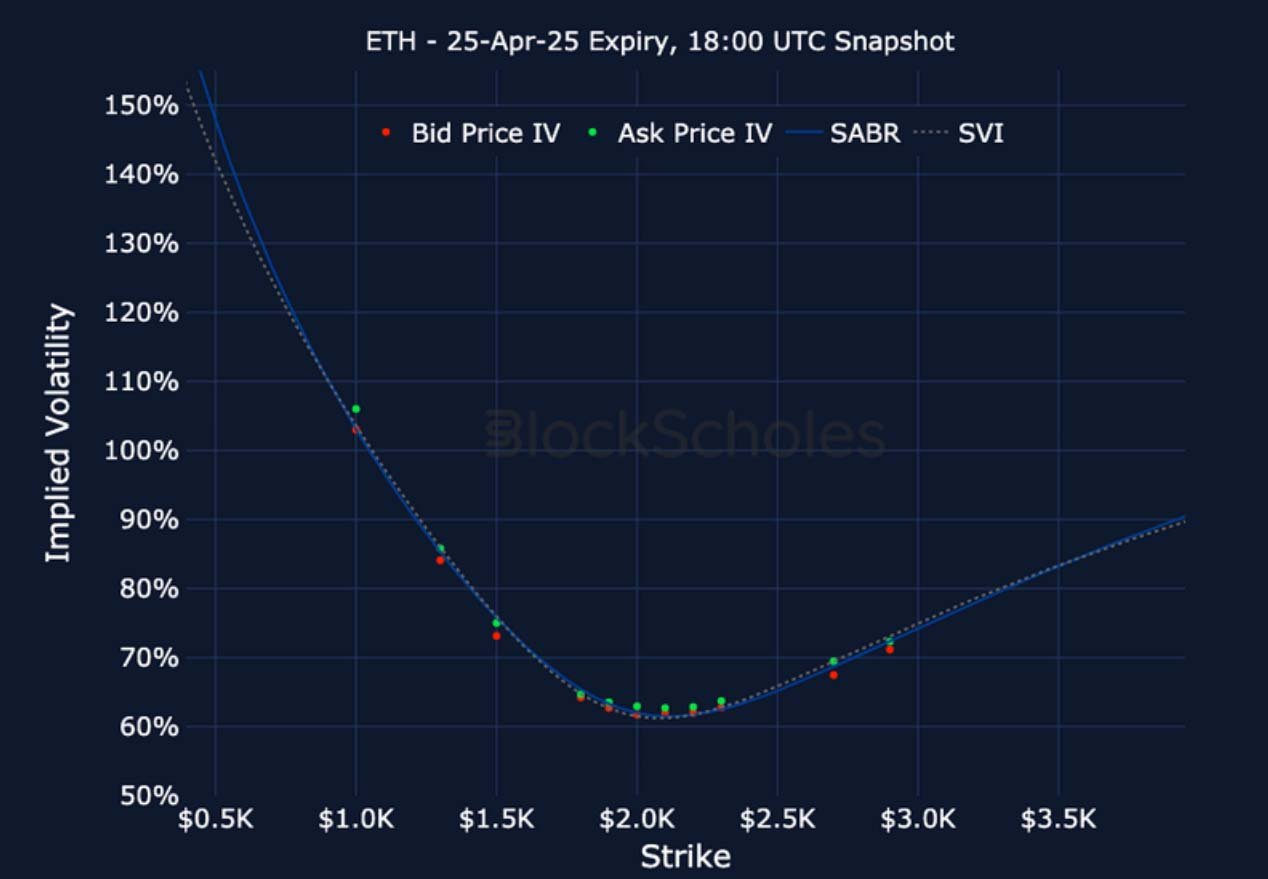

Listed Expiry Volatility Smiles

BTC 25-APR EXPIRY – 9:00 UTC Snapshot.

ETH 25-APR EXPIRY – 9:00 UTC Snapshot.

