In this episode, Lex interviews David Namdar, CEO of BNB Network Company, starting with his early exposure to Bitcoin in 2012, moving on to co-founding Galaxy Digital, and his current role leading BNB Network Company. Namdar reviews the evolution of the interaction between traditional public markets and crypto assets, pointing out how regulatory hurdles and speculative cycles have shaped market participation.

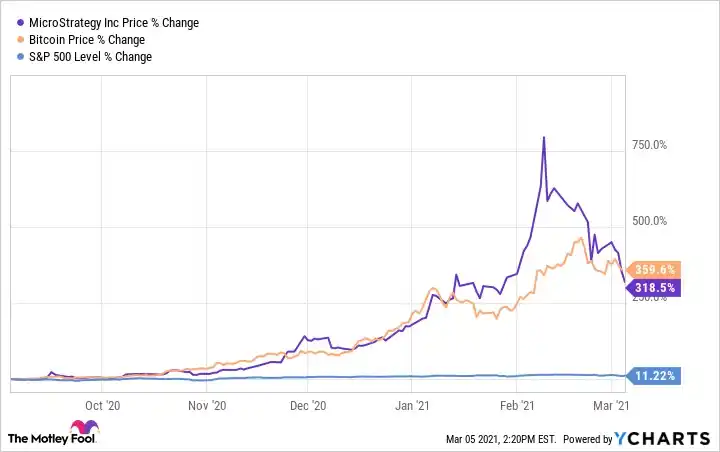

He further analyzed the rise of Digital Asset Treasury (DAT) companies, and specifically highlighted how MicroStrategy, under the leadership of Michael Saylor, pioneered this model: converting $400 million in cash into Bitcoin, which now holds over $75 billion in Bitcoin.

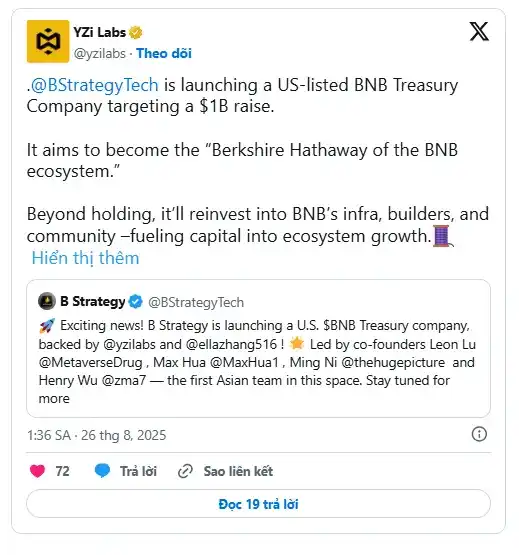

They then discussed Binance's role in this ecosystem: with 290 million users, accounting for approximately 40% of global crypto trading volume, and through a quarterly burn mechanism of up to $2 billion, it has made BNB a deflationary asset.

Finally, Namdar shared why he chose to focus on BNB rather than Bitcoin in the new DAT project, providing US investors with an exposure to a previously severely undervalued yet powerful asset.

TL;DR

1. Digital asset vaults are becoming "disguised crypto ETFs".

Publicly traded companies like MicroStrategy and MetaPlanet are shifting their balance sheets to crypto asset holdings, providing indirect exposure to assets such as Bitcoin, Ethereum, and BNB. With ETFs or direct investment channels limited, this model is attracting billions of dollars in inflows, becoming a new investment avenue.

2. BNB has a huge global usage, but it is severely "undervalued" in the US market.

With 290 million users and a quarterly token burn of up to $2 billion, BNB is one of the most widely used tokens globally. However, it remains virtually inaccessible to US investors, creating a significant disconnect between market awareness and asset demand, thus generating potential opportunities for public market investment vehicles surrounding BNB.

3. Cryptocurrency market trends often rely on misunderstood and unsustainable incentive mechanisms.

Namdar points out that past cycles of demand inflation were driven more by staking rewards and nominal yields than by genuine value creation. A lack of economic and financial literacy has fueled the pursuit of "superficial gains," obscuring underlying fundamentals and thus undermining long-term sustainability.

Who is David Namdar?

David Namdar's career trajectory to becoming CEO of BNB Network almost perfectly encapsulates every key stage in the development of the crypto industry. Starting with traditional finance jobs at UBS Hong Kong and Millennium Management, he discovered Bitcoin in 2011 and became one of the earliest evangelists, attending one of the earliest offline Bitcoin gatherings in New York in 2012–2013.

