A discussion on risk, time and the future of money

I hope today's topic didn't surprise you. Because the reality severely slapped the topic in the face:

Gold, today (March 16), briefly broke through $3,000 per ounce, setting a new all-time high.

After falling from a high of 102,000, Bitcoin fell all the way below 77,000 and is now hovering around 84,000.

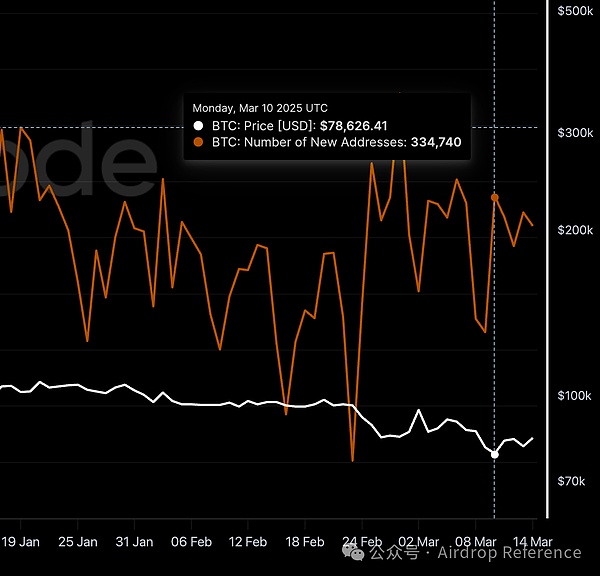

With such a sharp contrast, it is clear at a glance that gold is a better safe-haven asset than Bitcoin. So let me ask you, are you willing to sell your Bitcoin to buy gold? Anyway, I am not willing to do so, and I think you are certainly not willing to do so either. Moreover, not only are those who hold Bitcoins unwilling to sell, but there are also more and more new people joining in continuously, as shown in the figure below .

From the above picture, you can see that even when Bitcoin was at a historical low of 78,000, there were still 330,000 new Bitcoin addresses on that day. Obviously, there must be some unknown secrets behind the contradiction. Your decision not to sell Bitcoin and buy gold was correct. Today I will tell you the real reason behind it. The answer is in the title, remove the question mark:

Bitcoin, the ultimate safe-haven for long-termists.

Of course, it is not enough to just tell you the answer. I should also tell you the reason. At the same time, as a popular science column, I should also achieve unity of knowledge and action. So in the end, I will also give the path and method to practice this concept. If you believe in long-termism and are not the kind of person who wants to get rich by leveraging transactions, then please continue reading.

First of all, we need to understand what safe-haven assets are?

1. What are safe-haven assets?

Safe haven assets, as the name suggests, are assets that can maintain or even increase their value when markets are turbulent, the economy faces uncertainty, or other events occur that may cause traditional investments (such as stocks, bonds, etc.) to fall in value. Such assets are often viewed by investors as a "safe haven" to protect their wealth from loss during risky times.

Traditional safe-haven assets usually have the following core characteristics:

Low volatility or negative correlation: An ideal safe-haven asset should be relatively stable when the market fluctuates violently, and even negatively correlated with those high-risk assets (such as stocks). This means that when the stock market falls, the price of safe-haven assets may rise, thus playing a role in hedging risks.

Value storage ability: Safe-haven assets need to have the ability to maintain value in the long term and be able to resist the erosion of wealth by factors such as inflation. When people hold such assets, they value their ability to maintain purchasing power rather than pursuing short-term high returns.

Strong liquidity: Being able to buy or sell quickly and at a reasonable price when needed is also crucial for safe-haven assets. This ensures that investors can flexibly operate when they need to adjust their asset allocation.

Historical verification: Assets that have demonstrated safe-haven properties during multiple market crises or economic downturns in history are often more easily accepted and trusted by investors.

The three pillars of traditional safe-haven assets:

Gold : As a hard currency for thousands of years, gold's safe-haven myth stems from its 70-fold increase after the collapse of the Bretton Woods system in 1971. Its physical scarcity (the total amount of gold mined worldwide is about 205,000 tons) and anti-inflation properties (annualized return of about 7.3% in the past 50 years) make it a classic choice in times of crisis.

