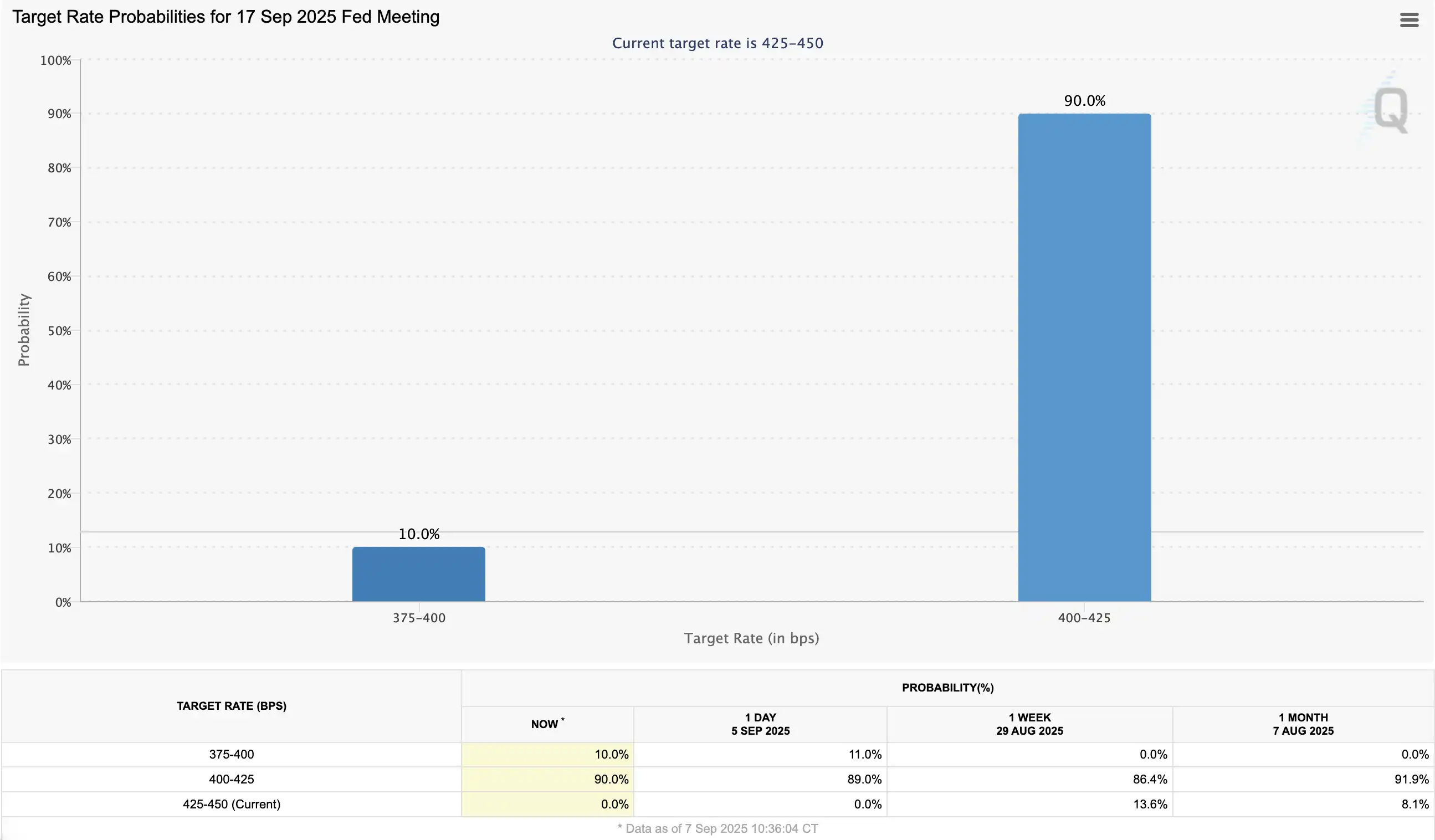

On September 5th, the U.S. Department of Labor released August's non-farm payroll data, which again disappointed the market. The report showed only 22,000 new jobs, far below the expected 75,000. This marked the fourth consecutive month of weak non-farm payrolls, with August bringing the average number of new jobs over the past four months down to just 27,000. The weak data directly prompted a market re-pricing of the Federal Reserve's policy path: expectations of consecutive rate cuts in September, October, and December intensified. According to CME data, the probability of a Fed rate cut soared from 86.4% before the announcement to 100%, with 90% betting on a 25 basis point cut and 10% even betting on a 50 basis point cut.

However, favorable policy expectations failed to boost risk appetite, and U.S. stocks fell slightly, indicating that traders are more worried about the recession risk brought about by the slowdown in economic momentum, and the "interest rate cut benefits" are being overshadowed by the "recession trade."

Next, BlockBeats has compiled traders’ views on the upcoming market conditions to provide some direction for your trading this week.

Bitmine CEO Tom Lee predicts the Federal Reserve will begin cutting interest rates in September, similar to what happened in 1998 and 2024. In both cases, the market subsequently experienced strong rebounds, particularly towards the end of the year. Therefore, Tom Lee offers a "contrarian" prediction, contrary to the prevailing market view: a potential rally in September 2025 is possible.

Trader Dove briefly long on Sol last Thursday and stopped out on Friday. This indicates that BTC has successfully reclaimed $110,000, making it the strongest major currency. Meanwhile, ETH has lost momentum, with its mNAV shrinking (BMNR <1.1, SBET <1), suggesting a market shift toward newer, lower-weighted currencies. If BTC falls below $110,000, the strategy will become ineffective.