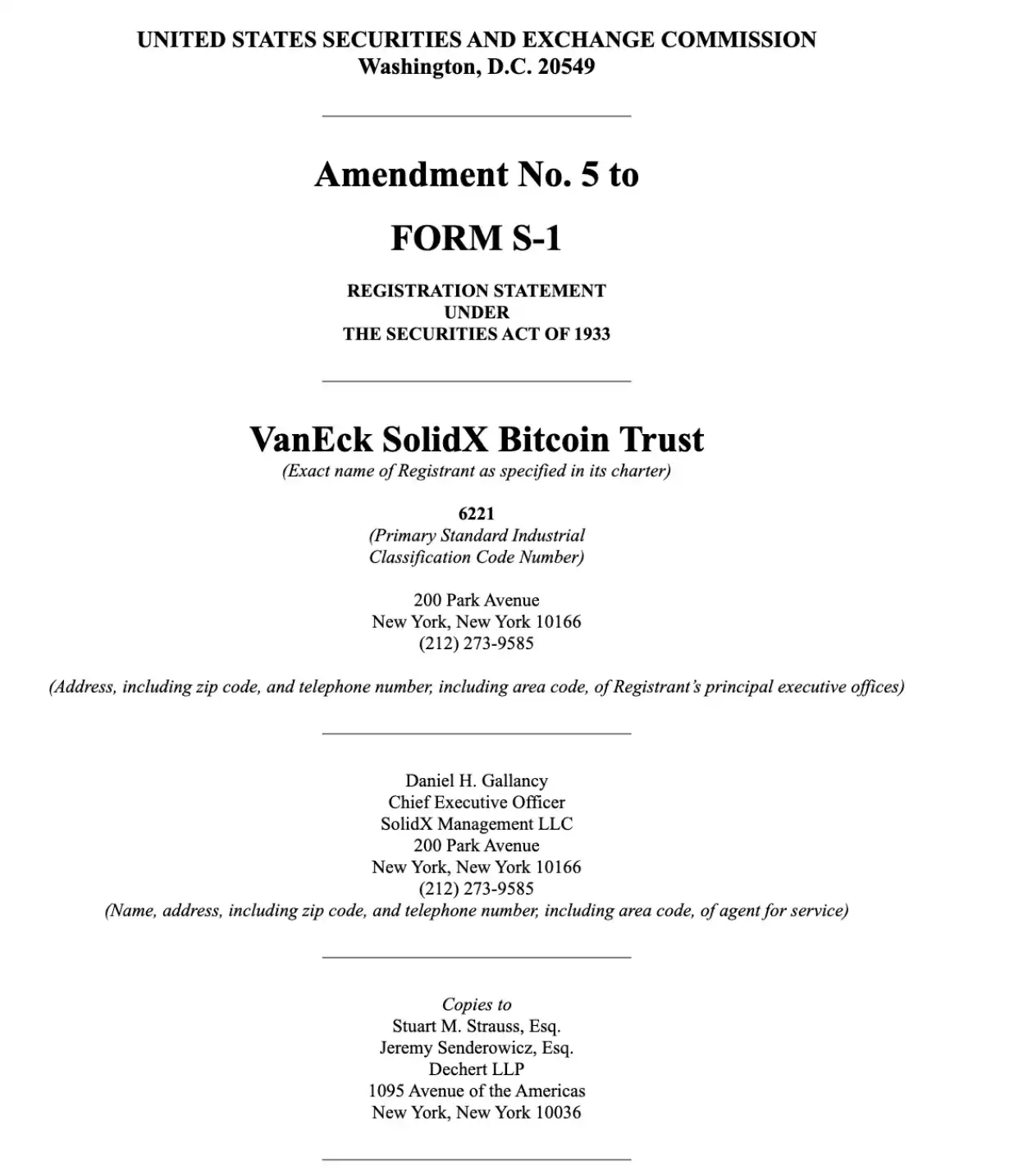

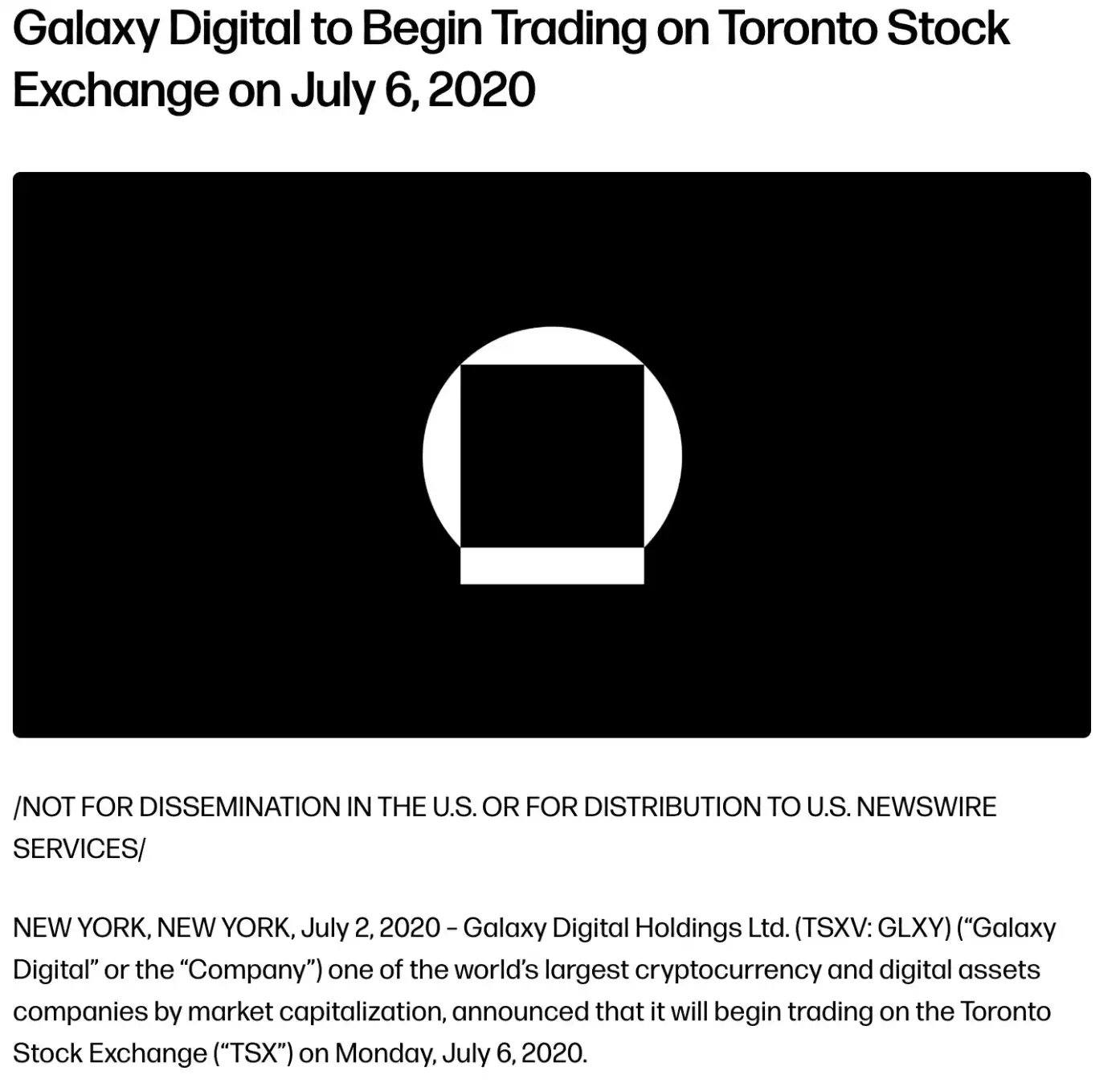

In 2014, he co-founded SolidX Partners, submitting the world's second Bitcoin ETF application within weeks of the Winklevoss brothers' submission. Then, in 2017, he partnered with Michael Novogratz to found Galaxy Digital, which successfully listed in Canada.

After leaving Galaxy, he founded Coral DeFi, co-founded NFT.com, and became an active angel investor, while also advising several digital asset treasury companies. With this unique combination of experience spanning Wall Street trading, early-stage crypto startups, and institutional-grade digital asset management—over a decade of experience from the infancy of Bitcoin to the institutionalization of crypto—he became the ideal candidate to lead BNB Network's ambitious $500 million treasury strategy in 2024.

Excerpt from the dialogue

Lex Sokolin: Hello everyone, welcome to today's conversation. I'm very pleased to have David Namdar with us. He is the CEO of BNB Network Company, one of the original co-founders of Galaxy Digital, and a very early crypto entrepreneur and investor. David, welcome to our conversation.

David Namdar: Thank you, Lex. It's great to be here.

Career Development

Lex Sokolin: Let's start with a quick recap: How did you get into the crypto space? And what led you to become the co-founder of Galaxy? What were your early years like?

David Namdar: Actually, that wasn't the first chapter of my career in the crypto industry. The real starting point was UBS in Hong Kong.

At the time, I was responsible for covering the entire Asian market and conducting global trading. Later, I returned to New York to work for Millennium, one of the world's largest hedge funds, where I started trading in almost every stock market. It was then that I realized Asians seemed to have an advantage over Westerners when it came to "currency": ordinary people in Hong Kong, Tokyo, and Shanghai were exposed to and thought about multiple currencies every day, while in the West, people only needed to care about the US dollar or the euro, and everything worked too smoothly.

It was at Millennium that I first encountered Bitcoin. I started attending some of the earliest Bitcoin meetups in New York, around 2012 or 2013, trying to convince my colleagues in hedge funds and banks to take notice. But when I saw their resistance, I chose to leave. In late 2013 or early 2014, I founded my first company in this field.

David Namdar: That company is SolidX Partners. Our initial goal was to create a boutique investment bank focused on digital assets. At the time, we were trying to launch a Bitcoin ETF—the second Bitcoin ETF application globally, after the Winklevoss brothers. Simultaneously, we were also experimenting with derivatives, using total return swaps, and publishing some of the earliest research reports on Bitcoin and digital assets, analyzing them as institutional-grade asset classes.

All of this happened between 2014 and 2015, which, frankly, was a bit early. Especially after the Mt. Gox crash in 2013, many people still had doubts about this field, feeling that the risks were too great and there were too many problems. Many others believed that governments would shut down Bitcoin directly, and that Bitcoin would never be what it is today.

A few years later, I met Mike Novogratz. He had just left Fortress to focus on managing his family office. He had made several investments in this area, including Ethereum and Ripple, which I had met through Dan Morehead of Pantera, whom I knew from my time at Fortress.

David Namdar: So I started managing all his digital assets, and to be honest, I continued doing what I do best: creating chaos, expanding opportunities, and dragging everyone into the crypto world step by step. In the family office, I was basically "fighting everyone," constantly pushing him and the entire team toward crypto, getting them deeper and deeper into it, and planting the seeds for the hedge fund and business we would later co-found, which eventually became Galaxy Digital.

After that, I pushed for us to take the company public. But the regulatory environment in the US at the time didn't allow us to go that way, so we turned our attention to Canada. Several crypto mining companies had already gone public in Canada, and the local market was more open to crypto assets. Some Canadian investors even compared crypto mining to mining traditional gold, silver, or other commodities, and were therefore more willing to accept this asset type earlier.

Therefore, we became one of the first teams to bring "a truly diversified crypto investment bank and crypto business" to the public market. You could say that this publicly traded company is an enlarged and evolved version of my first company, SolidX.

Lex Sokolin: That's a lot of work done in a very short time, thank you for sharing. I'm actually very interested in public markets because it touches on the topic of digital asset treasury. What motivated you to go public? Companies usually go public to provide liquidity to shareholders, but for a company like Galaxy, why did you decide to list on a Canadian exchange? Also, how do you view the market structure of that exchange? After all, it wasn't Nasdaq, was the liquidity sufficient at the time? Was that important? What were the key considerations?

David Namdar: That's a very good question. Let me go back to SolidX. One of the challenges SolidX faced at the time was that, after the financial crisis, we were trying to launch a Bitcoin ETF, with the goal of creating a product that retail investors could trade, while institutional investors could also manage creation and redemption on their ETF desktops.

David Namdar: The problem was that the market was too early at the time, and people didn't see the opportunity. Instead, they were overly concerned about the risks of Bitcoin as the underlying asset for the Total Return Swaps we were trying to implement. Another obstacle was ISDA. This is an internationally recognized standard for derivatives contracts, and banks were unwilling to deal with a small startup on these ISDA protocols.

If SolidX had become a publicly traded company earlier, and if the market environment and opportunities had allowed, these problems might have been solved, and SolidX might have been able to successfully bring its products to market.

Returning to Galaxy Digital, when we consider the company's business layout in trading, investment banking advisory, and other areas, as well as the different segments that can be expanded in the future, we realize that it must have credibility in the public markets and be able to use public market capital to drive business growth.

David Namdar: Now, almost a decade later, we see more and more companies being able to raise significant amounts of money in the private market. But back then, whether it was gaining market recognition, attracting clients and doing business with large institutions, or raising funds through the public market, these were the core factors driving our decisions.

Lex Sokolin: Next, could you review the situation over the past few years, especially in the US public markets? I'd like to explore how market attitudes have changed from fintech to digital assets, and then to cryptocurrencies and DeFi. What has been the comfort level of people in holding and managing these assets, and what generational differences have emerged? Also, what has been the overall sentiment towards these assets in the US public markets? This is a big question. I'm thinking of the SPAC boom of 2021 and 2022, the wave of fintech company listings and IPOs, and the early stages of crypto trading platforms and brokers trying to access the capital markets. Could you outline the evolution of the US capital markets towards this asset class and related sectors?

David Namdar: Absolutely, and this is a topic I really enjoy revisiting. I remember our first meeting was sometime between 2016 and 2018, a crucial stage in the market's evolution. Unfortunately, one of the key factors hindering this process was the heavy regulatory environment. Many in the industry, including myself, believe that the NYDFS's BitLicense regulations, along with Ben Lawsky's policies, severely slowed and stifled innovation, causing a large number of crypto companies and capital to avoid New York, and even the United States altogether. This impact was very evident in 2017, 2018, and 2019, and arguably continues to this day.

During the ICO boom of 2017 and 2018, some companies, such as Galaxy and some mining companies, did successfully go public, but the overall environment remains challenging.

David Namdar: At the time, Bitcoin and Ethereum practically became the "fundraising currencies" of the entire digital asset world. People had to buy Bitcoin or Ethereum to participate in various ICOs and the ever-emerging projects in the crypto ecosystem. As a result, many companies that raised large amounts of Bitcoin in ICOs would choose to hold those Bitcoins, and as the price of Bitcoin rose, their paper profits would also increase, and the same was true for Ethereum.

Therefore, ICO projects and the companies receiving investment have effectively become speculators of the underlying assets. As more and more people buy Bitcoin and Ethereum to participate in these projects, and these projects appear profitable on paper, a "reflexivity" effect is created, driving further leverage in the market. These activities mostly occur in the private market; similar situations are rare in the public market.

Around 2021, with the rise of DeFi, the situation changed. People no longer entered the crypto world solely through Bitcoin and Ethereum; instead, various new channels emerged, allowing investors to invest through stablecoins.

David Namdar: At that time, Tether began to expand rapidly, Circle became increasingly popular, and other large crypto assets also emerged, providing access to the crypto world through these channels. Simultaneously, a similar leverage effect emerged in the market: new projects incentivized users to lock tokens or assets—whether Bitcoin, Ethereum, or stablecoins—by offering yields. These tokens were required to be locked into these new protocols.

However, one of the core issues is that many of these so-called "returns" are actually inflation disguised as returns. If you and I start a project where we hold 50% of the token supply, sell 10% to the market, and keep 40% as rewards, then as users gradually acquire this 40% through "returns," we early holders will continuously sell tokens to new buyers while they wait for those returns.

Lex Sokolin: I have to interrupt because this has always struck me as incredible. High school economics 101 teaches the difference between nominal and real interest rates, and I think if people truly understood the difference between nominal and real returns, many crypto projects might not even exist.