Government bonds : Taking U.S. Treasury bonds as an example, their "risk-free" label is based on national credit, but the scale of U.S. Treasury bonds exceeded 35 trillion U.S. dollars in 2024, and the actual yield has been negative for 18 consecutive months, revealing the inflation trap behind the "safe assets."

Safe-haven currencies : The US dollar, as the global settlement currency, accounted for 59% of foreign exchange reserves during the 2020 epidemic crisis; the Japanese yen relies on the low interest rate environment (Japan -0.1%) and the Swiss franc relies on the bank secrecy system to maintain its safe-haven status.

However, gold has long been considered a classic safe-haven asset. In many historical periods, when stock markets fell or geopolitical risks heated up, investors would flock to gold, causing its price to rise. Gold itself does not generate interest or dividends, but its scarcity and historical recognition as a store of value make it an important means of preserving value in uncertain times.

However, with the continuous development and innovation of financial markets and the diversification of investors' risk preferences, the definition of "safe-haven assets" is also evolving. Some emerging assets are beginning to show their safe-haven potential in specific environments, although they may not fully meet all the characteristics of traditional safe-haven assets. This is why we will discuss the relationship between Bitcoin and safe-haven today.

The most critical sentence in the above paragraph is "investor risk preference". Because of the existence of "investor risk preference", everyone's perception and feeling of risk are different. For example, for me, I don't expect to get rich through leveraged trading, so the ups and downs of Bitcoin's price have never been a risk or an opportunity for me.

So, what is risk to you?

2. Relativity of Risk

Now let’s look at the broader arena and see how risk looks different across geography and time.

Imagine that you live in different countries and feel different pressures from risks. For example, during the economic turmoil in Zimbabwe, hyperinflation made the currency almost worthless. For local residents, holding the local currency is the biggest risk, and they will try their best to convert their assets into more stable foreign currencies or physical objects. In a country with a stable economy, such as Switzerland, people may pay more attention to the long-term preservation of assets rather than the short-term risk of currency depreciation.

This is precisely the “spatial” relativity of risk—the same asset carries different risks in different economies.

The passage of time will also profoundly affect our perception of risk. Assets that were once considered high-risk may gradually be accepted by the market and regarded as mainstream over time; and assets that were once considered safe may also expose new risks due to changes in the times.

Looking at the picture above, you might think that such a large pullback must be caused by Bitcoin or other cryptocurrencies, but it is not. It is gold.

Because the safe-haven property of gold is not static. In different historical periods, the price fluctuation and safe-haven effect of gold will also be affected by various factors such as economy and politics. For example, in some economic recessions, gold has shown good safe-haven function, but in other periods, its performance may not be satisfactory.

From the panoramic picture above, you can clearly see that gold experienced significant corrections in the 1970s, 1980s and 2010s.

So, if we reposition the coordinates of time and space, what should we do as long-termists today?

First of all, it should be clear that a long-termist will not regard making money as the goal of life. We all try to do something more meaningful. In addition to work, I choose blockchain popularization, and you may choose something else. However, we all have one thing in common, that is, we don’t want to worry too much about making money. We hope to have a once-and-for-all way to manage our investments. We don’t have too high a profit demand, and we are not willing to take unnecessary risks.

However, as long as we live on Earth, there is a risk that we cannot avoid.

3. Risks of Fiat Currency

Fiat money, as the name implies, is a currency that is given legal status by government decree and is forced to be used as a circulating currency. The paper money we use in daily life, such as the US dollar, euro, yen, etc., are all fiat money. Unlike the currencies that have existed in history and are linked to a certain physical object (such as gold or silver), the value of modern fiat money is entirely based on people's trust in its issuing institution (usually the central bank) and the economic strength of the country.

3.1 Depreciation

The fatal flaw of fiat currency is its unlimited supply mechanism . In order to cope with economic downturns, stimulate economic growth or repay debts, governments and central banks often take measures to increase the money supply. Although moderate inflation may have a certain positive effect on the economy in the short term, in the long run, continued inflation will lead to a continuous decline in the purchasing power of currency.

