By Lyn Alden

Compilation: The Way of DeFi

After the collapse of Luna, Celsius, Voyager, 3AC, and FTX/Alameda, many crypto industry analysts pointed to DeFi (“decentralized finance”) as a potential solution.

This article unpacks some of the nuances of this view, acknowledging that certain opportunities exist but offering a fairly critical assessment of the current state of the industry as a whole.

Additionally, the article touches on a number of other concepts in the crypto industry, including Web3, NFTs, tokenized securities, and the broader problem of creating tokens that have no purpose other than to enrich the founding team.

Article sections:

- CeFi: The problem of opaque leverage

- What DeFi aims to achieve

- The Centralized Disadvantages of DeFi

- The Arbitrary Seigniorage Problem

- Upgrade Technology Track

- Pandora's box has been opened

1. CeFi: The problem of opaque leverage

According to the description, the benefits of DeFi are decentralization and increased transparency for various transactions and leverage services.

Therefore, before discussing crypto DeFi (“decentralized finance”), it makes sense to first analyze crypto CeFi (“centralized finance”).

In the crypto asset industry, the two major centralized companies that exist are exchanges and deposit/lending institutions. The term “CeFi” primarily refers to the latter, but more broadly, it can include both, especially because the two business models can be intertwined.

- Exchanges allow traders to exchange various crypto assets and usually provide leverage tools for traders.

- Deposit/lending institutions (aka “liquidity providers”) allow people to deposit crypto assets and earn yield, allow people to deposit crypto assets as collateral to borrow stablecoins or fiat currencies, and allow some institutions to borrow on an uncollateralized basis.

There are some other types of companies, such as pure custody, technology development, etc., but these are the two types of companies that are more relevant to DeFi.

A large part of the traditional financial system is opaque, and it is difficult to determine how much debt any given entity has unless it is publicly traded (a listed entity). Even then, it is still possible to commit fraud or use certain accounting tricks to obfuscate the details to some extent.

This problem extends to the CeFi crypto industry, and is even more problematic. Various trading firms and funds often use leverage to speculate on crypto assets, especially Altcoin. Since few of these companies are publicly traded, almost all of them are quite opaque, even when billions of dollars are involved.

Throughout 2021 and 2022, the crypto industry began to encounter cyclical problems. The early problems began when the Grayscale Bitcoin Trust (GBTC)'s net asset value premium turned to a net asset value discount. In other words, there was a time when the market price of the fund was $1.4 for every $1 of Bitcoin, and now, the market price of the fund's $1 of Bitcoin is less than sixty cents.

Chart source: YCharts

A lot of trading firms have leveraged exposure to this instrument, so this is a bigger issue for them than people might realize.

For many years, GBTC was one of the few ways to get exposure to Bitcoin in the form of a security, which is what many regulated entities want. As a result, GBTC once traded at a premium to net asset value "NAV" because it provided something that was difficult to obtain in this type of securitization portfolio.

As more funds and securities enter the market, providing these regulated types of entities with exposure to the Bitcoin price, GBTC becomes less unique and its premium disappears. Most closed-end funds trade at a slight discount to their net asset value, and GBTC is no exception.

The vast majority of my Bitcoin exposure is through outright purchases of BTC itself, however, in my brokerage portfolio, for lack of a better option, I use a small GBTC position to replicate Bitcoin price exposure. I rebalance its exposure from time to time, especially when its premium becomes too high:

Chart source: YCharts

GBTC is not only a way for portfolios to gain exposure to the price of Bitcoin, it has also provided accredited investors with an arbitrage trade for many years. They can 1) short Bitcoin and 2) send funds to GBTC to create new GBTC units at NAV. They must hold this position for a 6-month lockup period, and can then sell their GBTC shares at a premium above NAV and close their short Bitcoin position, thereby taking the premium above NAV as profit without exposing themselves to the risk of BTC itself and the volatility of the GBTC price. They can then repeat this trade over and over again.

This practice continued for a long time until it became easier to gain exposure to Bitcoin in a variety of other regulated vehicles, at which point the trust no longer had reason to pay the premium.

This caught many trading firms off guard because they were stuck with large short positions in Bitcoin and large long positions in GBTC, which, instead of trading at a premium as they had in the past, were now trading at a discount. In other words, they experienced significant losses on what they thought were low-risk trades.

So, that was the first shock.

I covered this reversal from premium to discount in one of my reports at the time, although I was primarily focused on the disappearance of buying pressure on Bitcoin:

“Compared to the structural bull run of the post-halving adoption cycle, Bitcoin currently faces two fundamental headwinds.

The first is the potential bond yields described earlier. If Bitcoin continues to rise, the U.S. dollar index remains strong, and liquidity becomes tighter, it should continue to put pressure on high-valuation growth stocks, and Bitcoin may also be temporarily classified by investors in this category, especially in a general risk-off environment.

Second, the Grayscale Bitcoin Trust (GBTC) no longer has a positive premium to its net asset value, or “NAV.” In fact, it trades at a slight discount to NAV. Canada now has a stable Bitcoin ETF, with companies like NYDIG and SkyBridge entering the market over time and providing competition for institutional and accredited investors to allocate to Bitcoin. Therefore, GBTC has less reason to command a premium. Most existing closed-end funds in other asset classes trade at a discount to NAV, and GBTC has, at least temporarily, joined the discount club.

This discount to NAV has pros and cons. It’s good because it makes GBTC a better vehicle for holding Bitcoin than it was in the past because you’re acquiring Bitcoin near NAV rather than at a premium. It’s bad because it eliminates one source of demand for Bitcoin.

GBTC is the largest buyer of Bitcoin in 2020, with a portion of it used for long-term exposure and a large portion used for market neutral arbitrage. For the second portion, qualified investors and institutions can buy GBTC at NAV during a six-month lock-up period, and then sell it at the market price six months later, which is usually higher than the NAV. While buying Bitcoin at NAV, they can short Bitcoin elsewhere, making non-directional investments, so that they can extract a premium over NAV every six months without being affected by the price of Bitcoin.