David Namdar: I think that's one of the things that fascinates me about the crypto market. No matter what industry people came from before, once they enter the crypto space, they have to grow and evolve. For example, if someone comes from a hedge fund or traditional market background, they suddenly need to learn early-stage tech investing, understand the global regulatory environment, and master the technology in entirely new ways. If they are lawyers, they not only need to understand the law, but also the market, early and late-stage investments, and even have a deeper understanding of security and technology than ever before.

This kind of cross-disciplinary learning is positive, but at the same time, every cycle brings a lot of misunderstandings about economics. Many people can't distinguish between genuine technological innovation and hype or pure marketing.

Lex Sokolin: This raises the question: what has been the attitude of the US public markets towards crypto and fintech companies post-pandemic? After two years of lockdowns, everyone was online, speculation was rampant, everything was digital, and commerce had shifted entirely to Amazon rather than brick-and-mortar stores. People were ready for these changes; you even saw a retail army on GameStop's Reddit account, and there was a lot of capital waiting to be deployed in the market. But then all of that quickly vanished. What happened?

David Namdar: During this period, the frenzy surrounding GameStop and Reddit overlapped with the excitement in the crypto market. I remember the Coinbase IPO; the hype and momentum were almost identical to that of Robinhood's IPO.

David Namdar: It all came together in the end. I think the most significant thing about that period was that, outside of the crypto market, it was actually the first time that retail investors were truly trying to take the initiative in the capital markets and gain greater investment power. And a similar trend emerged in the crypto market as part of a longer-term, grander vision—eliminating intermediaries, taking control of personal finances, achieving financial sovereignty, and an idealized vision of the future of money and finance.

However, the reality is that they still face obstacles such as transaction costs, regulatory barriers, and market structure. Many even believe that this game is still "manipulated." If I remember correctly, Robinhood repeatedly suspended its purchases of some popular concept stocks and "meme stocks" due to pressure from its backers and institutions.

David Namdar: Although the incident caused a brief market crash, it also further strengthened people's confidence in the crypto market because there are no large institutions manipulating the rules of the game in the crypto world.

Digital Asset Treasury

Lex Sokolin: Next, let's talk about digital asset treasuries. First, let's define what they are and how they came about, and then we'll discuss the current market landscape.

David Namdar: To explain this concept, we need to go back a little. I usually start with Michael Saylor, but this time I want to go a bit further back. Actually, there were one or two companies that started this trend early on, and I still keep in touch with some of them, such as Charles Allen, who ran BTCS, a company that has now transformed and is considered a representative of the Ethereum Treasury.

David Namdar: He went public in 2014 or 2015, making him one of the earliest publicly traded companies to hold digital assets on its balance sheet. In contrast, other mining companies typically sell the mined Bitcoin or Ethereum immediately to cover fees and record the remainder as revenue.

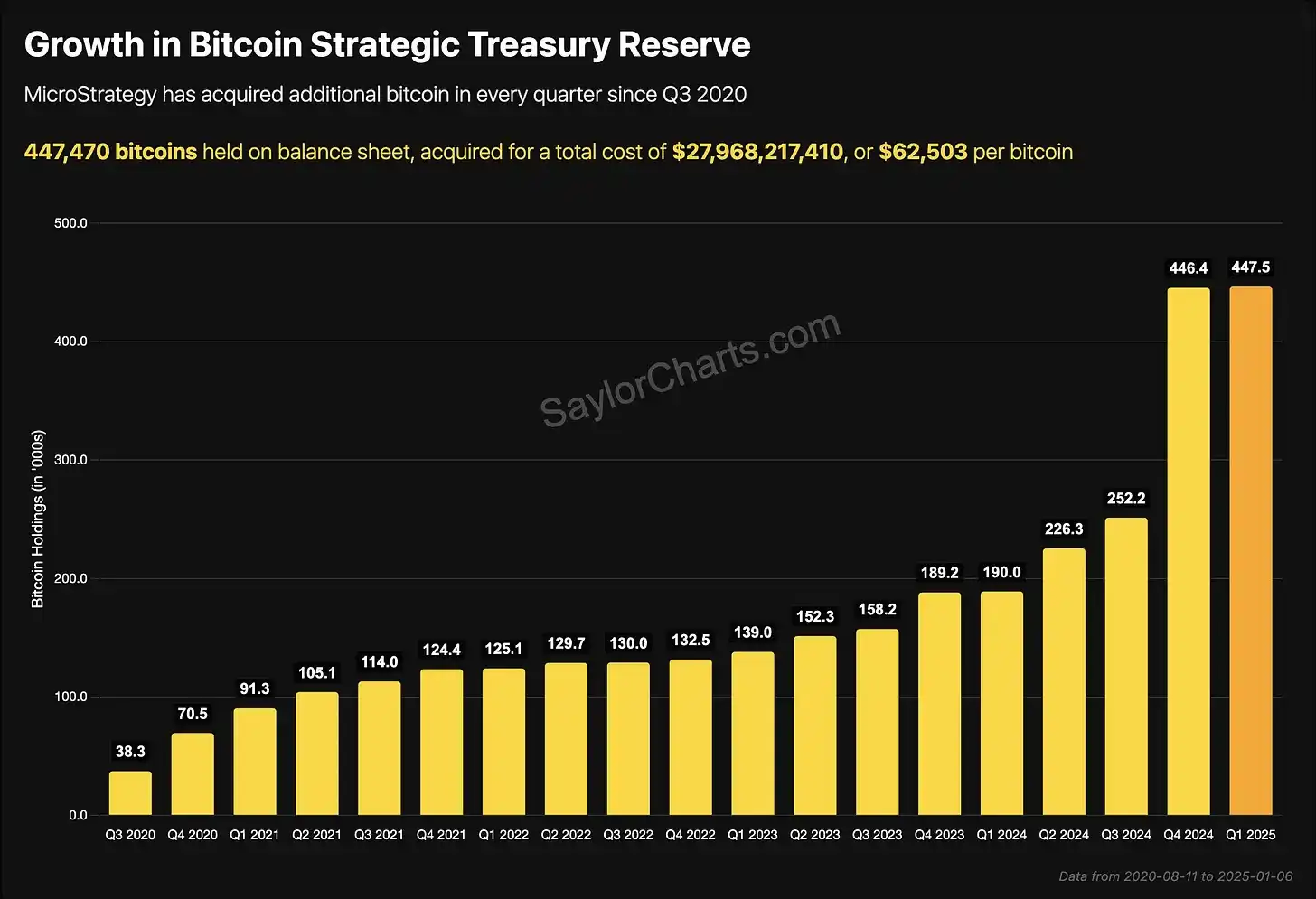

Let's go back five years to the story of Michael Saylor. He had spent most of his career running a traditional tech company focused on software, but the company was struggling to grow, despite having around $400 million in cash on hand. Later, he was convinced of the value and potential of Bitcoin, and there's an interesting story behind this: as far as I know, he sold the domain voice.com to Brendan Blumer—a key figure in Block.one and the EOS ICO. When Saylor saw that the deal was worth $30 million, he realized there must be much bigger opportunities in the crypto world.

David Namdar: His initial thought was, "If these people in the crypto world have this much money, there must be an opportunity here." This led him to rediscover Bitcoin's potential and ultimately commit fully, and in an incredible way. He converted all $400 million in cash on the company's books into Bitcoin, believing it to be stronger and more robust than fiat currency. He fiercely debated this with the board and overcame various regulatory hurdles. Ultimately, when he began buying Bitcoin, the company's stock price saw a premium, the market reacted positively, and investors were very excited.

He then used the stock price premium to continuously sell more shares, obtaining funds to purchase Bitcoin, thus creating a cycle of "selling stocks and buying Bitcoin." Going further, he issued convertible bonds and other financial products, with the sole purpose of accumulating more Bitcoin. This process effectively initiated the financialization of Bitcoin.

David Namdar: Over the past five years, he has successfully accumulated over $75 billion worth of Bitcoin, and his company's market capitalization now exceeds $100 billion. Due to his achievements and holding more than 3% of the global Bitcoin supply, this strategy has quickly become a trend and has been imitated.

He not only implemented the initiative himself but also actively promoted its dissemination, hosting "Bitcoin for Corporates" events to teach corporate finance executives, CFOs, and small business owners about the advantages of Bitcoin compared to fiat currency. He even visited large listed companies and private enterprises to popularize the concept of digital asset treasuries.