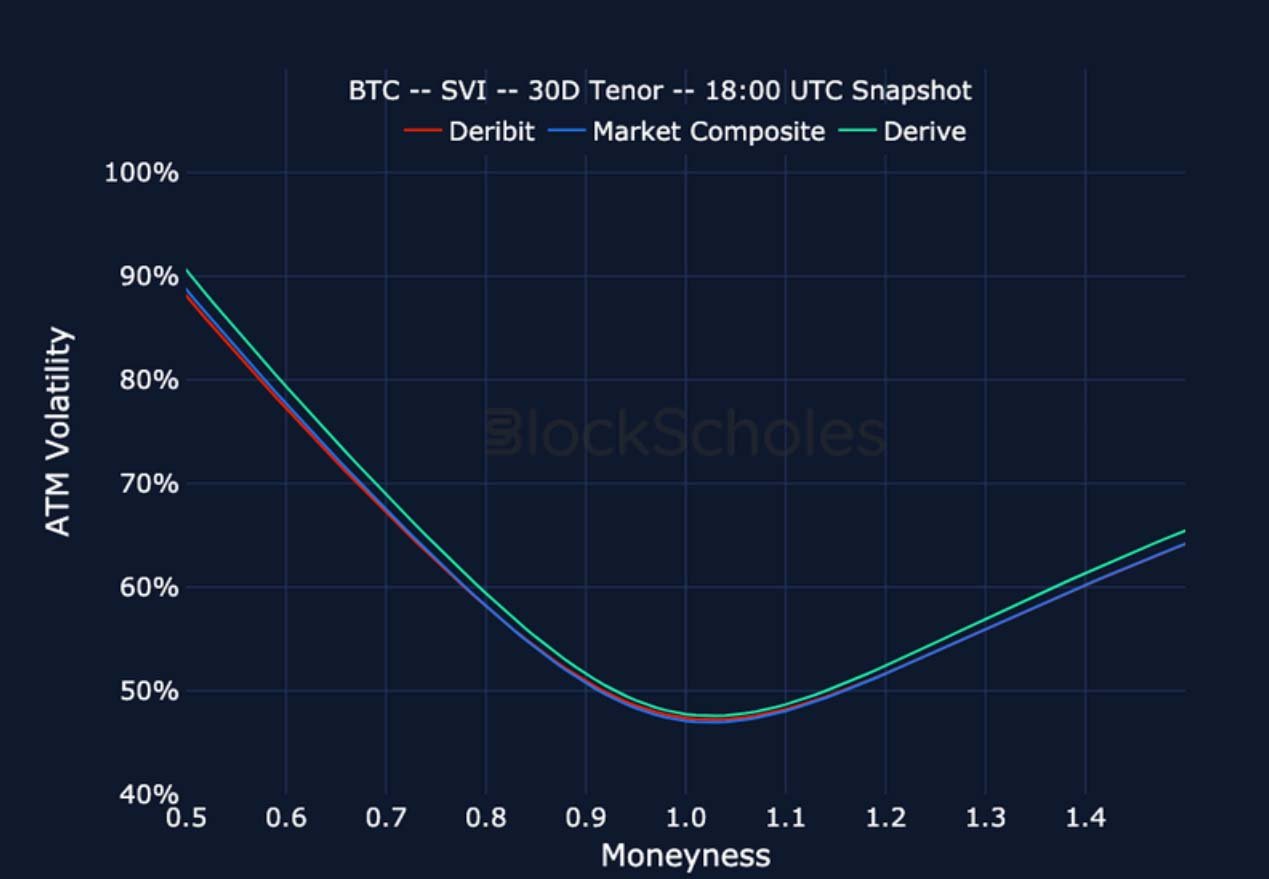

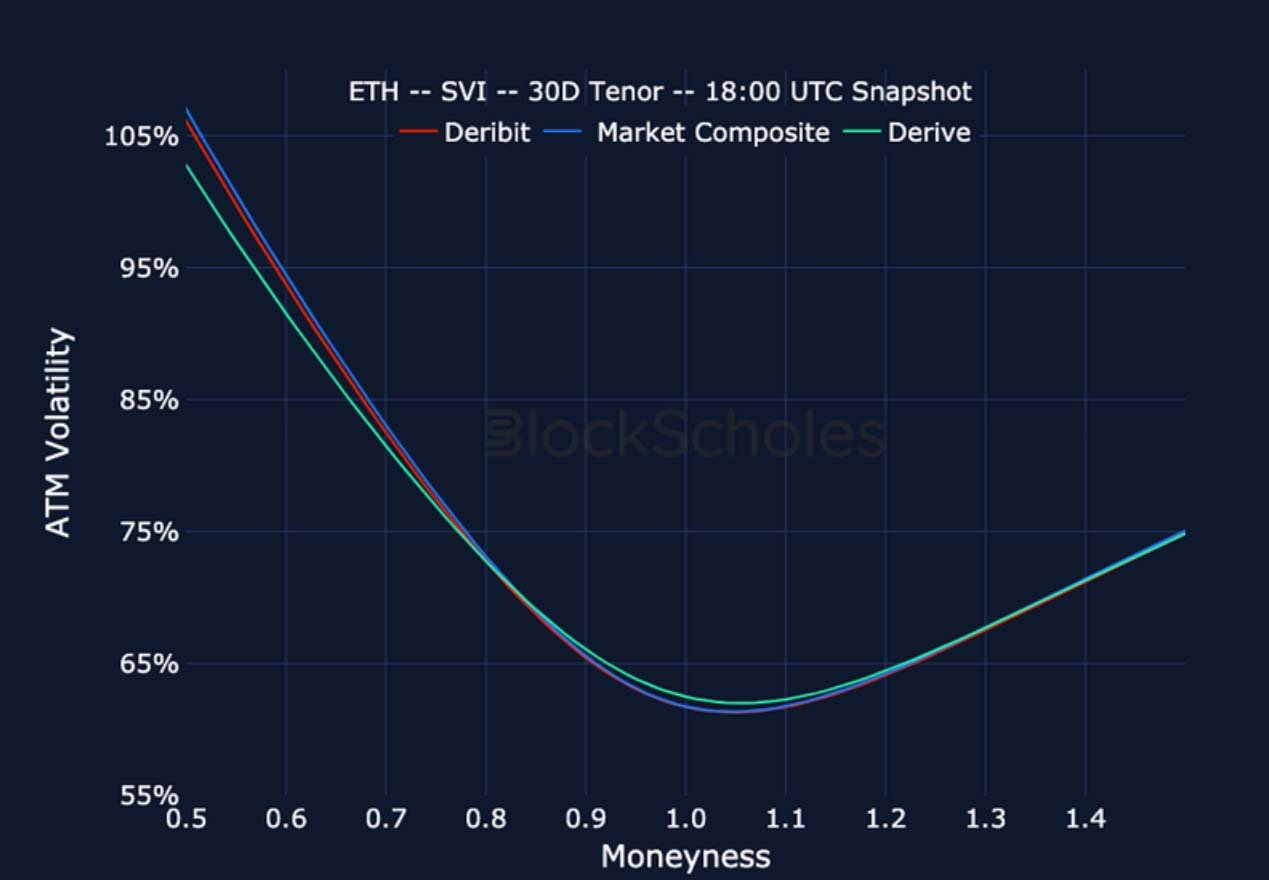