Take the US dollar as an example. After it was decoupled from gold in 1971, its purchasing power has declined by 98%. In 2024, the Federal Reserve implemented quantitative easing to deal with the US debt crisis, causing the M2 money supply to surge by 23%, and the actual inflation rate to soar to 8.5%, far exceeding the policy target of 2%. This "printing tax" is creating a "time black hole" of wealth around the world - the actual yield on cash assets has been negative for 18 consecutive months, equivalent to an implicit loss of 6.3% purchasing power each year.

Even more serious is the negative feedback loop between sovereign debt and fiat currency credit: the scale of global sovereign debt has reached 356% of GDP, and the US debt has exceeded 35 trillion US dollars, and its "risk-free" label is collapsing. The proportion of Japanese central bank holdings of government bonds has exceeded 52%, causing the yen to plummet against the US dollar by 15%. This "debt monetization" mechanism is pushing the fiat currency system to the edge of the cliff.

In addition to depreciation, there is a more important personal sovereign risk: the bank can block or restrict your account at any time.

3.2 Blocking

Imagine that you have worked hard to accumulate a fortune and deposit it in a bank account. This money belongs to you in the legal sense and you can use it freely. However, in real life, your control over this money is not absolute. As an intermediary institution, the bank may restrict or even freeze your account in certain circumstances. This may be due to suspected legal disputes, cooperation with regulatory investigations, or even simply due to operational errors within the bank.

This indirectness of control over funds is a potential risk of holding fiat currency. Although your wealth exists in digital form, the ultimate control is in the hands of the state and financial institutions.

Cyprus Capital Controls in 2013: Cyprus imposed strict capital controls in 2013 to prevent the collapse of the banking system. Initially, the daily withdrawal limit for banks was set at 300 euros . Even more shocking, for bank deposits of more than 100,000 euros , depositors faced a loss of up to 60% of their assets, part of which was directly converted into bank shares. These strict capital controls lasted for about two years and severely restricted the control of ordinary people over their own wealth.

Argentina’s foreign exchange controls, 2011-2015: In response to economic difficulties and to prevent capital flight, the Argentine government implemented complex foreign exchange controls between 2011 and 2015, severely restricting individuals and businesses from purchasing U.S. dollars. This led to the rise of an illegal “black market” for U.S. dollars, and many individuals and businesses had difficulty obtaining the dollars they needed to conduct international trade or save. It is estimated that grain exporters at the time hoarded billions of dollars of agricultural products, waiting to be sold at a more favorable exchange rate after the controls were lifted, reflecting the significant impact of foreign exchange controls on economic activity.

Icelandic capital controls 2008-2017: After the 2008 financial crisis, Iceland implemented capital controls for nearly a decade in order to prevent large-scale capital flight. These measures severely restricted foreign exchange outflows, including restrictions on cross-border payments and capital flows. The main reason for the implementation of capital controls was the fear of large outflows of funds held domestically by bankrupt Icelandic banks, which could lead to a significant depreciation of the Icelandic currency, the krona. These controls were not gradually lifted until 2017.

Bank withdrawal restrictions in Venezuela in 2017: As the Venezuelan economic crisis continued to worsen, the government imposed strict restrictions on bank withdrawals. In 2017, the daily withdrawal limit for ATMs was only 10,000 bolivars , which was worth less than $1 at the time . To make matters worse, ATMs were often out of cash, and people had to queue for hours to withdraw a maximum of 20,000 bolivars at bank counters , which was far from meeting the needs of daily life.

All of the above real cases and data clearly show that under the fiat currency system, during certain economic or political crises, the government may take strong measures to restrict or even freeze individual bank accounts to maintain financial stability or other policy goals. This is undoubtedly a risk that long-termists who pursue long-term wealth security and personal financial autonomy need to seriously consider.

In more extreme cases, if you encounter a financial crisis or a bank collapses, your deposits may be at risk of loss. Although there is now protection from the deposit insurance system, there is still a certain upper limit.

For those who seek greater financial autonomy and personal sovereignty, this is a question that needs to be seriously considered. Now, it should be possible to answer the question of why "Bitcoin" is a better safe-haven asset for "long-termists".

4. Why should long-termists choose Bitcoin?

In fact, the first thing we should exclude is legal currency. Don’t choose even the US dollar, Japanese yen, or euro.