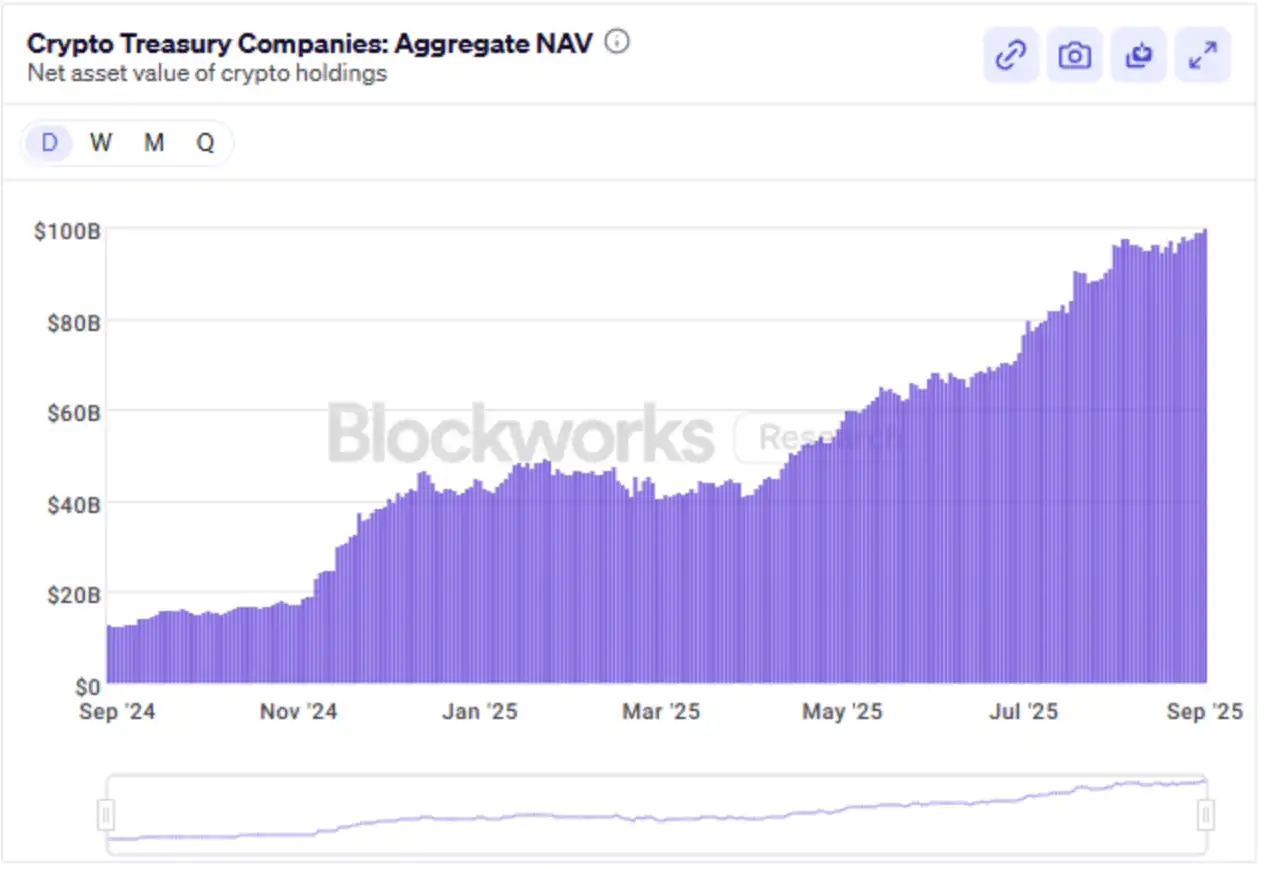

Over the past year or two, this trend has spread not only in the United States but also to multiple markets around the world. Currently, more than 100 digital asset treasury companies are focusing on accumulating Bitcoin, and more than a dozen other companies have begun to realize that holding other important crypto assets is also valuable.

David Namdar: He now holds over $75 billion worth of Bitcoin over the past five years, and his company's market capitalization has surpassed $100 billion. His strategy of controlling approximately 3% of the global Bitcoin supply quickly inspired imitation and became an industry trend. He not only implemented it himself but also actively promoted it, hosting "Bitcoin for Corporates" events to educate corporate finance executives, CFOs, and small business owners about the advantages of Bitcoin compared to fiat currency. This trend has now spread beyond the United States to multiple markets globally. Currently, over 100 digital asset treasury companies are focused on Bitcoin accumulation, and more than ten companies are beginning to invest in Ethereum, Solana, and even other core crypto assets such as BNB.

Lex Sokolin: Going back to Michael Saylor's operations, especially the early premium of market capitalization relative to net asset value, what financial instruments did he use to achieve such rapid growth?

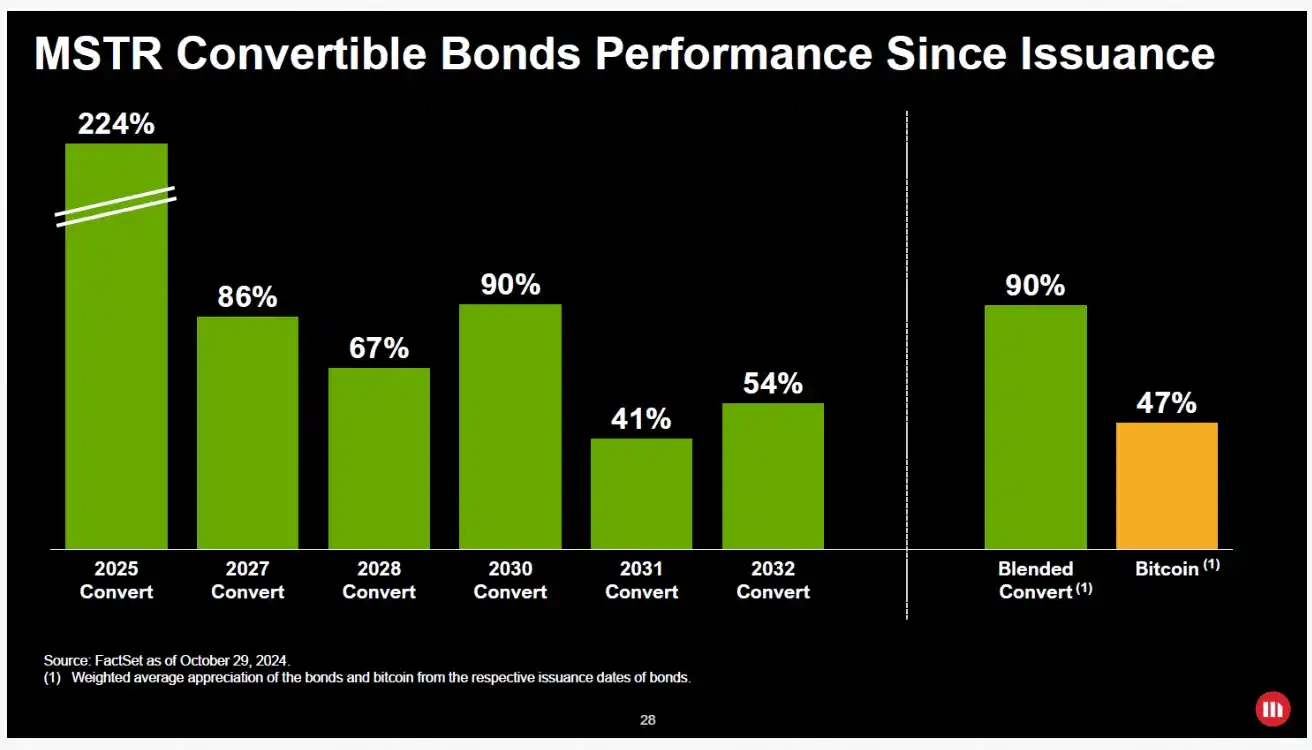

David Namdar: Absolutely. I'm not sure exactly when he started using convertible bonds early on, but it's certain that his business faced some vulnerability during 2021 and 2022. I recall him even borrowing on-chain through DeFi products because the market was focused on his Bitcoin liquidation price, and if it fell to $3,000 or $5,000, he might be forced to liquidate.

His strategy included using an ATM (At-the-Market) issuance mechanism to raise funds by selling shares at a premium, a premium that lasted far longer than market expectations and typically exceeded the book value of his Bitcoin holdings by 70% to 100%. Furthermore, he pioneered the "financialization" of Bitcoin, issuing multiple convertible bonds. As his balance sheet expanded, he even secured extremely favorable debt terms and issued preferred stock.

His logic is simple: Bitcoin's annual growth rate is between 20% and 30%, or even higher, making it one of the fastest-growing "horses" in the world. He believes that as long as one can borrow fiat currency at an interest rate of 0% or 5%, it's worth doing and holding as much Bitcoin as possible. This strategy has been extremely effective so far.