This process makes a lot of money for people and also permanently absorbs a lot of Bitcoin. GBTC basically converts liquid Bitcoin into illiquid Bitcoin, which is then locked in a cold storage wallet. If the GBTC premium remains minimal or negative, the transaction is closed, thus completing the specific source of demand and the conversion process of liquid to illiquid. "

-Lyn Alden, Premium Report February 28, 2021

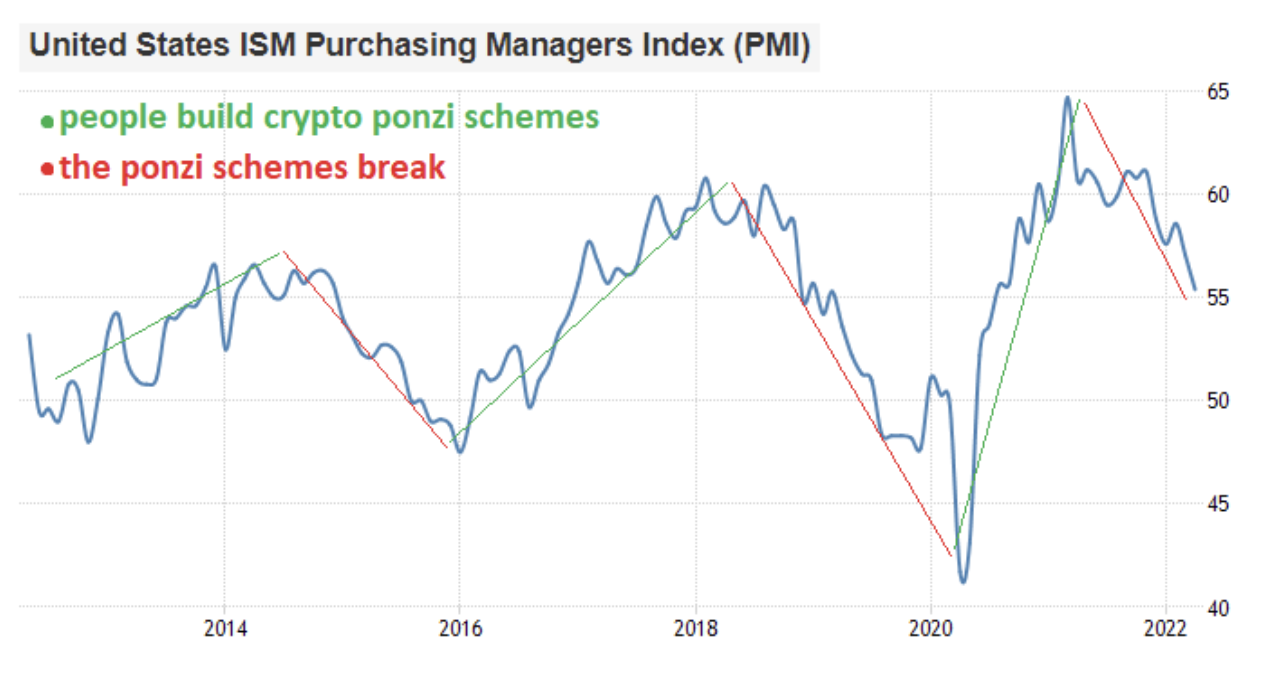

The second blow was when Terra/Luna collapsed, which was basically a Ponzi scheme from the beginning. The people involved lured retail investors with artificially unsustainable 20% annualized returns. I warned about Terra/Luna in April and May 2022 when it was near its highs, and then wrote a post-mortem analysis article in May 2022 called "Digital Alchemy".

One of the themes of the post-mortem is that crypto Ponzi schemes tend to be established when liquidity and general business conditions improve, and tend to be uncovered and collapse when liquidity and general business conditions deteriorate:

Chart source: Trading Economics, Lyn Alden notes

Many leveraged trading firms were exposed to Luna, which made the subsequent crypto industry shock more serious than I guessed at the time. The biggest surprise for many people was the fall of Three Arrows Capital (abbreviated as "3AC"), which was affected by the GBTC discount and then hit by the Luna collapse. The 3AC team had always been particularly bullish on Luna.

Three Arrows Capital (3AC) is a large crypto trading firm that has been around for a decade. They use a lot more leverage than most people realize because it is opaque and they quietly borrow money from a lot of different sources that they don’t necessarily communicate to everyone. Multiple institutions including Voyager and Genesis have provided 3AC with large unsecured loans. BlockFi also provided 3AC with a large loan, but it was secured, which reduced the overall impact on themselves. In addition to this, Celsius and dozens of other companies have also provided loans to 3AC.

The resulting 3AC implosion therefore destroyed a large swath of the crypto lending industry, with only a handful still standing. Overall risk control in the space is terrible, and while some companies are doing relatively well, many lenders only lend to a small number of equally large borrowers (like 3AC).

I explored CeFi platforms in early 2021 to get a feel for the ecosystem. I endorsed BlockFi in an article back in February 2021 as a small exposure to novelties like stablecoin yields, gold token yields, etc. I highlighted its risks, the fact that deposits were not FDIC insured, and suggested that one should only put a small portion of their assets in it at most, and keep the majority of their assets in custody. However, a year later, in February 2022, when BlockFi and the broader industry were still operating normally, I withdrew my endorsement because I no longer believed the risk/reward was worth it.

Unlike many lenders, BlockFi managed to survive the subsequent crypto lender crash of May/June 2022, while other CeFi deposit/lenders such as Celsius and Voyager failed. BlockFi’s avoidance of providing centralized unsecured loans at least minimized the hit to its solvency and provided them with a way to continue processing withdrawals and continue operating with the support of investors.

However, BlockFi subsequently sealed their fate by participating in the FTX/Alameda deal in June 2022, providing liquidity provision and a tender offer. After the FTX/Alameda collapse in November 2022, BlockFi had to stop processing withdrawals, joining most other deposit/lending institutions.

Overall, the biggest failures in the CeFi industry come from: 1) providing unsecured loans to leveraged entities with opaque balance sheets, or 2) custodial assets to leveraged entities with opaque balance sheets. Of course, the problem with opaque balance sheets is that it’s hard to know exactly how leveraged they are, especially when in some cases outright fraud is involved.

2. What does DeFi aim to achieve?

Unlike CeFi, trading and leverage also take place on various blockchains, often referred to as “DeFi.” As mentioned earlier, this stands for “decentralized finance.”

The foundation for this activity includes L1 smart contract blockchains such as Ethereum, Binance Chain, Tron, Avalanche, Solana, etc. These systems allow computing environments to be embedded into the blockchain. This effectively becomes a federated computing environment, meaning a computing environment that is distributed across multiple machines and can therefore be observed and confirmed by multiple different entities.

This computing environment can also be built on layers/sidechains on top of the Bitcoin network (e.g. Liquid or RSK), but to date, most activity has taken place on these L1 smart contract blockchains.

After the computational layer, the next layer consists of two main parts: decentralized exchanges (DEX) and decentralized deposit/lenders. Decentralized exchanges (DEX) allow traders to exchange various crypto assets, similar to how they do on centralized exchanges. Decentralized deposit/lenders (the most common term is "liquidity providers") allow users to 1) deposit crypto assets into the protocol to earn a yield, or 2) deposit crypto assets as collateral to borrow another type of crypto asset, with the most common assets in terms of deposits and lending being stablecoins. Whether these are really as decentralized as participants claim will be discussed later in this article.

After that, there are other types of DeFi assets. Most of these are equity/governance tokens associated with controlling these trading protocols and deposit/lender protocols and potentially earning profits from them.