4.1 Fiat Currency Vs. Bitcoin

We have seen that the purchasing power of the U.S. dollar, for example, has shrunk significantly since it was decoupled from gold. One of the most striking features of Bitcoin is that its total supply is constant . The total supply limit of 21 million is written into its underlying code and cannot be changed.

Bitcoin's supply mechanism is the first monetary contract in human history sealed by mathematics: the output is halved every four years, and the total amount is constant at 21 million in 2140. This programmed deflation model is in sharp contrast to the unlimited over-issuance of legal tender. Take 2024 as an example:

USD : The Fed expanded its balance sheet by 23% to cope with the US debt crisis, the M2 money supply exceeded 22 trillion USD, and the actual inflation rate soared to 8.5%;

Bitcoin : After the fourth halving, the annual inflation rate dropped to 0.9%, far lower than gold's 1.7% .

We have also discussed the risk of fiat currency accounts being blocked. The decentralized nature of Bitcoin can effectively avoid this risk. The Bitcoin network is not controlled by any single central agency, and transaction records are openly and transparently stored on the blockchain. No one can tamper with or freeze a user's Bitcoin assets at will unless the user discloses the private key.

4.2 National Debt Vs. Bitcoin

Treasury bonds, especially sovereign debt like U.S. Treasuries, have long been considered "risk-free assets" in the financial market. This concept is based on the credit of the country, and investors believe that the government has the ability to repay the bonds it issues. In times of market turmoil, funds tend to flock to Treasury bonds in search of safety.

However, for today's long-termists, viewing government bonds as ideal safe-haven assets may require more cautious thinking, especially in the current global economic landscape, when some data and facts have revealed the possible traps behind traditional ideas.

As we mentioned before, taking the US Treasury as an example, its size has exceeded 35 trillion US dollars in 2024. Such a huge debt scale and the fact that the real yield has been negative for 18 consecutive months point to a core question: Can Treasury bonds still effectively resist inflation?

Negative real yields mean that after deducting inflation, holding these so-called "safe assets" is actually losing purchasing power. For long-termists who pursue long-term value preservation and appreciation, this is obviously unacceptable.

In addition, the scale of global sovereign debt has reached 356% of global GDP, which is a worrying figure. In some countries, such as Japan, the proportion of government bonds held by the central bank has exceeded 50%, which has led to a sharp drop in the yen exchange rate. This trend of "debt monetization" has challenged the long-term security of some government bonds that have traditionally been considered safe. For long-term investors, it is not a wise move to invest a large amount of money in assets that may be at risk due to a sovereign debt crisis.

In contrast, as a decentralized digital asset, Bitcoin's value does not directly depend on the credit of any single country. Although it also faces its own risks, in the long run, it provides an option to decouple from the traditional financial system, which may be more attractive to long-termists who are concerned about sovereign debt risks.

Of course, as a low-volatility asset, government bonds may provide a certain degree of stability in the short term when the market is turbulent. However, for long-termists who focus on the next few decades and pay more attention to long-term wealth preservation and growth, simply pursuing short-term stability may not be enough. What they need is an asset that can resist long-term inflation and has long-term growth potential. From this perspective, despite the volatility of Bitcoin, its unique scarcity and decentralization, as well as its huge potential in the digital economy era, make it a better long-term safe-haven option than traditional government bonds.

4.3 Gold Vs. Bitcoin

As we mentioned before, gold has achieved an annualized return of about 7.3% over the past 50 years, making it a good long-term store of value. However, if we look at Bitcoin, its long-term performance is even more impressive.

According to backtesting data from Curvo.eu (as of March 2025):

Over the past five years: Bitcoin's total return was about 1,067.5% , while gold's was about 88.8% . Bitcoin's average annualized return was 63.5% , much higher than gold's 13.5% .

Over the past decade: Bitcoin's total return rate is as high as 51,259.5% , while gold is about 142.7% . In terms of average annualized return rate, Bitcoin is about 86.7% , which is also significantly higher than gold's 9.3% .

Nasdaq also pointed out in an article in September 2024 that over the past decade, Bitcoin has been the best performing asset in the world, with an average annualized return of 693% , while gold was only about 5% during the same period .