Cross-Exchange Volatility Smiles

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

Constant Maturity Volatility Smiles

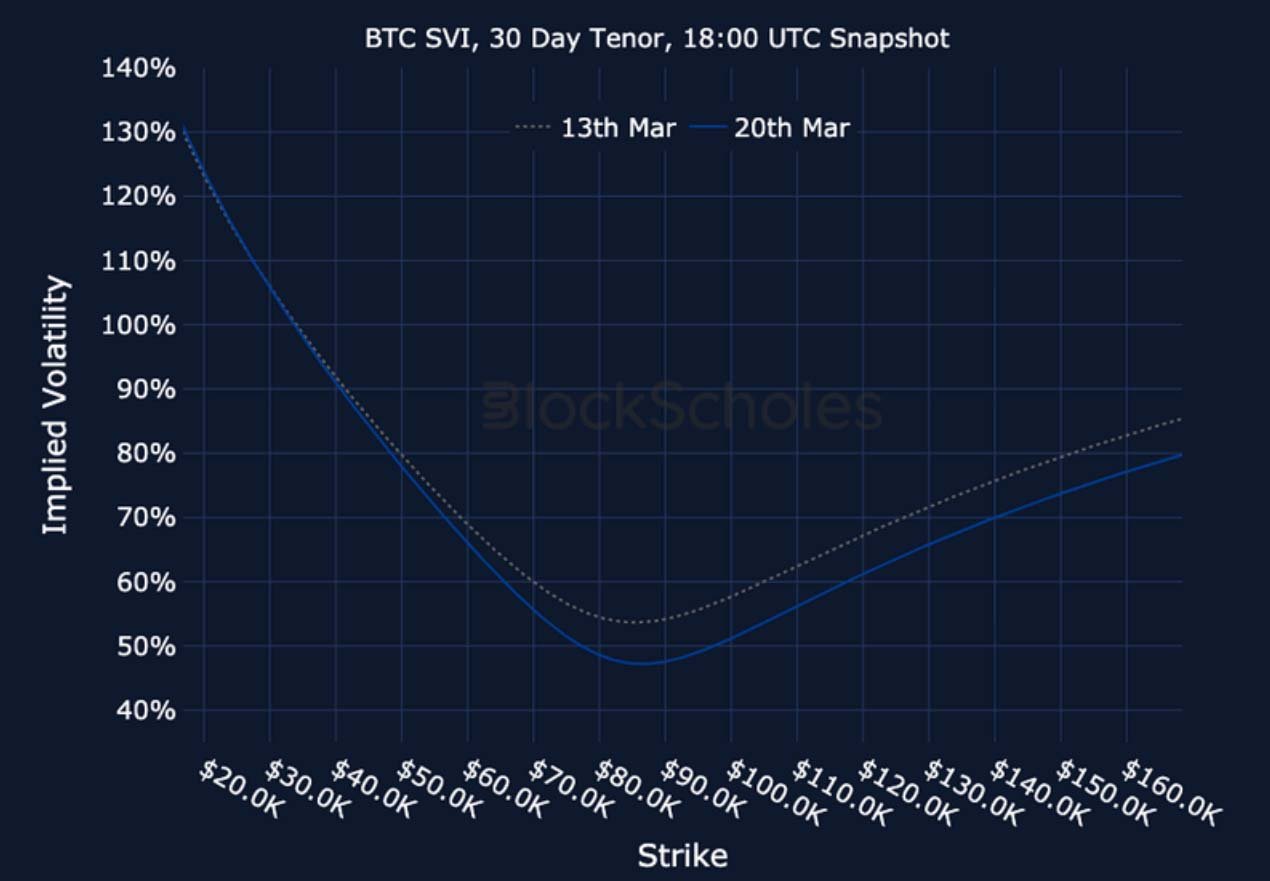

BTC SVI, 30D TENOR – 9:00 UTC Snapshot.