However, there are still many questions in the long run. Here are some examples of what is possible with DeFi:

Person A has a bunch of Bitcoin, and he transfers those BTC into Wrapped Bitcoin (“WBTC”), so it is now a custodial bearer asset that is tradeable on the Ethereum network. They then deposit that WBTC into Aave (a borrower/lender protocol) as collateral to borrow stablecoins. They send some of those stablecoins to a centralized exchange and cash them out into fiat, which they then withdraw to a bank for daily spending. They have now leveraged, which presents multiple layers of counterparty risk such as hacks, custody issues, and the chance of liquidation if the price of Bitcoin goes too low.

B has a bunch of ETH, which he deposits into Aave as collateral to borrow a bunch of stablecoins. Then, B trades these stablecoins on a decentralized exchange called Uniswap in exchange for some DeFi governance tokens (such as AAVE, COMP, and UNI). Therefore, B uses ETH as collateral to buy a bunch of DeFi protocol governance tokens (AAVE, COMP, UNI).

C doesn't have much crypto assets, but he decides to convert some of his fiat into stablecoins and deposit these stablecoins in Aave and Compound to earn a yield. In this sense, C is funding the mortgage loans of A and B. Before the Fed raised interest rates this year, the yield on these stablecoin deposits was much higher than that of safer FDIC-insured bank deposits or Treasury bills, although the risk was much higher, so this use of capital is a bit competitive with junk bonds or similar methods, which are intended to obtain high returns.

If all this sounds familiar, here’s what I responded to in January 2021:

“One of my concerns when examining the biggest use cases for decentralized applications is that many of them are circular and speculative.

Ethereum is used heavily for decentralized trading of crypto tokens, crypto stablecoins as liquid units of account for trading crypto tokens, and for lending and earning interest on crypto tokens, a practice of providing a source of liquidity/borrowing for crypto token traders. To a lesser extent, it is also used in gamified ways to earn or trade various crypto tokens.

So it’s a massive operating system powered by crypto tokens, for the purpose of moving… crypto tokens around.

A healthy banking system in the real world would consist of people depositing money and banks making various loans for mortgages and business financing to generate real-world utility.

On the other hand, a banking system based on speculation would consist of a series of banks that take deposits and then make loans to speculators on nearby stock markets, as well as technology providers that make this easier, and then what those speculators are trading (consisting mostly of shares in those banks, shares in those tech companies, and shares on the stock exchanges), leading to a big circular speculative side. Ethereum’s biggest use case to date is a decentralized version of a circular speculative system.”

— Lyn Alden, Economic Analysis of Ethereum, January 2021

Nearly two years later, as we look back at the article I wrote when I was covering this industry in early January 2021, I really can’t say it’s any different. It’s been a party of cycles and speculation with little real-world utility, and the industry as a whole has barely improved on that front.

In fact, a March 2022 study found that 97.7% of tokens traded on Uniswap were rug-pull transactions, a process in which developers and investors hype a project and extract value from it as investor money pours in, but have no intention of actually executing on their plans.

The risk of DeFi vulnerabilities is everywhere

DeFi offers some transparency benefits, but it also provides a huge attack surface for hackers/attackers. These are often referred to as "DeFi hacks," where someone figures out how to steal funds from a smart contract. In reality, they are better viewed as exploits or arbitrage opportunities rather than hacks.

“Code is law” was a common adage in the early days of DeFi (and, of course, dating back to before DeFi). If there is a vulnerability in a smart contract, then someone can exploit it and potentially gain themselves an advantage, including even taking assets in ways that were not intended by the contract. This is similar to a poorly written real-world contract, where a clever lawyer can find loopholes and help a client abuse the contract in a way that was not intended by the writing. After all, what is the point of a smart contract if the code is not the ultimate arbiter of it?

The Bitcoin network is the most streamlined blockchain with nearly 14 years of operational history. It is intentionally simple, intentionally slow to change, and intentionally resistant to change except under overwhelming consensus. Despite this, the Bitcoin network has still encountered some serious vulnerabilities in the past few years.

So how do ever-changing, highly complex smart contracts survive attacks? Anyone holding funds in DeFi or other smart contracts should assume that the risk of code exploitation and loss of funds is always there. You get a 3% yield on it? Weigh that against the probability of a 100% loss at any time of the year, and repeat it year after year. The risk is further amplified when smart contracts from different blockchains or different layers interact with each other.

Over $2.5 billion worth of crypto assets have been stolen from smart contracts in the past two and a half years:

Chart Source: The Block

Collateralized vs. Uncollateralized: That’s the Key

Many DeFi supporters point out that most CeFi lenders collapsed in 2022, while DeFi contracts continue to operate.

While this makes some sense, we should look at the root cause: collateralization. CeFi lenders that offer fully collateralized loans are also generally doing well, and if they have to liquidate a client, it’s the client that goes bankrupt, not the lender. The problem occurs because CeFi lenders provide under-collateralized or uncollateralized loans to entities they believe are trustworthy (who then gamble in DeFi, such as LUNA tokens, and are unable to repay the loan).

Due to the automated nature of DeFi, it is difficult to do this in a meaningful way without overcollateralization. Therefore, by its very nature, DeFi consists mostly of overcollateralized leverage. The lesson here is not that DeFi is better than CeFi, but that overcollateralized loans are safer than undercollateralized or uncollateralized loans when it comes to volatile assets.

In a DeFi environment, depositors are primarily exposed to collateralized loans (a good thing in terms of lending), but also face ongoing smart contract exploitation risk (a bad thing). In a CeFi environment, depositors may be exposed to some mix of collateralized and uncollateralized loans (a bad thing), but are better protected from exploitation (a good thing).

My conclusion from the crypto industry events in 2022 is not that DeFi is better than CeFi.

Instead, I conclude that chasing yield is inherently unwise in these highly volatile assets. Prudent lending should be primarily overcollateralized.

Bitcoin provides users with the ability to self-custody a limited liquid asset and use it to send or receive permissionless payments without relying on a centralized third party. In my opinion, this is a signal in the noise that is more powerful than many people realize.

Using stablecoins for savings and payments in the medium term is another good practical use case in developing countries where USD is difficult to access. They should be aware of counterparty risk, and in general I would like to see more transparency around stablecoin collateral.

Almost everything else involves speculation, or involves picking up pennies (yields) in front of a steamroller (opaque counterparty risk or code exploits). The fact that I was in it for a year with very little capital and stopped investing even before the crash happened is a mistake I think I made when navigating this industry.

3. Centralized Disadvantages of DeFi

In addition to being circular, speculative, and sometimes outright fraudulent, DeFi also has a centralization problem at its core, even though it is marketed as decentralized.

Centralized smart contract blockchain

The foundation of the DeFi technology stack, the underlying smart contract blockchain, already starts with some centralized aspects compared to the more decentralized Bitcoin network.

For example, the Ethereum network had a difficulty bomb in the code for more than 7 years, from its birth in 2015 to the PoS transition in 2022. This reduced the power of miners and individual node operators and strengthened the power of head developers, which is a form of centralization that allows them to advance the roadmap and change the protocol according to their vision, which basically makes it an investment contract. Even after the Proof of Stake (PoS) transition in 2022, network users will still need to wait for developers to implement staking withdrawals.