In addition, after the fourth halving, the annual inflation rate of Bitcoin is 0.9%, which is only 53% of gold (1.7%). Bitcoin will become increasingly scarce.

Secondly, portability and storage costs are another limitation of gold. Holding a large amount of gold requires physical storage space, which comes with security risks and storage costs. Bitcoin, on the other hand, exists in digital form and can be stored in a variety of electronic devices, with almost no storage costs and is easy to transfer around the world, which is an important advantage for an increasingly globalized world.

In addition, Bitcoin is far superior to gold in terms of divisibility . Bitcoin can be divided into eight decimal places (i.e. Satoshi), which makes small transactions and investments more flexible and convenient. The cost of dividing and trading gold is relatively high.

More importantly, as a digital asset born in the Internet age, Bitcoin is more transparent and verifiable . All Bitcoin transactions are recorded on the public blockchain and can be queried and verified by anyone, which reduces the risk of fraud and counterfeiting to a certain extent. The authenticity and purity of gold are sometimes difficult to identify.

In addition, from the perspective of market size growth , although the total market value of gold is still much higher than that of Bitcoin, the growth rate of Bitcoin is remarkable. Currently, the market value of Bitcoin is close to 2 trillion US dollars , while the estimated market value of gold is about 18.5 trillion US dollars . Galaxy Research predicts that by 2025, the market value of Bitcoin is expected to reach 20% of the market value of gold. This shows the market's strong expectations for the future growth of Bitcoin.

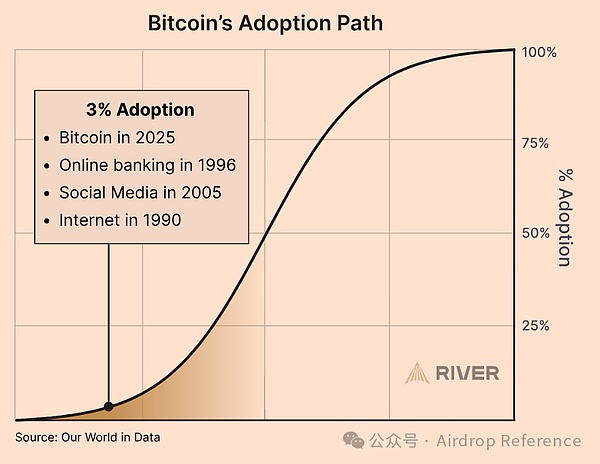

Finally, from the perspective of adoption rate , gold as a mature asset has been widely accepted, but Bitcoin as an emerging digital asset has an adoption rate of only 3%, indicating that Bitcoin has a broader future. As I pointed out in "Above the Trend, Between Cycles: Cold Thinking on Bitcoin's "Pullback Moment" , a 3% adoption rate is equivalent to the Internet in 1990 , online banking in 1996 , and social media in 2005 .

Long-termists choose Bitcoin not to completely abandon gold, but because they see that in the future, Bitcoin may show stronger potential than gold in fighting against the depreciation of legal currencies, protecting personal wealth, and seizing opportunities for the development of the digital economy. We are willing to bear volatility in exchange for possible future returns.

So, how should long-termists invest in Bitcoin?

Save enough living expenses and start DCA.

5. Why is DCA an investment approach for long-termists?

DCA is the acronym for Dollar-Cost Averaging, which is an investment strategy that involves investing a fixed amount of money to buy an asset at fixed time intervals (such as weekly or monthly), regardless of the price of the asset.

As we discussed before, as an emerging asset, Bitcoin's price volatility is much greater than traditional safe-haven assets such as gold and government bonds. Although we are confident in the value of Bitcoin in the long run, short-term price fluctuations are difficult to predict. For long-termists, they do not pursue profits brought by short-term market fluctuations, but focus on long-term returns in the next few years or even decades. In this case, the DCA strategy is particularly important and effective.

The most direct benefit of this phased investment approach is that it reduces the pressure on investors to try to "buy the dips" . No one can accurately predict the market's bottom, and even professional traders often make mistakes. Long-termists know this well, and they pay more attention to long-term trends rather than short-term fluctuations. The DCA strategy allows them to not have to guess when the market will bottom out, but only need to stick to the established plan to invest.

