This article is machine translated

Show original

The Federal Reserve has officially entered the Warsh era. I've been following Powell since 2018, scrolling through my WeChat Moments – almost eight years now, and it's quite an experience. From a personal perspective, Powell isn't an artist of long-term prosperity like Greenspan, nor a crisis innovator like Bernanke; rather, he's a typical "data-driven" executor. Faced with multiple shocks from the pandemic, supply chains, geopolitics (Russia-Ukraine to the Middle East), fiscal expansion, and high inflation, he stabilized employment and the financial system with a pragmatic and flexible approach, but also paid the price of inflation due to initial "temporary" misjudgments. Let's also discuss the gains and losses of Powell's two terms.

Main gains: Decisive crisis response, strong employment resilience, and safeguarding independence deserve recognition.

1. The 2020 pandemic response was textbook-level zero interest rates + unlimited QE, with the balance sheet expanding from $4 trillion to $9 trillion. Combined with fiscal policy, this directly suppressed the recession to within two months, and employment quickly fell from the peak of the pandemic to a low of 3.5-4%. Throughout his term, the average unemployment rate was low, and a strong labor market became the biggest fundamental factor for the US economy. 1. The Powell team's swift response played a significant role in preventing a financial collapse and a double-dip recession.

2. The soft landing was relatively successful, with timely tightening corrections. Aggressive rate hikes in 2022-2023 suppressed inflation, while cautious adjustments in 2024-2025, driven by data, prevented a hard landing. The dot plot and press conferences repeatedly demonstrated "data dependence": strong employment led to patience, while recurring inflation slowed the pace of rate cuts. This had a stabilizing effect on liquidity management and market expectations, especially against the backdrop of fiscal bond issuance and reverse repos, signaling a slowdown in balance sheet reduction or adjustment, which actually benefited the marginal liquidity of risk assets.

3. Defending independence is the greatest legacy. Faced with political pressure (insults and investigations during the Trump era), Powell persisted to the end, even stating that he would remain a governor/interim chairman until the investigation was completed. This was crucial in an era of partisan polarization, preventing the Fed from becoming a complete fiscal/administrative appendage. As mentioned in previous posts, this has positive implications for market confidence and the external environment of the US-China financial game—an independent central bank makes capital flows more predictable.

4. A straightforward communication style and good internal consensus are maintained. While not holding a PhD in economics, the ability to explain complex policies clearly in plain language is crucial for managing market expectations.

Major Mistakes: The most obvious misjudgment was of inflation; policy path volatility was high; and the framework was biased towards employment.

1. The biggest mistake was the assessment of "temporary" inflation in 2021, underestimating supply shocks and fiscal spillovers, leading to runaway inflation in 2022 to a 40-year high, requiring aggressive correction later. The transmission of inflation, wages, and energy costs repeatedly occurred. In multiple posts on CPI and non-farm payrolls, I repeatedly emphasized that the "deviation between data and expectations" is far more important than absolute values. Powell's early framework (average inflation target) was too loose, sacrificing some price discipline. Average inflation during his term exceeded the target, and household purchasing power and asset pricing paid the price at times.

2. Path dependence and side effects: Early gradual interest rate hikes were followed by a rapid shift; the 2022 banking pressures (SVB, etc.) exposed regulatory shortcomings; later interest rate cuts were intertwined with politics/elections, with the dot plot repeatedly raising interest rate expectations and reducing the number of rate cuts, causing market volatility. The dual impact of energy and tariffs, coupled with the decision to hold rates steady or discuss potential rate hikes, indicates a lag in judgment. AI's observation that productivity growth is slow but pushes up the neutral interest rate aligns with my tracking of capital expenditure and the neutral interest rate.

3. Insufficient foresight in responding to fiscal-monetary interaction. In the era of high deficits, the pricing power of a single interest rate signal is weakened, leading to increased intervention and pronouncements from the Treasury Secretary and others. During Powell's tenure, fiscal policy sought low interest rates, but inflation constraints made it difficult to fully satisfy this demand. Liquidity repeatedly "drained" and "released" between TGA, balance sheet reduction, and bond issuance, significantly amplifying volatility in risky assets.

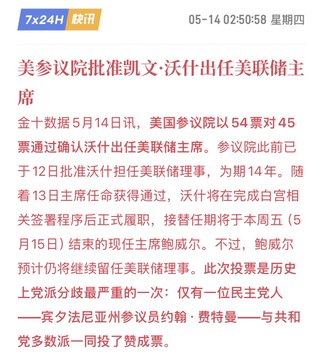

The next few years will depend on Warsh's performance. 🤔

twitter.com/qinbafrank/status/...

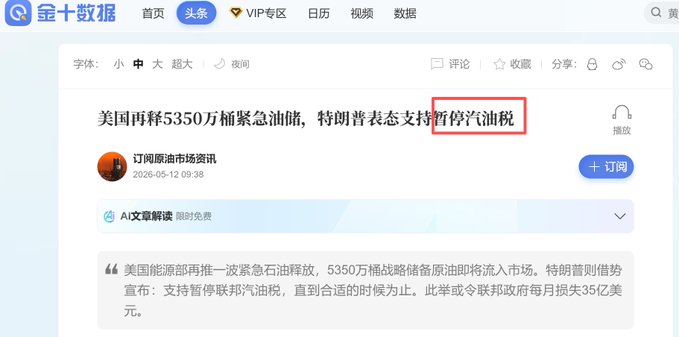

The government side is also trying to figure out something for oil prices.

Anyway, raising interest rates is impossible, and lowering them will take time too, right?

TVBee

@blockTVBee

05-14

The U.S. is considering suspending the gasoline tax; if passed, it would be good news.

A U.S. senator has proposed suspending the gasoline tax, and Trump has expressed support.

┈➤ How big would the impact of suspending the gasoline tax be on oil prices?

The U.S. gasoline tax x.com/blockTVBee/sta…

I also wrote about Powell, but my summary of Powell's contributions wasn't as comprehensive as Brother Wu's. However, I did analyze the reasons why he raised interest rates late.

TVBee

@blockTVBee

05-14

Powell has no problem, Trump has no problem either, but

Powell + Trump = inflation staying stubbornly high

Have you ever seen negative times negative equals positive, positive times positive equals negative?

┈➤Powell's Achievements

╰✦Trading time for space, achieving a x.com/blockTVBee/sta…

Sector:

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content