At the same time, Binance can request to suspend the blockchain when problems occur with Binance Smart Chain, as it did between October 6 and 7 this year. In theory, Binance Chain is a decentralized system independent of the centralized company Binance, but in reality:

Source: CZ, the CEO of Binance (via Twitter)

Similarly, when Solana unexpectedly went offline five times in 2022, validator operators had to meet via Discord to manually restart the blockchain.

Many PoS chains operate in this way, and the technical or financial requirements to become a validator are very high, which ultimately makes the operation of the system quite oligopolistic.

Unlike proof-of-work (PoW) protocols, proof-of-stake (PoS) protocols do not have an unforgeable ledger history, so if the system goes offline intentionally or accidentally, a fairly manual process is required to determine where the appropriate checkpoint is and where to restart the network from. Since it is costless to create an almost infinite number of alternative histories, each of which appears to be valid, there is no unforgeable, self-verifying way to determine the "true" history of the ledger in a PoS system (this is what PoW specifically does), so using PoS checkpoints requires trusting some authority or group of authorities.

This is why there are projects like Babylon Chain , which allows PoS chains to insert unforgeable timestamps into the Bitcoin blockchain. It attempts to mitigate some of the inherent circularity issues of PoS systems by using the dominant PoW proof-of-stake system, using the Bitcoin network as a checkpoint authority.

In addition to the problems of centralized difficulty bombs, centralized developer decision making, centralized validation, and centralized checkpoint authority, there is the simple problem that, in most cases, smart contract blockchain nodes are too big.

Optimal blockchain privacy and decentralization requires users to run their own nodes, or at least have a practical option when they need to. This enables them to verify various aspects of the network themselves and allows them to initiate transactions themselves, rather than requiring a third party to initiate transactions for them.

However, by adding higher throughput or more code expressiveness to the base layer of the protocol, it increases the processing, storage, and bandwidth requirements for running a node. For example, to run a Solana or Binance node, you almost need enterprise-grade equipment or use a cloud provider.

Ethereum nodes are lighter than those of Solana or Binance Chain, but still too bulky to run on Tor. According to ethernodes.org, there are only about 6,700 Ethereum full nodes. Of these, more than 4,400 are hosted by vendors (usually cloud services), 2,700 of which are hosted exclusively through Amazon, and only about 2,300 are non-custodial nodes.

Most users and applications instead rely on third-party node operators like Infura and Alchemy (which themselves make heavy use of cloud providers). When the U.S. Treasury sanctioned privacy-focused smart contract Tornado Cash in August 2022, Infura and Alchemy complied and stopped processing transactions related to Tornado Cash. This meant that many foreigners, including those not even subject to U.S. sanctions, could not use Tornado Cash unless they were willing to run their own Ethereum node, which is not an easy task.

In contrast to all this, when Satoshi Nakamoto invented Bitcoin, he deliberately made sacrifices in bandwidth and complexity to make it as small, simple, and decentralized as possible.

This makes it easy for an individual user to run a Bitcoin node on a laptop with a working internet connection. The requirements for running a node scale more slowly than technological improvements in processing, storage, and internet bandwidth, so running a Bitcoin node will get easier, not harder, over time. The goal of the Bitcoin network from the beginning was to trim all unnecessary fat to make it as lightweight as possible.

"Governments are good at cutting off the heads of centrally controlled networks like Napster, but pure P2P networks like Gnutella and Tor seem to be able to hold their own."

- Satoshi Nakamoto, November 2008

Centralized custody assets

In addition to some centralized aspects of the underlying smart contract blockchain that the DeFi industry relies on, actual DeFi use cases tend to be more dependent on centralized entities.

The vast majority of DeFi’s total locked value relies on centrally managed stablecoins and other centrally managed assets. In pseudo-decentralized deposit and loan protocols, stablecoins account for a large portion of lending, and stablecoins are a common trading pair in pseudo-decentralized exchanges.

A fiat-collateralized stablecoin, such as USDT or USDC, is one where a centralized issuer holds an asset in the form of a bank deposit, treasury bill, repurchase agreement, commercial paper, or similar asset, and issues a redeemable token liability that can be traded on the blockchain. In other words, there is a centralized issuer that manages the collateral and handles redemptions, but the liability is a digital bearer asset that the holder holds, and can therefore be traded efficiently and automatically between people without further action by the centralized issuer. However, centralized issuers can still choose to proactively freeze specific addresses based on requests from law enforcement or due to various code vulnerability exploits.

In addition to its heavy reliance on centralized custodial stablecoins, DeFi on Ethereum also makes extensive use of Wrapped Bitcoin (WBTC), a custodial product whose token liabilities can be traded on the Ethereum blockchain or used for collateralized lending. The amount of Bitcoin held in custody on the Ethereum network is comparable to the amount of Bitcoin held in custody by even the largest crypto exchanges. Like stablecoins, WBTC is a centralized product whose liabilities are bearer assets.

Bad things have already happened on Solana, which also has wrapped BTC and ETH, but because FTX is the issuer of these assets, with the bankruptcy of FTX, these custodial assets have experienced decoupling and lost almost all of their value:

Chart Source: Coin Gecko

Attempts at synthetic stablecoins

Some stablecoin developers seek to move away from reliance on centralized issuers and custodians. After all, if much of the value of assets traded on “decentralized finance” protocols are themselves completely centralized, is the term even appropriate? Just because a centralized entity’s liability is a bearer asset token doesn’t make the system decentralized.

For example, MakerDAO launched DAI a few years ago, which was originally a synthetic stablecoin with ETH as collateral asset. This means that DAI is not directly redeemable for US dollars like USDT or USDC, but is backed by over-collateralized ETH and balanced by a stabilization algorithm to synthetically represent one US dollar.

Fiat currencies are centrally managed ledgers, and attempts to link pseudo-decentralized ledgers (such as crypto-collateralized stablecoin protocols) to actively managed and centralized ledgers (such as the Federal Reserve System) always come with various limitations and risks. In this case, using an unstable asset as collateral means that the probability of sudden liquidation of that collateral is quite high. During periods of market turmoil, it is easy for sudden liquidations to occur, leading to blockchain congestion and extremely high transaction fees because too many people are scrambling to exit at the same time, triggering too many liquidations at the same time, and the network cannot properly handle it.

In March 2020, during the global market crash associated with the COVID-19 pandemic and the lockdown of various economies, ETH prices plummeted, and in an emergency, MakerDAO was forced to vote to add the centralized USDC stablecoin as one of the collateral for DAI. This is because crypto-collateralized stablecoins (basically an attempt to back low-volatility assets with high-volatility assets) are inherently either fragile or capital inefficient. Since then, USDC has been a large part of DAI's collateral. If the government demands it, then the USDC issuer can freeze DAI's collateral at any time and basically terminate the project.