Companies are producing more orders with fewer people, but a month later the same logic of first worrying about a recession and then gradually regaining confidence is repeated. The non-farm payroll figures are significantly lower than expected, leading to concerns about a recession. After a few days of recovery, people feel that the economy is actually fine.

The logic from a month ago still applies. Two new insights emerged this week: 1. The manufacturing and service PMIs released this week were both strong. More notably, the order indices for both significantly exceeded expectations. (The chart below shows the service sector on top and the manufacturing sector on the bottom.) This significant improvement in industrial orders doesn't indicate a recession in any way. However, how can we explain the decline in hiring? The previously discussed structural changes in the labor market brought about by technological change are becoming a reality. With rising productivity, companies are achieving more output with fewer people. This may be the norm in the AI-era economy. With increased labor productivity, companies are increasingly employing fewer people.

Both of these events, like the previous Jackson Hole symposium, increased the likelihood of a rate cut, but at the expense of an economic downturn. Markets often experience initial excitement followed by a cooling of the market, and this is also true for the US stock market, with the economic impact being even more significant. While bad data can be treated as good data, it is still bad data. Economic problems are likely to point to a recession. If this happens, it will be the "final drop." If it doesn't, the probability is for a continued decline.

Therefore, the economic problems are more serious than the interest rate cut itself. Simply put, interest rate cuts aren't always positive; they must be considered in conjunction with the economy. If they're cut out of concern for the economy, it's likely not a positive outcome. Rate cuts are only one factor; the more crucial factor is the policy response to the economic downturn. Historically, the 2020 recession lasted only two months, with the S&P 500 recovering its losses within six months and reaching new highs for seven consecutive months, demonstrating that recessions don't necessarily lead to long-term declines.

My personal strategy remains unchanged: I plan to reduce my holdings in smaller cryptocurrencies, retain mainstream ones, and hold onto cash, waiting for buy the dips opportunities. If the market declines, I'll increase my holdings; otherwise, I'll continue to enjoy the gains from rising mainstream prices. Data shows a significant drop in BTC turnover, indicating that most investors are choosing to wait and see. Until the outcome of the negotiation between Trump and the Federal Reserve becomes clear, more investors are staying on the sidelines.

Although the unemployment rate did not rise significantly in this employment data, the non-farm payroll data in August dropped significantly. As I said in the previous interpretation, this was caused by the decline in the supply side of the employment market.

So the current situation is that weak employment is not only caused by a decline in demand, but also a significant reduction in corporate supply, which means that companies are cautious about expanding. This situation is a response to insufficient economic confidence.

After the data was released, Trump again said that the Fed needed to cut interest rates. At the same time, Bessant said that the Fed's ability to manage the economy had failed. The market then interpreted this situation as a deterioration in employment, and the Fed's management of employment had failed.

This is what I was worried about before. Once confidence in the economy is insufficient, a 25BP rate cut, or even a 50BP rate cut, is "poison". Once economic risks are expected, such as stagflation, recession, etc., the more severe the rate cut in September or this year, the less confidence the Fed has in the economy, and panic expectations will gradually spread.

At this time, the probability of a 50BP rate cut in September has increased again to 11.8%. Although it has increased slightly compared to the release of the employment data just now, if confidence in the economy cannot be restored and market concerns about a possible economic crisis cannot be weakened, the higher the 50BP rate cut, the more negative the effect will be.

However, judging from the current situation, concerns about short-term expectations have emerged, but panic is not yet a cause. It depends on the sentiment next week.

The altcoin is still fluctuating and has not experienced a big drop, mainly because Ethereum has not fallen below the limit, so it can maintain the fluctuation between 280-310b.

The volatility here is similar to that in September and October 2024. Generally speaking, there is not much long-term analysis worthy of attention. The short-term analysis is to make profits through swing trading within the range.

Yesterday's sharp decline in the non-farm payrolls made a September rate cut a foregone conclusion, which is generally a positive development. As for the risk of a recession, I believe it remains relatively low (unemployment hasn't increased significantly). However, there is an overall expectation of a US stock market correction in September (statistically, this is unrelated to a recession), so Bitcoin may adjust along with the US stock market. If this happens and the price falls below 100,000, I still believe the bottom will be between 93 and 98.

If the adjustment of the US stock market does not occur or does not cause a sharp drop in Bitcoin, then 107 may have bottomed out. From a technical perspective, the short-term focus is on the 11w area.

As it is generally expected that there will be several consecutive interest rate cuts, the market conditions in October and November should be favorable, which is also in line with our prediction that the unspeakable will occur between October and November.

BTC Markets analyst Rachael Lucas stated that the weak US jobs report did fuel expectations of a more dovish Federal Reserve stance, which typically supports risk assets like Bitcoin. However, the market has already priced in some policy easing. Meanwhile, we are seeing institutional investors taking profits, while ETF flows have remained relatively flat. Bitcoin faces resistance at $113,400, with further resistance at $115,400 and $117,100. A break above these resistance levels would suggest the market has priced in recent selling pressure and is poised to retest highs.

Twitter: https://twitter.com/BitpushNewsCN

BitPush TG discussion group: https://t.me/BitPushCommunity

Bitpush TG subscription: https://t.me/bitpush