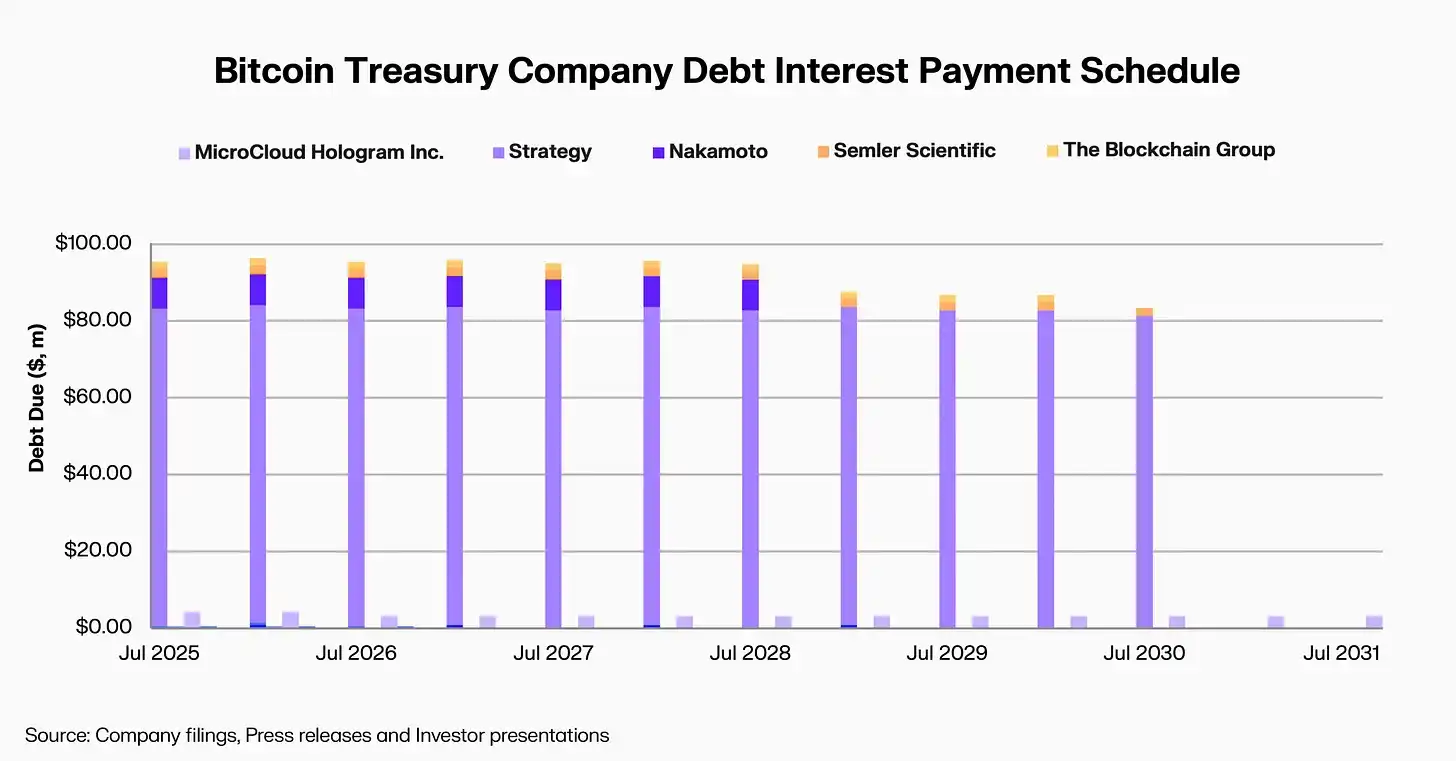

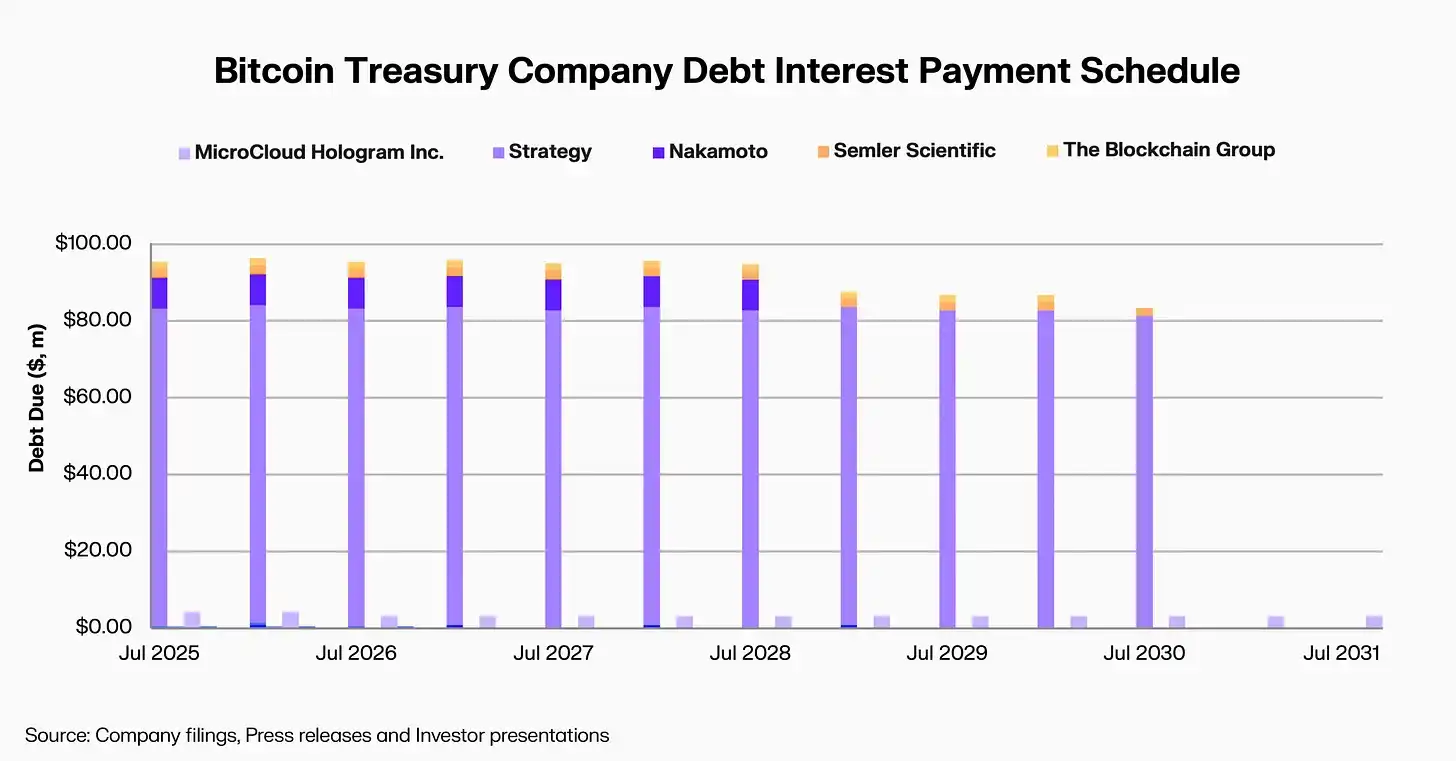

David Namdar: Looking at the current landscape of digital asset treasury companies, some have experimented with convertible bonds, but many are gradually moving away from this approach to avoid any structure that could put their balance sheets at risk. One reason is that today's convertible bond investors are offering much more stringent terms than Michael Saylor received back then.

These convertible bond investors don't care what the underlying asset is, whether it's Bitcoin, Ethereum, or other crypto assets; they only care about their claim to that asset. Furthermore, they are often motivated to hedge their risk exposure by short stocks.

Therefore, I believe that in the future we will see these treasury companies reduce their use of convertible bonds and instead explore more reasonable financing mechanisms to ensure that the interests of all investors are aligned and to avoid structural conflicts.

Lex Sokolin: Why do you think MicroStrategy's premium can last so long?

David Namdar: That's a good question. I think, first of all, he's been very successful in telling his story. The market believes he has the ability to continuously accumulate Bitcoin and increase the amount of Bitcoin per share, which is key for investors. I myself am an investor and I'm also following this area. I've intermittently invested in MicroStrategy and MetaPlanet over the past few years, and I've invested in some new companies in this cycle. My investment logic is to select companies whose management teams can consistently increase their holdings of Bitcoin, Ethereum, or BNB per share, and these teams are expected to have a long-term presence in the industry, rather than short-term arbitrage based on market frenzy.

Lex Sokolin: Could you talk about the changes in price dynamics over the past 6 to 12 months? I know we'll be talking about Binance and the debt issuance you led soon, but before that, I'd like you to add some information about what happened between May and October of this year.

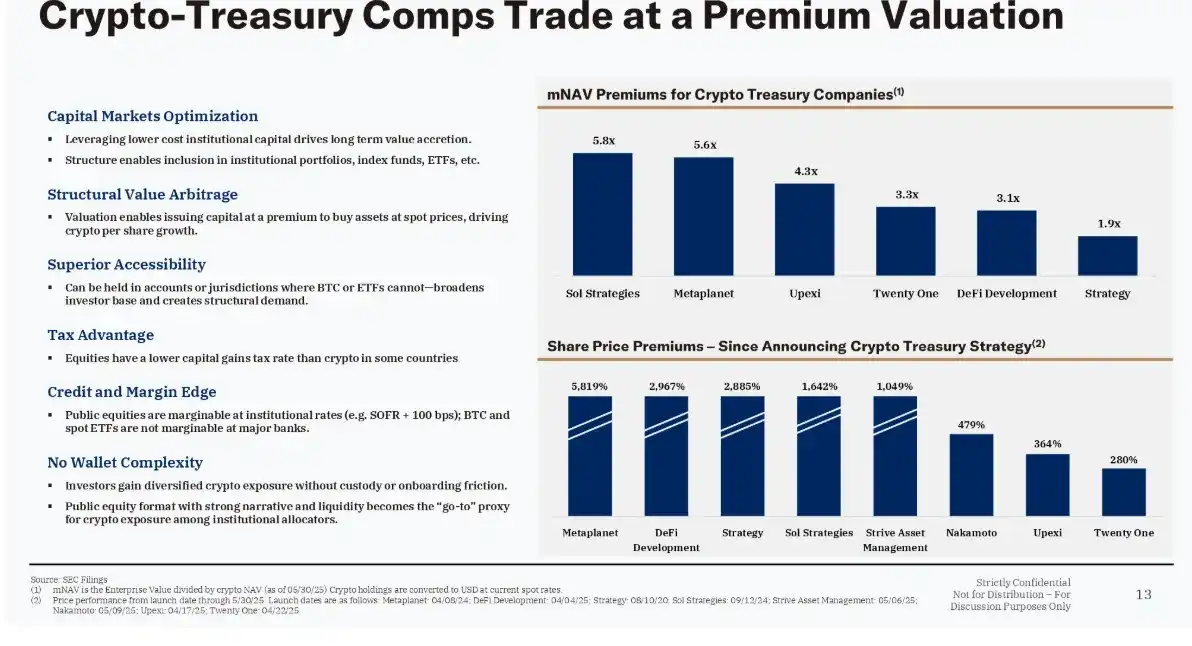

David Namdar: This year's debt financing boom primarily stemmed from two cases: MetaPlanet in Japan and Nakamoto in Puerto Rico, founded by David Bailey. MetaPlanet's performance has been the most outstanding, arguably the most successful Bitcoin treasury company globally, second only to MicroStrategy. They capitalized on a unique advantage of the Japanese market—holding Bitcoin through a publicly listed company is more tax-advantageous than direct private ownership. Based on this, MetaPlanet once commanded a premium similar to MicroStrategy, ranging from 50% to 100%.

David Namdar: At the time, they held approximately several hundred bitcoins on their balance sheet, worth about $700 million. Subsequently, the market realized that rapidly introducing Japanese capital into the crypto space through the public market was a shortcut, and Meta Planet's share price premium quickly expanded, reaching as high as 400% to 500%. The company took the opportunity to issue more shares, significantly increasing its bitcoin holdings per share, ultimately accumulating a total of billions of dollars worth of bitcoins.

In the United States, Nakamoto was founded by David Bailey, one of the earliest Bitcoin holders I know, earlier than Michael Saylor, and even earlier than almost everyone active in the industry today. He founded Bitcoin Magazine and BTC Inc., and was one of the major investors in Meta Planet.

David Namdar: He essentially followed MicroStrategy's approach, incubating several Bitcoin treasury companies globally. Then, he founded Nakamoto, which truly made the market aware of the opportunity. He was incredibly successful in raising awareness and fundraising—initially planning to raise $200 million, he ultimately raised over $700 million. This move directly sparked a wave of Bitcoin treasury companies.

We've seen Anthony Pompliano, Vivek Ramaswamy's Strive Asset Management, and other teams take different paths, some through mergers and acquisitions of existing companies, others through SPACs. There's also Jack Mallers' $121 million funding round in partnership with Cantor and Tether. A variety of strategies have emerged in the market.

At the time, the core logic was that you were investing in a "pipeline," or a company that was issued at close to its net asset value (NAV). If the market premium persisted, you would have the opportunity to obtain a certain or even considerable return in the short term, because the public market would give these treasury companies a premium, thereby driving the entire flywheel effect.