In order to have an arbitrarily low liquidation probability, a crypto-collateralized stablecoin needs an arbitrarily high overcollateralization ratio. In simple terms, if you want your stablecoin to not have to be liquidated even if the collateral loses 75%, you need an overcollateralization of 4 to 1. If you want your stablecoin to not have to be liquidated even if the collateral loses 90%, you need an overcollateralization of 10 to 1.

It would be extremely capital inefficient if handled this way, so most protocols will try to work around these levels, relying on incentives to bring in more collateral from the community when needed rather than keeping it there all the time.

For example, newer crypto-collateralized stablecoins such as Liquity and Zero aim to achieve 100% crypto collateralization through incentive mechanisms. Liquity’s “LUSD” is collateralized by ETH, and Zero’s “ZUSD” is a fork on the RSK sidechain of the Bitcoin network, which is collateralized by RBTC (RBTC is RSK’s merged mining packaged version of Bitcoin.)

The way this works for Zero is that when someone deposits RBTC as collateral into a smart contract and receives a loan with ZUSD as its collateral, a ZUSD synthetic stablecoin can be created. If they are liquidated (which would happen if the value of RBTC falls below the contract’s maintenance threshold), they lose their RBTC but keep their ZUSD. The system is optimized for overcollateralization at 1.5x or higher levels overall, though individual loans may be as low as 1.1x. If the system as a whole reaches a level of collateralization below 1.5x, it liquidates loans that are below 1.5x collateralization and changes the incentives for borrowing to encourage higher levels of collateralization. Importantly, there is a stable pool that incentivizes holders of ZUSD to deposit and back loans. If a loan is liquidated, these ZUSD depositors convert their funds into RBTC at a discount to the RBTC market price (which is conceptually a bit like selling a put option to wait and buy RBTC at a discount, since most participants are generally bullish on RBTC).

These incentives are interesting. LUSD has been around longer than ZUSD (and is the basis of ZUSD), and has managed to maintain its peg to the USD during the 2021 and 2022 bear market, when ETH (the collateral for LUSD) was down about 80% from its highs. Here’s a May 2021 article analyzing how it held up well during the ETH flash crash, thanks to a working oracle and a working stablecoin pool. However, it’s been running for less than two years overall, and LUSD is minuscule compared to fiat-collateralized stablecoins like USDT and USDC, which means DeFi as a whole is still very reliant on custodial assets.

All else being equal, I think BTC is a better collateral than ETH, so I would naturally prefer DeFi on the Bitcoin network, at least to the extent that I’m interested in DeFi. I don’t plan on leveraging my Bitcoin, and I’m happy holding bank dollars, money markets, or short-term T-bills, so I’m not really the target audience here.

Continued holders of LUSD and ZUSD must also have confidence that 1) the underlying smart contracts will not be exploited in the foreseeable future, 2) the incentives will continue to work in the foreseeable future to appropriately maintain overcollateralization under all market conditions, 3) price oracles will not be exploited in any destabilizing manner, and 4) the governance of the smart contracts will not be misaligned or otherwise captured by users (referring to either specific contract governance or the underlying computational layer governance).

The Centralized Oracle Problem

Connecting digital assets to real-world information involves a centralized oracle, or a quorum of several centralized oracles in an attempt to decentralize the oracle’s readings. The oracle is the source of information that smart contracts need to perform their functions.

For example, pegging a crypto asset to the U.S. dollar means that the smart contract needs to know what the price of the crypto asset is in U.S. dollars, which means it needs information from exchanges.

Likewise, sports betting smart contracts require an external source of truth that gathers information from real-world sports matches so that the smart contract can award earnings to winning speculators.

This reliance on one or more oracles represents another point of centralization. Who controls the oracles? How easy is it to manipulate a given oracle or set of oracles and exploit the contract?

Centralized Governance Action

Many deposit/lending protocols and trading protocols have centralized web-based user interfaces, and centralized companies that support them. The underlying technologies may be open source and accessible without them (requiring users to run nodes, or be technically hands-on), but for most users, the web-based user interface is how they access the service.

These centralized companies and interfaces already have a history of removing certain tokens from their trading or leverage environments, either at government request or voluntarily to avoid violating securities laws.

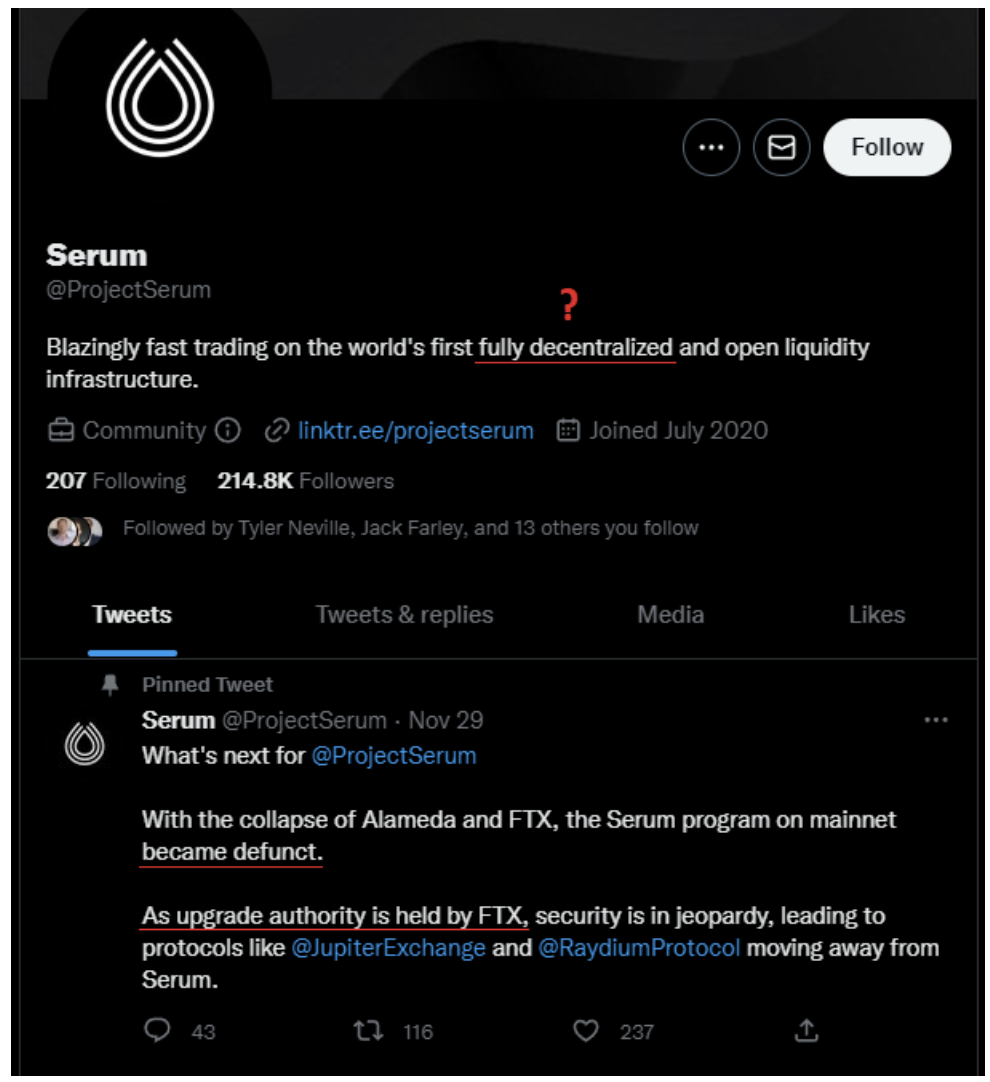

And many of these systems are more centralized than they appear. For example, as Jameson Lopp pointed out earlier this month, a DeFi protocol called Serum on the Solana blockchain markets itself as fully decentralized in its Twitter bio and elsewhere, yet below its bio is a tweet about how it fails due to centralized control.