In addition, DCA can help overcome human weaknesses . When the market is rising, people tend to buy high because they are afraid of missing out; when the market is falling, they tend to sell at a loss because of fear. The DCA strategy helps investors stay calm and rational through regular investment, avoid being affected by short-term emotions, and thus be more able to stick to the long-term investment strategy.

Calculated based on the data from 2015 to 2025:

$100 DCA per month : total investment of $12,000, final value of $111,000, annualized rate of return of 25%;

During the same period, the S&P 500 Index DCA had a final value of only US$21,000, with an annualized return of 9.8%.

This difference comes from the exponential growth characteristics of Bitcoin . DCA is like "time-space arbitrage" in the Bitcoin ecosystem - exchanging the depreciation rate of legal currency for the scarcity premium of Bitcoin.

Looking back at the historical price trend of Bitcoin, we can see that despite several large corrections, its long-term trend is still upward. If an investor insists on using the DCA strategy from the beginning of Bitcoin, no matter how many times it is "cut in half", the final return on investment will be very considerable. Of course, past performance does not represent the future, but the essence of the DCA strategy is to diversify risks and reduce the impact of a single purchase timing on the final return.

For long-termists, we pursue a "once and for all" investment method and do not want to spend too much time and energy on researching and predicting the market. The DCA strategy meets this need. Once the investment plan is set, it can be automatically executed regularly without frequent operations, so that more time and energy can be invested in more meaningful things, such as personal career development, family life or social contribution.

Therefore, for long-termists who recognize the long-term value of Bitcoin and want to participate in it in a worry-free and labor-saving way, DCA is undoubtedly a very suitable investment strategy. You may ask, what should I do with the money that I didn't buy Bitcoin? It's very simple, just exchange it into US dollar stablecoins. Here is a zero-based tutorial on stablecoins .

In the cryptocurrency market, DCA is already a mature service with many ways to do it. If you want to buy Bitcoin directly on a centralized exchange and then send it to a cold wallet, here are two zero-based tutorials, one on how to buy Bitcoin ( https://t.co/2IzQI80lll) and the other on how to send Bitcoin to a cold wallet ( https://t.co/sbT1E9A3bw) .

What I recommend is the ARP2 project from "Airdrop Reference" , because with this project you can not only invest in Bitcoin on a regular basis, but also obtain additional benefits from automatic rebalancing. For detailed operations, please see here ( https://t.co/9E8Q9XWe0J) .

ARP2 still has a 43.77% return even when Bitcoin has plunged. The only downside to this project is that you need to manually complete the investment each time.

Conclusion : Value awakening across the time dimension

In the monetary epic of human civilization, gold has used thousands of years to build the "Temple of Value", legal tender has used national credit to weave "flowing illusions", and Bitcoin is reconstructing the "Digital Tower of Babel" with mathematics and codes. This debate on safe-haven assets is essentially a game between human nature and time - gold carries the ancient belief in physical scarcity, while Bitcoin heralds the future consensus on the absoluteness of numbers.

The choice of long-termists is never a simple asset replacement, but a redefinition of monetary sovereignty. When the "inflation tax" of fiat currency eats away wealth, and when the "geopolitical shackles" of gold restrict mobility, Bitcoin, with its transparency of "code is law" and control of "private key is sovereignty", has opened up a third way for individuals to fight against systemic risks.

History has repeatedly proved that true risk aversion is not about escaping volatility, but about anchoring the future.

Just as time will eventually reveal the vanity of all bubbles, it will also precipitate the light of true value. Bitcoin, a decentralized network based on mathematics and powered by consensus, is showing its potential to surpass traditional safe-haven assets in the test of time with its scarcity, verifiability and growing adoption rate.

Choosing Bitcoin is not a short-term speculation, but a belief in the future. It represents a new view of wealth - not relying on centralized authority, but returning the control of value to individuals. For those of us who are long-termists who do not want to waste our lives in the fog of chasing wealth, Bitcoin may be the key to open the door to future value.

Let us use the patience of time as our sail and long-termism as our rudder to sail towards the other side of wealth that is more independent and secure.