David Namdar: That was the initial logic, and what excited the market at the time. Subsequently, we saw two Ethereum treasury companies enter the market, the two largest being Sharp Link and Bitmain. Bitmain was an established player in the industry, while Sharp Link was originally a gambling company, later acquired by Joe Lubin, co-founder of ConsenSys and one of the founders of Ethereum.

They successfully conveyed a vision to the market: Ethereum is an asset with immense potential. Meanwhile, Wall Street capitalized on the momentum and enthusiasm surrounding stablecoins following Circle's successful IPO. Sharp Link seized this window of opportunity, leveraging market hype by selling shares at a premium, and in a short period, amassed approximately $15 billion to $20 billion in Ethereum through innovative methods, creating significant value for early PIPE investors and shareholders.

David Namdar: Over the past few months, I've felt the market is somewhat similar to the ICO boom of 2017 and 2018. I've formed a prediction: if $50 billion to $100 billion of capital flows in in the future, approximately 25% to 50% will concentrate in the top five to ten companies, such as MicroStrategy, MetaPlanet, 21 Pro, ProCap Nakamoto, and Link BMR. The next 25% will flow to twenty to thirty mid-sized companies, and the remaining 25% will be distributed among the long tail of 100 to 300 companies.

This distribution is very similar to that of the ICO era. Back then, there were some surprising cases among the long-tail projects, such as some projects that managed to raise $30 million or even $100 million. Some of these projects still exist today and have developed into meaningful businesses, but many others have eventually disappeared.

The dispersion of capital across these different tiers has led to investor confusion and has also ushered in a phase common in the crypto market: from euphoria and excitement to hesitation, anxiety, and even fatigue. I believe the market is currently showing signs of fatigue with the "treasury strategy," which is why many related companies are still trading at a premium to their net asset value (NAV).

Why choose the BNB ecosystem?

Lex Sokolin: Over the past few years, many different types of tokens and cryptocurrencies have adopted a similar "digital asset treasury" model. In many cases, these treasury companies are replacing the role originally played by foundations. Now, with regulators and the political environment becoming more favorable to cryptocurrencies, businesses can directly drive protocol development as commercial entities, without relying on non-commercial foundations, grants, or cultural frameworks incompatible with their actual goals. While this background information is extensive, I believe it is very important.

Next, please talk about Binance, BNB, and your current focus.

David Namdar: Absolutely. I think context is crucial. Only those who have truly entered the crypto space, or those who have personally experienced these exciting cycles, can understand where we are now and why we've come this far. You just mentioned the current regulatory environment, and I think that's the most important factor driving all of this. If the regulatory environment had been more mature earlier, we might have had a Bitcoin ETF much earlier, and even the Winklevoss brothers' ETF might have been approved. In that case, US investors might have already made $50 billion to $200 billion in profits on Bitcoin, and the US market would have seen more innovation, more companies, and a more vibrant ecosystem.

David Namdar: This trend has also enabled some new crypto companies to successfully enter the capital markets over the past year, including Circle, Gemini, and Bullish. I believe there will be more crypto companies going public in the future. At the same time, we will also see more reasonable regulations emerge, creating more opportunities for existing US crypto trading platforms, as well as some international trading platforms, to interact with US users. Recently, the CME or CFTC released relevant regulatory explorations, considering allowing US investors to access overseas crypto trading platforms, which could be one of the most significant news events in the next one to two quarters.

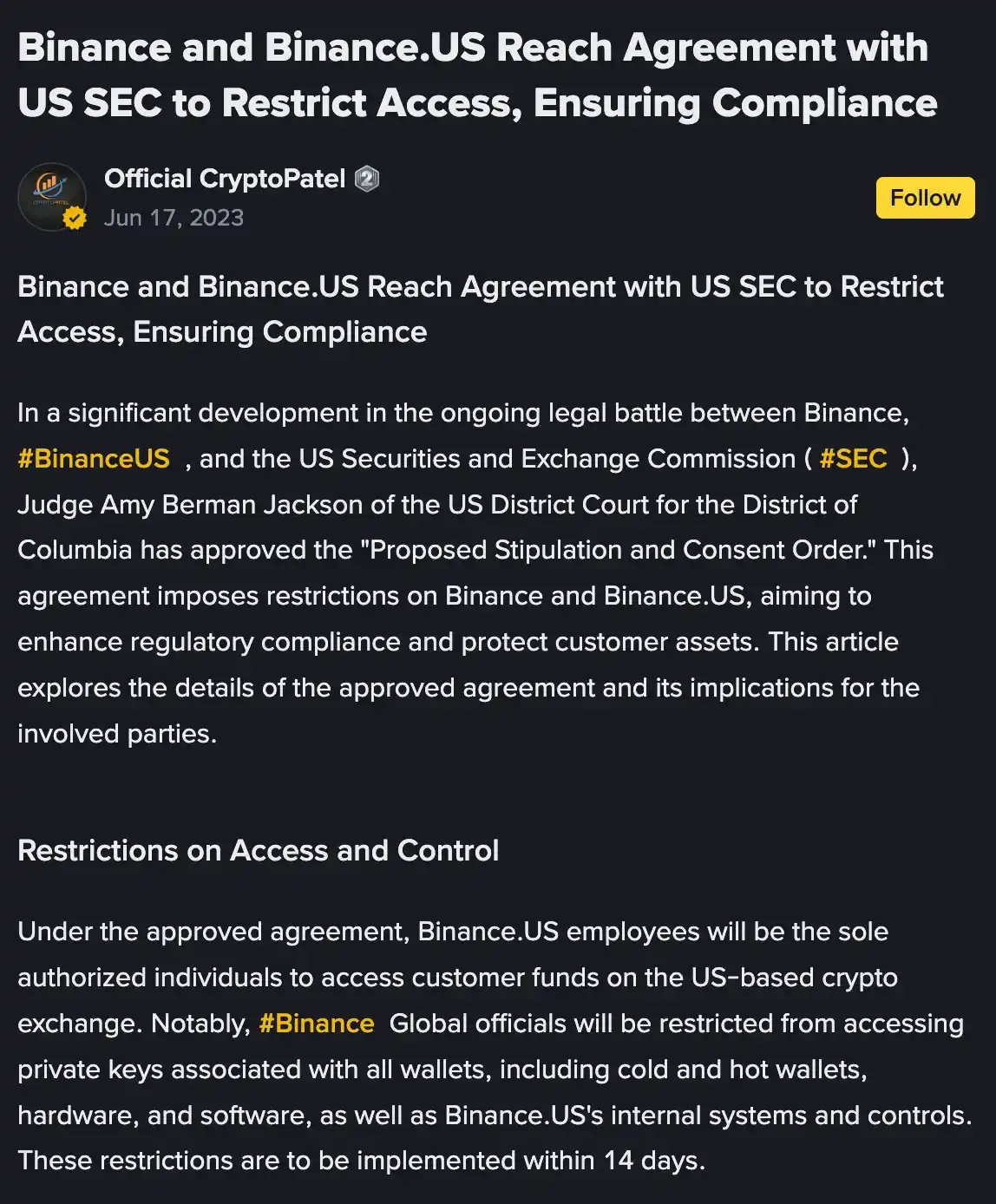

For me, regulatory issues have always been a major concern. After Galaxy, I had opportunities to serve as CEO of FTX US, Binance US, and some listed mining companies, but ultimately felt they weren't a good fit. I didn't want to put all my energy into one trading platform or company, and more importantly, the pressure from the regulatory environment could force me to leave the industry altogether. I know someone who was running a trading platform at the time, and he was eventually completely overwhelmed and even left the industry.

Over the past few years, I've been investing broadly across the sector, supporting early entrants looking to sell their businesses or go public via IPO or SPAC. The stories of Binance and BNB have been a constant companion throughout this process. After investing in these companies, some close friends told me, "You have more experience in crypto and capital markets than many people, and you're better at telling and selling the 'treasury story' than many management teams or even bankers."

David Namdar: They did want me to run a Bitcoin treasury company in any market around the world. But after careful consideration, I realized I couldn't tell the Bitcoin story with the same passion and conviction as Michael Saylor, David Bailey, or Simon of Metapan. Instead, I'm better at identifying trends in the global crypto market, revealing overlooked or underestimated opportunities, and helping people understand the truly global nature of the crypto industry.

Therefore, running a Bitcoin treasury company didn't seem like a good fit for me, and I even felt it was difficult to truly commit. But when I thought about running a treasury company focused on BNB, it felt perfectly appropriate. Ultimately, with the encouragement of several close partners, I decided to take on this challenge. I am very grateful because it has become an exciting story over the past few months. I believe that this will be a cause I am extremely passionate about and willing to fully dedicate myself to for years to come.

Lex Sokolin: Let's start with some background information: What is Binance? How large is it? How many users does it have? Could you give us a comparison, for example, with companies like Coinbase? Also, what is the BNB token?