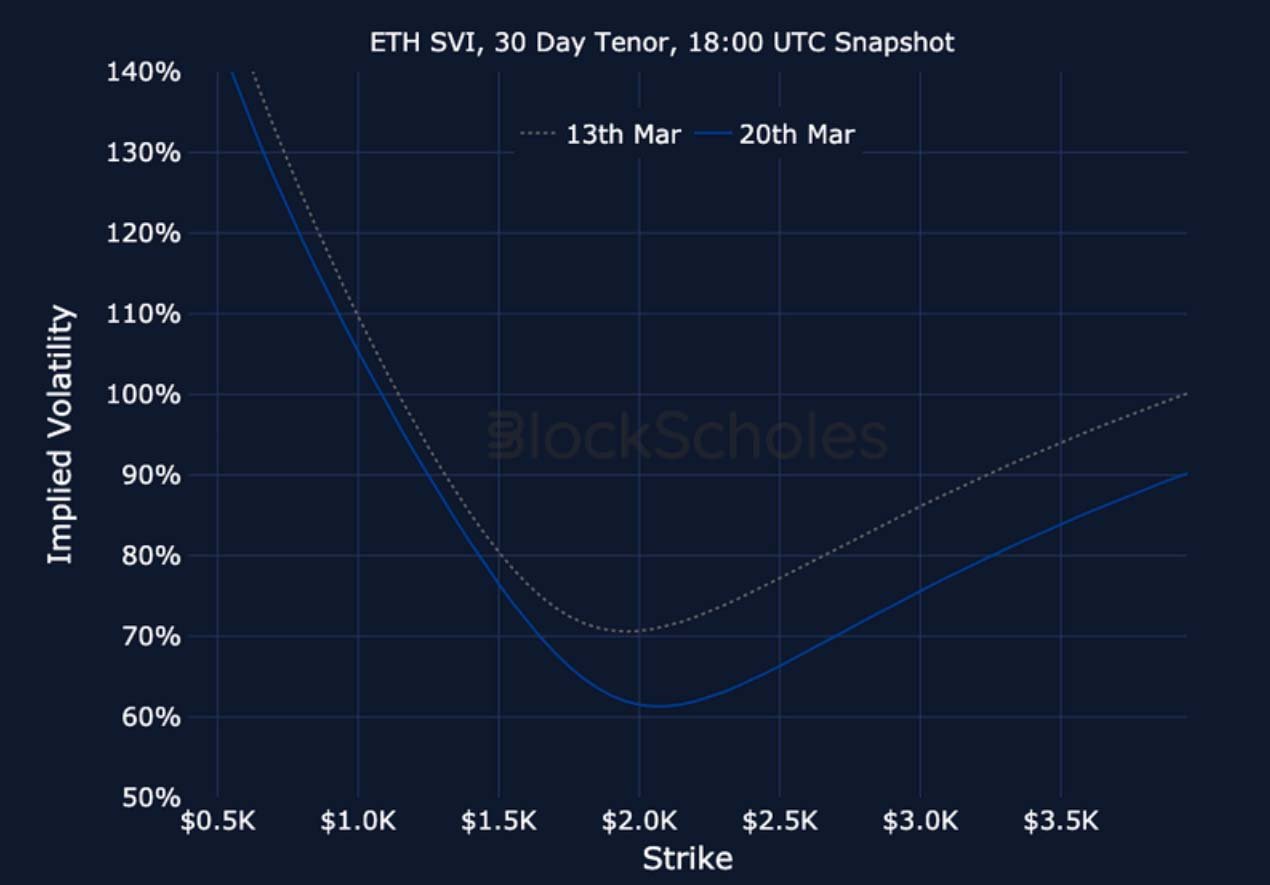

ETH SVI, 30D TENOR – 9:00 UTC Snapshot.

AUTHOR(S)

Trading with a competitive edge. Providing robust quantitative modelling and pricing engines across crypto derivatives and risk metrics.

RECENT ARTICLES

Crypto Derivatives: Analytics Report – Week 12

Block Scholes2025-03-21T11:15:52+00:00March 21, 2025|Industry|

BTC Downside Fear Dissipates

Imran Lakha2025-03-19T14:37:55+00:00March 19, 2025|Industry|

Crypto Derivatives: Analytics Report – Week 11

Block Scholes2025-03-12T08:42:37+00:00March 12, 2025|Industry|

The post Crypto Derivatives: Analytics Report – Week 12 appeared first on Deribit Insights.