At the time of writing, you can see the following on their Twitter profile:

Source: Project Serum (via Twitter)

How can it be considered “fully decentralized” if a centralized entity has upgrade authority?

Many of these protocols attempt to answer this question by using governance tokens to break control of the service. Either from an initial token offering or an airdrop to users, and allow for voting on various governance actions related to the operation of the service. These same tokens can also share in the profits generated by the protocol.

While this is interesting in theory, it starts with a few problems.

First, like most things in crypto, the vast majority of governance tokens are held by whales, meaning a small number of wealthy entities retain controlling stakes in voting rights.

Second, voter turnout tends to be low, allowing highly active and incentivized entities to have greater control over the governance of the protocol in practice.

Third, because it’s anonymous, these governance models are often easier to game than real-world democracies. Paying for votes, entities secretly controlling a larger share of governance than the market realizes, and other issues make it difficult to operate in a truly decentralized way.

Ethereum co-founder Vitalik Buterin recently raised the economic issues associated with governance tokens, and I agree with him:

Source: Vitalik Buterin (via Twitter)

Thus, sustained profits may be able to support the value of tokens (e.g., digital equity securities), but governance alone is not sufficient for tokens to maintain sustained value. Regardless of whether they are profitable or not, they are likely to be centrally held and controlled in practice.

Overall, DeFi protocols are likely to face greater scrutiny and regulation over time, and because they have so many centralized attack surfaces, it won’t be hard for regulators to clamp down on them, reduce their usability, and increase their traceability.

In the DeFi ecosystem, its blockchain nodes mainly run on centralized cloud providers, most of its locked value is heavily dependent on centralized custodians, and users mainly interact with the ecosystem through centralized web interfaces maintained by centralized companies.

DeFi cannot solve the bottleneck of fiat currency channels

One of the criticisms of Bitcoin by those in the DeFi industry is that Bitcoin is heavily dependent on centralized exchanges and brokers, with the vast majority of its transactions occurring on centralized exchanges or through centralized brokers.

“This is why we need DeFi,” many of them said.

However, we need to conceptually distinguish between 1) post-entry speculation/trading and 2) actual entry and utility.

If you want to trade in DeFi, how should you get started? Can you magically transfer your funds into the DeFi ecosystem? Of course not. First, you need to transfer money from your bank to an exchange with a fiat currency on-ramp, such as Coinbase or Kraken, or you can go through other centralized payment providers. Then, you can purchase various crypto assets and move these crypto assets into the DeFi environment. From there, you can trade and utilize these crypto assets in various smart contracts.

Therefore, DeFi does not eliminate the bottleneck of relying on centralized exchanges or centralized bank connections to solve the fiat currency entry part. DeFi only provides a post-onramp smart contract environment to trade or utilize crypto assets as a competitor to the alternative of staying on these exchanges to trade and utilize crypto assets.

But how many people should actually be trading or leveraging crypto assets? These are not “banking” services, these services are primarily provided for speculators.

On the other hand, the Bitcoin network has a similar on-ramp bottleneck. You wire money to an exchange or broker, buy Bitcoin, and then withdraw it. From that point on, you are financially “sovereign,” meaning you can self-custody your Bitcoin and use the decentralized network to send or receive permissionless Bitcoin payments around the world. Also, if for some reason you want to get a loan (in fiat or stablecoins) while using Bitcoin as collateral, you can use some multi-signature escrow services.

If centralized exchanges are locked out of the banking system, the only way to get around the on-ramp bottleneck is peer-to-peer purchasing (besides mining, which is how people first got into Bitcoin before exchanges existed).

There are methods like Bisq, RoboSats, Hodl Hodl, Paxful or Azteco for those who do not want to buy Bitcoin through centralized exchanges and sometimes need anonymity. The downside is that liquidity is limited and these types of services are only suitable for buying and selling small amounts of Bitcoin. However, if centralized exchanges were excluded from the banking system, the number and size of such services could increase significantly.

As a tangible example, Nigeria shut out crypto assets nearly two years ago. Nigerian banks do not allow customers to send money to crypto exchanges. Yet Nigeria has one of the highest bitcoin/crypto adoption rates in the world on a per capita basis, with the country’s bitcoin/crypto asset adoption rate far higher than the country’s central bank digital currency, eNaira. How is this possible? Because they use a variety of peer-to-peer methods to acquire bitcoin. They can even do remote work like programming or graphic design and pay foreign clients in bitcoin directly to their own custodians, who can then use bitcoin for global payments.

Nigeria’s official consumer price index has generally increased about fivefold since 2010 due to an expanding money supply, and when authorities have arbitrary powers to freeze protesters’ bank accounts, there will certainly be a willingness to adopt crypto assets.

Bitcoin’s “killer app” is simply using it for what it was originally designed to do: self-custody and send/receive permissionless payments in the most decentralized, secure, and immutable crypto asset to date.

Trading/leverage is something a subset of Bitcoin holders may choose to do, but it’s not like the world desperately needs more ways to speculate on 10,000 crypto assets, especially when DeFi is only built on top of centralized infrastructure.

Conclusions and further reading

In conclusion to this section, DeFi environments attempt to solve real trading/leverage problems, but are typically composed of multiple layers of centralized components.

-The underlying smart contract computation layer is often not as decentralized as claimed, thanks to validator oligopoly or developer control, reliance on checkpoint authority due to no unforgeable ledger history, and general difficulty in users’ ability to run nodes due to high bandwidth and storage requirements.

-Any non-trivial tradable asset that involves some external data (like a price or some real-world connection) will require some centralized or partially centralized custodian or oracle.

- Governance in practice, even for purely digital assets, tends to be centralized and can be traced back to a centralized commercial entity or a small group of individuals.

- Any potential areas of actual decentralization in leverage/trading protocols that may emerge in the industry will only apply once speculators get past the fiat on-ramp bottleneck, which DeFi does not solve.

For those who want more details on the speculative nature of DeFi, circular leverage, or centralization issues, I recommend “Only the Strong Survive ” (a September 2021 research report by Allen Farrington and Big Al) and “ Green Eggs and Ham ” (a long research article by Allen Farrington and Anders Larson).

4. The problem of arbitrary seigniorage

When founders and early-stage venture capitalists (VCs) form a tech startup, they often tie their wealth to the success or failure of that idea. They invest in illiquid equity, and the primary ways to unlock that stock and achieve successful exit liquidity include going public or being acquired.

To go public, they must go through a costly disclosure process in which they open their books, disclose major ownership and discuss risks in detail. The average length of time it takes for a startup to go public is more than eight years.

To be acquired, they need to build something attractive enough that other businesses will want to acquire them. In other words, professionals with MBAs or other business experience/education will review their business and then decide whether to acquire it.

Therefore, the wealth of startup founders and early investors is often tied to the fundamentals of the businesses they build and fund. Companies need some revenue, some use cases, and some level of due diligence. They have to spend years building a company that either another company wants to acquire, or get big enough and stick around long enough to go public and make all the necessary disclosures.

But in the crypto world, things are different. Founders and early investors can create a project, sell tokens publicly (usually to accredited investors or overseas to avoid today’s public securities laws), work on it for a year, two, or three years, market it heavily, get it listed on crypto exchanges, and then dump the hyped tokens (which may be unregistered securities) on the public retail speculators, making exaggerated or completely false claims about the project’s level of decentralization and utility.

In other words, founders and early investors can separate their profits from the actual success of the project's fundamentals. They don't need to spend 10 years to build a business good enough for another corporate to want to acquire, nor do they need to go through the SEC process to enter the public market. To exit liquidity quickly, they can hype up and dump their tokens to retail investors.

“Seigniorage” is the profit a government makes from issuing its currency, specifically related to the difference between the cost of production (which is close to zero) and its market value. Blockchain technology enables private entities to benefit from seigniorage as well. They can create a crypto semi-liquid/fungible asset at very low cost, hype it up, and try to profit from it. Because so little value is created in the process, it’s essentially a zero-sum game, with token creators and promoters making money and retail speculators losing money.

Bitcoin does not meet the definition of a security because it never raised money. Instead, open source software was created and then just sat there. Based on on-chain analysis, it is clear that Satoshi did not sell his Bitcoin either, as Satoshi left the Bitcoin community as early as 2010 without any obvious financial interests, and the Bitcoin network continues to exist in a fairly decentralized manner without him.

However, the technology created by Satoshi Nakamoto to enable peer-to-peer payments and savings has also been repurposed by others for peer-to-peer scams, fraud, and the hype and dump of digital penny stocks in the broader cryptocurrency industry.

As this continues to happen, I think one of two things will happen.

First, regulators in more countries may step up their crackdown on the practice. The United States has already restricted the ability to sell unregistered initial coin offerings (ICOs) to the onshore public, and they may further restrict the ability of onshore exchanges to sell tokens to the public after the offering.

Second, regardless of whether regulatory risks materialize, people will get burned by the crypto industry over and over again until they start associating crypto with scams, which has already happened to some extent.

“Does the project need a token?”

The problems in the crypto industry have nothing to do with cryptography, and no one would blame any developer for researching interesting technologies and building interesting projects.

The ethical issues only arise when they try to make millions of dollars from this work before it is fundamentally successful.

When evaluating any Crypto project, if it has its own token, we always have to ask, “Does it really need a token?”

The usual answer is no, the reason it has a token is so that the creator/founder can benefit in terms of quick exit liquidity, regardless of whether the underlying project provides any real value in the long run.

For example, let’s say someone invented a ride-sharing app called Rebu, except that it’s labeled a “decentralized” Web3 project. The founding team and early investors create their own Rebu tokens, keep most of them to themselves, and sell some of them to raise money. They spend two years developing the app, hyping it up, getting the Rebu tokens listed on some Crypto exchanges, and then a lot of retail speculators buy these tokens (which are probably unregistered securities, even though they are now sold to the public), at which point the Rebu developers and early investors use this opportunity to exit their Rebu token positions for huge gains of millions of dollars. Then people realize, “Wait, isn’t it easier to buy Rebu services with dollars than to convert dollars into Rebu tokens first? Isn’t this adding unnecessary friction?”

Then the project will go nowhere and eventually fall apart, with the Rebu token plummeting in value but the developers and early investors having exited and become rich.

Web3 is the Crypto industry’s marketing term for a project that aims to provide a more decentralized internet experience than the Web2 we’ve become accustomed to. While the goal is admirable, the problem is that most of these projects want to issue their own tokens, most of them are not truly decentralized, and most of them will fail (although many of the creators will get rich anyway, thanks to quick exit liquidity).

There have been a number of developments that offer alternatives.

For example, Block, Inc. (SQ) has a business unit called TBD that has been working on what they call “Web5,” a set of technologies that allow for decentralized interactions without the need for new tokens. Block’s CEO Jack Dorsey has been critical of the problematic financial incentives that exist for Web3 and its associated tokens, while acknowledging that the goal of creating a more decentralized internet is an important one.

As another example, many developers have been building technology stacks using Hypercore protocols. Example technologies in this regard include Slashtags and Holepunch. As these technologies mature, they may allow decentralized identity and decentralized applications, which covers most of the goals of Web3 technologies. These Slashtags and Holepunch protocols do not have tokens because they are not required.

I’ve been testing and using Holepunch’s first app called Keet, which is a peer-to-peer encrypted video, file sharing, and chat app that also has Lightning payments built in. Keet is still in alpha development at the moment, but so far it works pretty well, and if you only have a few people on a video call, it’s higher resolution, lower latency, and more private than server-based offerings like Zoom.

Another technology that these teams are working on using the Hypercore protocol is called Pear Credit, a peer-to-peer accounting system that, if successful, would allow for stablecoin transfers, as well as other centralized bearer asset transfers, in a very efficient manner without the need to attach a separate token.

This is still a vibrant space, but it’s important to remember that the vast majority of cryptocurrencies that have been created have not been able to consistently accrue long-term value. Many of these projects are sweepstakes and often exist solely to allow the creators to financially benefit from the project, regardless of whether the underlying project ultimately succeeds.

As I pointed out in my Digital Alchemy article, of the more than 20,000 coins in the history of the industry, only three have hit new highs in Bitcoin terms during their second crypto bull cycle.

If you look around and don’t know where the exit liquidity is, you are exit liquidity.

5. Upgrading the technology track

I have been interested in Bitcoin and stablecoins for many years and will continue to be so.

With Bitcoin, a fairly decentralized system allows users around the world to make permissionless payments and self-custody limited bearer assets. It comes with volatility and risk, but is a real innovation and, in my opinion, will continue to offer great promise in the long run. Looking around the world, it is hard to underestimate how many people have savings or payment problems, either due to persistent inflation and currency failures in developing countries, or due to authoritarianism and financial censorship.

With stablecoins, a centralized issuer creates a dollar liability in the form of a bearer asset, backed by collateral, allowing people to use dollars in jurisdictions around the world that would otherwise be difficult for many to access. Stablecoins carry counterparty risk, but that can be mitigated by greater transparency around collateral. I’m less interested in stablecoins used by wealthy people in developing markets for leverage/trading, but I’m very interested in stablecoins used by people in developing countries for small payments and savings.

Are there other use cases for blockchain technology or similar types of distributed ledgers? In theory, yes, of course.

What both of these types have in common is that, like stablecoins, they have a centralized issuer, but the liabilities can be traded as bearer assets in an automated fashion, which can provide tremendous utility. In other words, they represent the potential for upgraded technology for the trading, settlement, and custody of centralized securities.

Tokenized currencies and securities

The normal trading window for US stocks is 9:30am to 4pm, 5 days a week, for a total of 32.5 hours. Since there are 168 hours in a week, this means that US stocks are only available for trading 19.3% of the time. Subtracting some holidays, this may drop to around 19%.

Is it reasonable to expect stocks to trade the other 81% of the time, just like Bitcoin and other crypto assets? I think so.

Additionally, stock and other securities trades take days to fully settle. Stock settlement time has shortened over the years, but it still runs on traditional settlement rails. What if every trade could be fully settled in minutes?

Finally, investing in stocks in general is quite difficult for most people in developing countries (at least outside the upper classes). This applies both to their domestic stocks and to U.S. stocks.

What if traditional securities like stocks and bonds, as well as all commodities and currencies around the world could be tokenized, accessible to anyone in the world with a smartphone, traded 24/7, and fully settled in minutes? Like stablecoins, they would still be centrally issued, but the liability side would be a digital bearer asset, and a fairly efficient one at that.

Tokenizing traditional assets seems like a reasonable expectation, simply an upgrade to the technological rails on which existing securities operate.

Digital Collectibles

NFTs, or digital collectibles, continue to attract interest from some.

These can be in the form of digital artworks, or, they can be in the form of video game items that can be transferred to other games or traded on the open market outside of the game. They can also be things like concert tickets that can be transferred as digital bearer assets. Some people may use them to directly support their favorite musicians or artists.

Back in my January 2021 article, I expressed my openness to the idea of digital collectibles, for example discussing some plausible use cases for crypto game NFTs:

“There are a lot of crypto-based games these days. I’m not as into gaming as I used to be, but if I were, I could certainly see why blockchain could add something valuable to the gaming ecosystem. The idea of allowing users to own items/pets/characters independent of the game publisher, and potentially even having those items/pets/characters recognized by other games, is certainly cool.”

-Lyn Alden, Ethereum Economic Analysis, January 2021

In July 2022, analyst and venture capitalist Nic Carter proposed the idea of twin NFTs, where a physical luxury item has a chip in it that has a related NFT.

“Most tech-savvy luxury brands have probably thought about ‘making an NFT’ in the last year. Hopefully, they’ve thought better of it. Now that the hype has cooled, these brands will begin to realize that the real innovation is not exploiting fans by selling them overpriced JPEGs of questionable utility, but by combining merchandise with a durable digital asset. This elevates a sweatshirt from a piece of cloth printed with a logo to a verifiable representation of a brand in the emerging digital realm, a long-term, solid communication channel between consumer and issuer, an anti-counterfeiting device, and a fair means of secondary transaction.

[…]

Wearing the shoe, location triggers give you access to more experiences. Your wallet is filled with goodies — a POAP here, a discount there. You find NFTs that give access to events thrown by designers. Your ticket to their next art show is a chip embedded in the shoe. You earn skins by attending events and use it immediately to customize your digital version of the shoe. Basic biometric monitoring tracks how long you wear the shoe and builds a usage profile along with location data. Some users prefer invisible mode, but you don't mind sharing your data — you allow it to be released to the manufacturer in exchange for USDC paid directly to your wallet.

Later, you decide to sell the shoes. You make a deal with the buyer, place the NFT and funds in escrow, and mail the shoes. When they get the package, they scan the label to make sure they’re receiving the real thing. They verify that the shoes are in good condition, and the escrow releases the NFT to the buyer and the funds to the seller.

–Nic Carter, Redeeming and Retaining NFTs Is the Future of Luxury, July 2022

Similarly, Coinkite has a product called SATSCHIP, a chip that can be embedded into physical artwork. As they describe it:

“Think of it as a Bitcoin private key that an artist can embed into a work of art! The piece comes with the private key, it is never separated from the artwork and cannot be used by the artist after the artwork is sold.

[…]

The purpose of SATSCHIP is to allow artists to embed Bitcoin value into their works.

Any passerby can verify the originality of a work with a tap of their phone. The owner of the work can sign a message with their private key at any time to verify their ownership and control of the work. "

– Coinkite, SATSCHIP FAQ

I’m not a big fan of art or consumerism, so these trends don’t really apply to me, but I wouldn’t deny that they are potential larger markets that could emerge. I really don’t know.

But in practice, whether it’s digital art, digital gaming items, physical and digital items, or something else, current iterations of NFTs are highly speculative and rife with purposeful price manipulation (which is easier to do with NFTs than with highly liquid assets). Rather than making a game that’s inherently fun and then seeing if some transferable value can somehow enhance the fun of the game, developers will often create uninteresting games and then put tokens or NFTs into them.

In my reporting over the past year and a half, I have been less than enthusiastic about the industry as a whole so far:

“The most expensive trading cards in the crypto world are worth millions of dollars, so I guess I’m not one to judge what art is. However, I can get a set of rookie cards of Michael Jordan, LeBron James, Kobe Bryant, Wayne Gretzky, and Tom Brady, as well as the rarest Black Lotus card from Magic: The Gathering, and a first edition Fire Dragon card from Pokemon, all for less than a top-tier Alien CryptoPunk. I think I’d take all of those cards instead of a CryptoPunk, as the risk/reward is clearly not attractive in my opinion.”

-Lyn Alden, August 8, 2021 Premium Report

“Basically, owning NFTs is a way to display personal crypto wealth as well as speculate on prices. Collectibles have always been popular, and showing off digital collectibles on Twitter and elsewhere seems to increase that popularity, at least for now. While I think NFTs offer interesting future potential, I am very cautious about the prices of current projects in the long term. This space is very speculative, illiquid, and has a high probability of bursting like many previous crypto bubbles in history.”

Lyn Alden, September 5, 2021 Premium Report

“The fifth is likely to be a broad and prolonged crypto bear market, which we may or may not be entering now. NFTs may be particularly vulnerable in such a downtrend due to their lack of liquidity.”

-Lyn Alden, December 12, 2021 Premium Report

In fact, the number and prices of NFTs have fallen significantly over the past year.

Chart Source: Dune Analytics, @rchen8

6. Final Thoughts: Pandora’s Box Has Been Opened

Satoshi Nakamoto’s invention in 2008, itself a fusion of decades of previous work in cryptography and computer science, opened Pandora