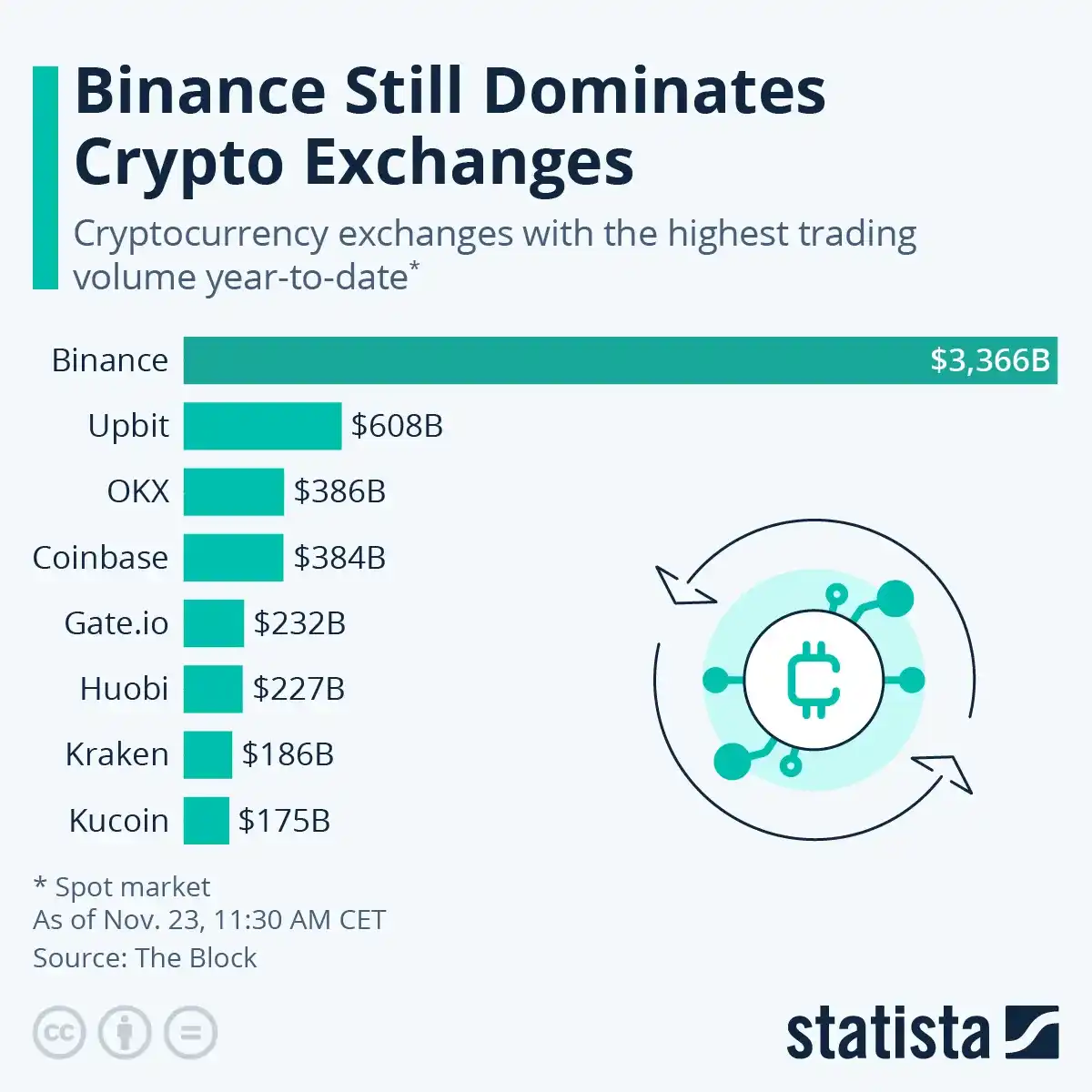

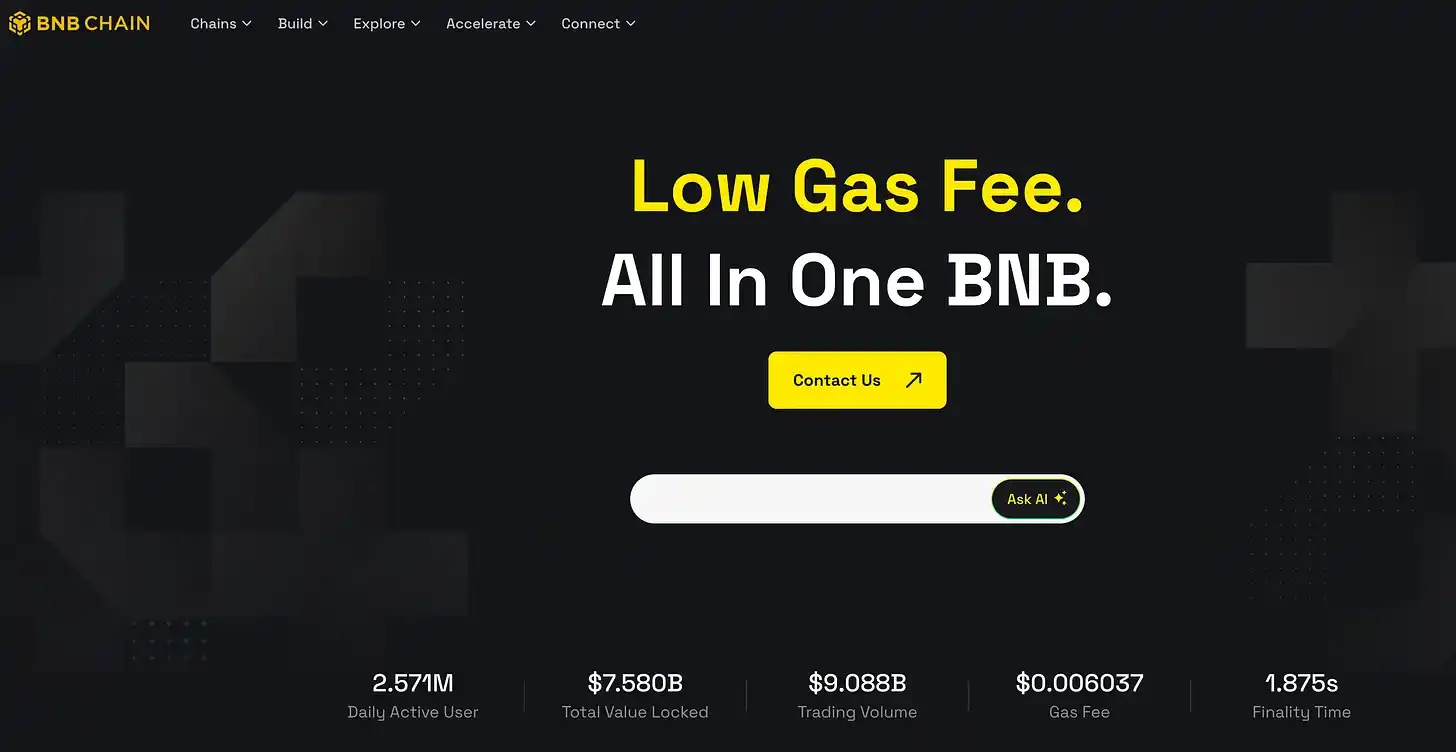

David Namdar: Binance is undoubtedly the world's largest cryptocurrency exchange. To give you a sense of scale, according to its official website, it has over 290 million users. In comparison, Coinbase has approximately 20 to 40 million users, Kraken has around 10 to 20 million, and Gemini falls within that range. In other words, Binance's size is likely 5 to 15 times that of Coinbase or other US exchanges.

David Namdar: Binance is not only the world's largest cryptocurrency exchange, but it also leads in trading volume across almost all trading pairs, accounting for nearly 40% of global crypto trading volume. To put it another way, if we look at other industries, such as social media, search, or hardware, the leading companies in these fields—Facebook, Google, and Apple—are all American companies, listed in the US, and have a large number of American users. However, in the crypto industry, Binance, the largest exchange, neither operates in the US nor has any American customers.

If Binance could enter the US market and attract American users, its scale would be much larger. However, the current reality is that US investors cannot invest in the company's equity, and US users cannot directly use its services. I can't think of any other industry where the world's largest company is completely outside the US system.

Lex Sokolin: So, how does the BNB token work? How does it accumulate value? And how does DAT (Digital Asset Treasury) derive value from the token?

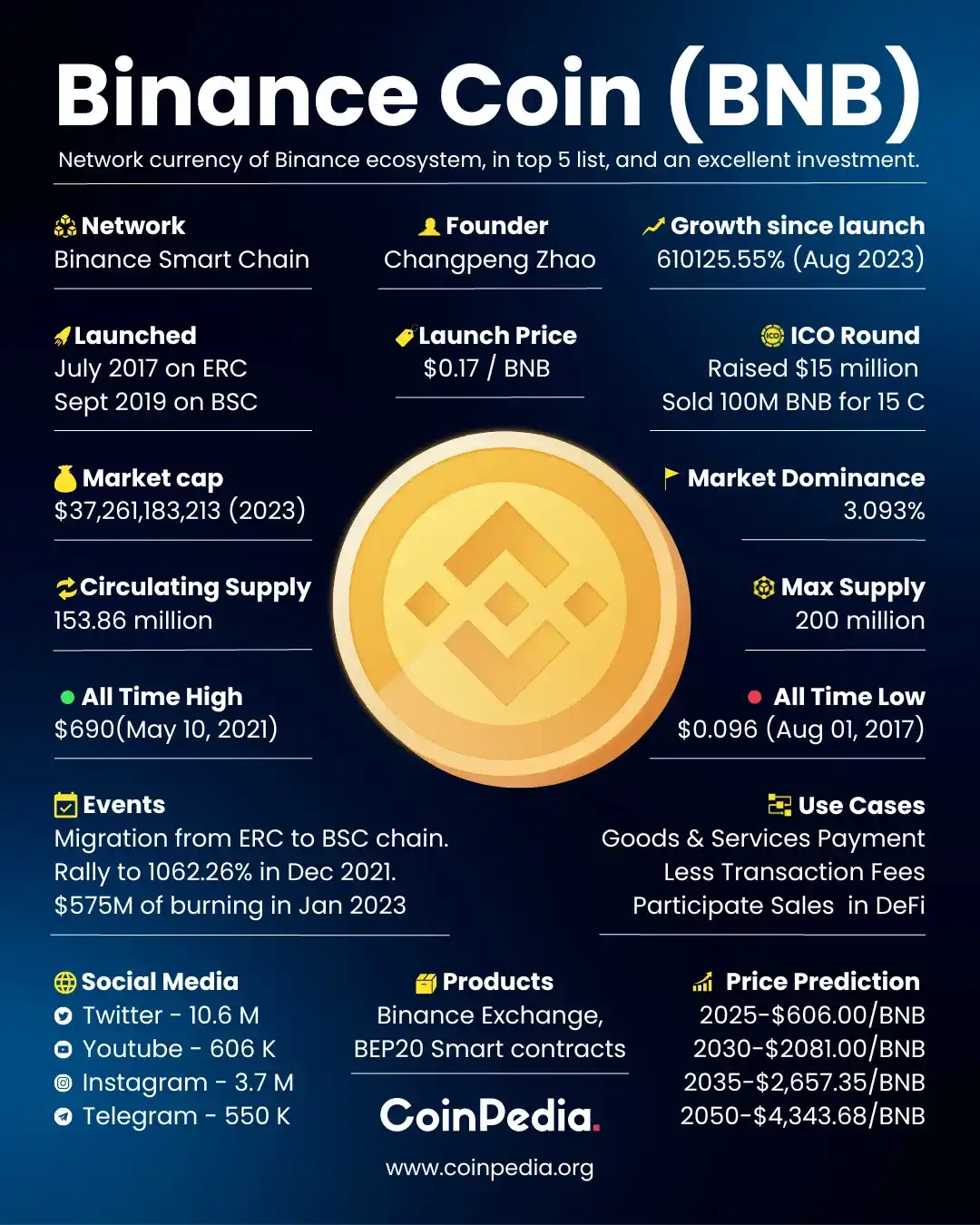

David Namdar: When Binance rose to prominence in 2017 and 2018, it pioneered the launch of a trading platform token. Unlike Bitcoin or Ethereum, BNB's initial purpose was to offer users discounts on transaction fees. It has been pointed out that this is quite accurate: trading remains the most successful and core use case in the crypto world to date. For some, trading means speculation; for others, it's an exchange of value or investment growth. After all, this asset class has grown from hundreds of billions of dollars to approximately four trillion dollars today, and the importance of trading is undeniable.

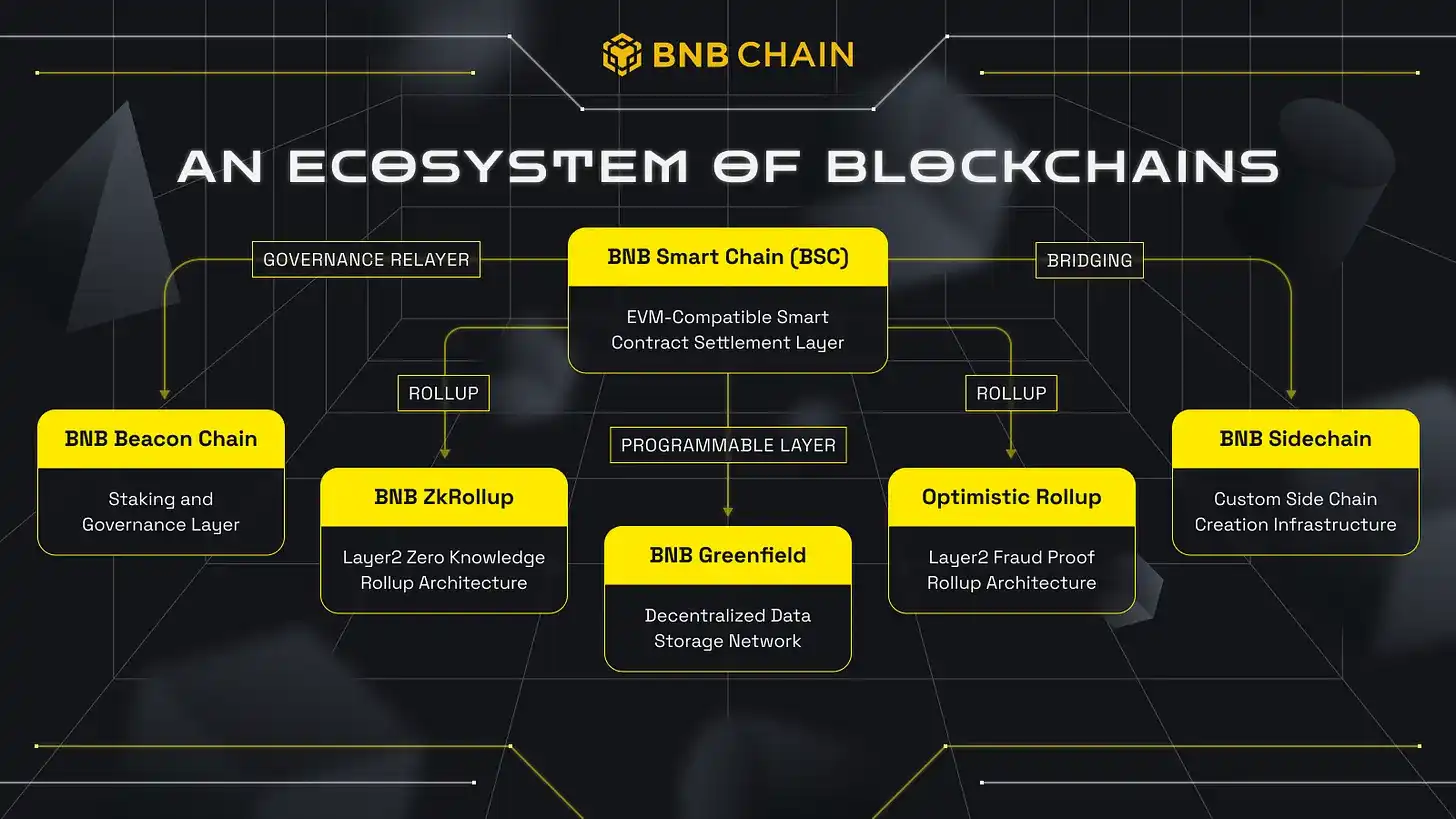

Initially used for transaction fee discounts, BNB was upgraded and migrated over the past five years to become BNB Chain, forming a vibrant ecosystem that remains closely integrated with Binance. It is estimated that approximately 80% to 90% of Binance's 290 million users use BNB to pay transaction fees. From this perspective, BNB is likely one of the most widely used cryptocurrencies globally, and while much activity occurs off-chain, this remains a long-term positive for BNB. Furthermore, BNB allows users to participate in other ecosystem activities such as airdrops, promotions, and rewards.

David Namdar: The value of the BNB token comes not only from transaction fee discounts but also from its unique deflationary mechanism, which distinguishes it from Bitcoin and Ethereum. Ethereum generates a "Gas" fee for each transaction, which ultimately flows to miners; in the BNB ecosystem, each transaction triggers a small burning mechanism, reducing the total token supply. Furthermore, all transaction fees are used for quarterly burning, further shrinking the supply.

For example, the average burn amount over the past four quarters has exceeded $1 billion per quarter, and I expect this quarter to set a new record, potentially exceeding $1.5 billion, or even reaching $2 billion in BNB burn value. This continuous burning not only creates scarcity but also reinforces the long-term value logic of the token.

David Namdar: While these tokens aren't stocks, they share a similar mechanism in some ways. For example, if you look at stock buybacks, like what Warren Buffett does at Berkshire Hathaway, or other large companies, when a company is profitable, it can choose to pay dividends, reinvest, or buy back shares to reduce the supply. BNB's mechanism is similar; it shrinks the supply through quarterly token burns, reducing the total token supply by about 3% to 6% annually.

Lex Sokolin: If a debt transaction is priced below net asset value, does that matter? If so, what tools would you use to address it?

David Namdar: Let me take a step back and explain why we started this project and my perspective on it. My view on DAT (Digital Asset Treasury) and the opportunities it presents is that it's a medium- to long-term investment. I've been investing in these companies and believe in their potential. For example, MetaPlanet was one of the best-performing and most liquid stocks in Japan last year, but it took a year or two for the groundwork to fall into place. And MicroStrategy took five years for the market to truly realize the massive cumulative effect of its Bitcoin holdings.

Therefore, when I consider this model, my logic is that BNB is an extremely valuable asset, and I want to hold more of it while helping more people gain exposure to it. Especially in the US market, the availability of BNB is very limited, and this gap is not only a current obstacle but could also become a catalyst for future value growth.

David Namdar: US investors not only find it difficult to directly participate in the BNB ecosystem, but they also face difficulties even in purchasing the underlying assets. Therefore, our goal is to create a compliant investment vehicle—a Nasdaq-listed company—that allows investors to gain exposure to BNB through this channel.

Looking back on my early experience promoting Bitcoin ETFs, I still feel regret: due to the SEC and other regulatory agencies' refusal to approve them, American investors missed the opportunity to invest in Bitcoin when it was only between $100 and $300 through an ETF. Today, BNB is similarly difficult to access in the US market, meaning American investors are once again excluded from a thriving ecosystem.

I hope that through this project, more people will recognize this opportunity and be provided with medium- to long-term investment opportunities.

David Namdar: From a market dynamics perspective, the crypto industry consistently exhibits cyclical fluctuations: there are periods of euphoria, as well as periods of panic and pessimism. Just last week, we experienced one of the largest sell-offs in crypto history, possibly even the biggest ever. But surprisingly, the market rebounded quickly and strongly, confidence recovered, and BNB even broke through to new highs after the plunge, demonstrating remarkable resilience.

This also reminds us that volatility has always been one of the core characteristics of crypto assets. When an asset is in a phase of rapid growth, volatility can actually be a positive sign. The key is to take a long-term perspective and consider future trends. If anyone believes this is the end for crypto assets, or that they won't become an important part of society and the global financial system, they are clearly ignoring the larger trend.

David Namdar: If you believe that crypto assets will become a larger asset class in the future, then short-term premiums or discounts are not the most critical issue. What really matters is that treasury companies must focus on increasing the net value per share of crypto assets—whether it's Bitcoin, BNB, or Ethereum—while ensuring that these assets are not put at risk.

This is why I am very cautious and unwilling to use convertible bonds or any financing methods that could potentially damage the balance sheet. Because in ecosystems like Ethereum, Solana, and BNB, there are opportunities for staking, yielding, and other income. Even if the share price is below net asset value at some point, these yields and share buybacks at a discount can still generate value, increasing the value of each BNB share and ultimately benefiting all investors.

At the Bitcoin conference in Las Vegas this April or May, what impressed me most was when Michael Saylor was asked what he would do if the premium disappeared and the stock price fell below net asset value. His answer was very calm: "Suppose we hold $50 billion worth of Bitcoin, and someone is willing to sell the stock at a 20%, 30%, or even 50% discount, I would issue preferred stock to buy back those shares. This way, other shareholders would profit from my discounted buyback."

The biggest lesson I learned is that the key to successfully operating a financial company is to acquire capital regardless of market conditions and to continuously increase value in the medium to long term, so that this "value-added cycle" can work.

Lex Sokolin: That's fantastic. David, thank you so much for bringing such a wide range of discussion; I'm very excited about what you're doing. Where should our audience go if they want to know more about you and your company?

David Namdar: I'll try to share everything on my Twitter account @Namdar, the company account @BNB Network Co, and our website BNC network. Yes, these are good starting points.

Lex Sokolin: That's great, I'm glad you could come.

David Namdar: I'm very grateful, it's really great.

[ Original Link ]

Click to learn about BlockBeats' job openings.

Welcome to the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia