Key Takeaways

EigenLayer has come under much unjust scepticism based on a misunderstanding of the protocol and its architecture.

EigenLayer does not rehypothecate assets, given depositors maintain control of assets, dictate the terms of their validation services, and are not subject to counterparty liquidity risks.

EigenLayer adds value to AVS network tokens, as opposed to stripping away elements of utility, and offers more than just bootstrapping security services.

LRT looping risk and liquidation cascade concerns do not impact EigenLayer itself, but rather the lending and borrowing protocols and markets that enable the looping.

Ethereum centralisation concerns are limited purely to smart contract risk and do not extend to similar concerns with LSTs, such as Lido, given a disconnect between control over validators and stake and the reallocation of assets.

Understanding EigenLayer: Economic Security Reimagined

Bootstrapping security for Proof-of-Stake (PoS) chains is notoriously difficult, requiring the accumulation and coordination of vast amounts of users and capital. Taking the time to carefully curate security for base chains has been an important task, although if we’re to expand to a world of thousands, and possibly even millions of app-chains, we need a more efficient way to reach the required security thresholds.

This is where EigenLayer comes in, a new primitive in cryptoeconomic security built to leverage the security of the Ethereum base chain through restaking. Essentially, restaking is the ability for users who stake their ETH on the consensus layer, be that natively or via a Liquid Staking Token (LST), to redeploy their staked ETH to secure an additional chain or application. Stakers are incentivised to do so by earning additional rewards. The chains or applications secured by this redeployed staked ETH are referred to as Actively Validated Services (AVSs).

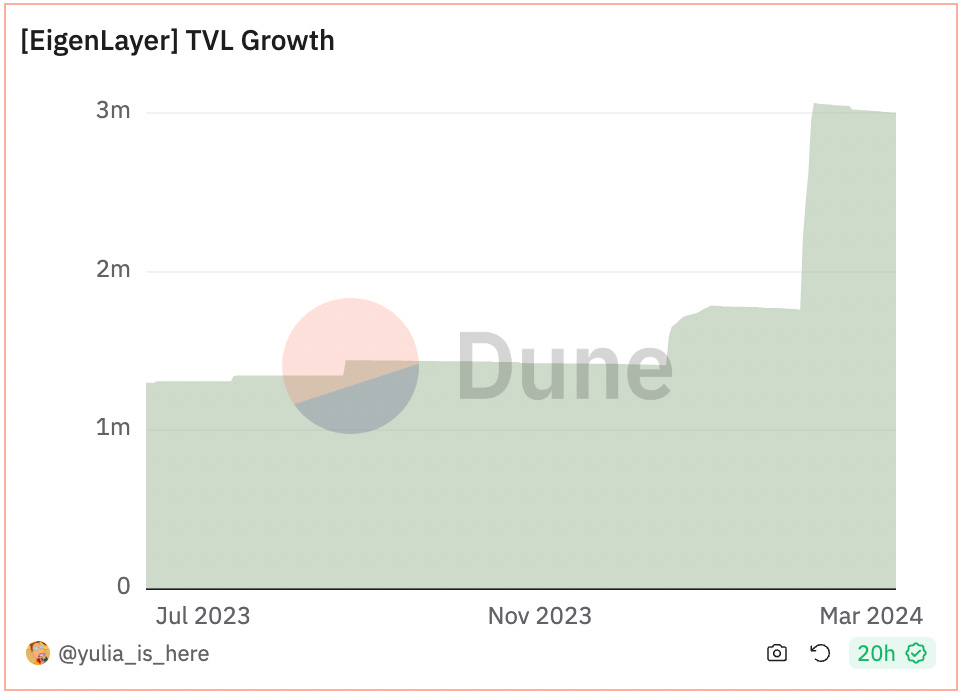

To contextualise the success of EigenLayer to date, it has accumulated ~3m ETH, equivalent to ~$11.9b in TVL since its launch in December 2023. This equates to a restake ratio of 2.5% of staked ETH.

Source: @hahaHash ‘EigenLayer Ecosystem Metrics’ Dune Dashboard

While the benefits of EigenLayer are clear, in that its innovations within cryptoeconomic security dramatically accelerate the time it takes to launch app-chains, there has been considerable scepticism around its architecture, and the impact on Ethereum, the AVSs it secures, and the ETH users restake.

This article aims to address these concerns and where appropriate explain in detail the debunking of such scepticism.

Staking Related Concerns

Rehypothecation Concerns in EigenLayer

Concern: The term rehypothecation often conjures up concerns within financial contexts. These concerns were heightened within the digital asset community by the events of 2022, with Celsius and FTX collapsing largely due to rehypothecation issues. In the case of EigenLayer, there's apprehension that it might employ rehypothecation practices with staked tokens.

Clarification: EigenLayer fundamentally diverges from traditional finance's rehypothecation practices. The EigenLayer protocol ensures that depositors retain full control over their staked ETH. This distinction is crucial for understanding the security and autonomy EigenLayer offers its users. In EigenLayer:

Stakers maintain complete control over their assets, unlike traditional rehypothecation, where depositors lose direct control to financial intermediaries.

Stakers dictate the terms of their validation services, reinforcing their autonomy within the ecosystem without being sidelined by intermediary decisions.

Depositors are not exposed to counterparty liquidity risks.

AVS Related Concerns

Concerns on AVS Network Token Utility with EigenLayer

Concern: There's a concern that the integration with EigenLayer might strip away the utility and value of AVS network tokens.

Clarification: Contrary to these concerns, EigenLayer arguably significantly enhances the value proposition of AVS network tokens rather than diminishing it.

Firstly, not all utility is captured through staking. Should an AVS network token grant governance rights over the AVS, investors will often assign it value. LDO is a good example of this, with the token primarily acting as a governance utility token over the protocol.

Moreover, all networks can employ a dual-staking model, whereby an AVS is secured by both its native token and ETH, should the AVS wish to add staking utility to the network token. This dual-staking mechanism not only diversifies the security model but also amplifies the utility and relevance of the AVS’s native token.

AVS governance would retain the ability to adjust the balance between its native token and ETH within its security structure, giving it flexibility as the native token gains value. In this sense, EigenLayer can act as a catalyst for enhancing the value of the AVS network token.

EigenLayer's Value Beyond Bootstrapping

Concern: There’s a concern that EigenLayer's utility and contribution to the ecosystem taper off after the initial bootstrapping phase of AVSs.

Clarification: While it is true that arguably EigenLayer is most impactful during the bootstrapping phase of an AVS, there are many other factors to consider.

EigenLayer reduces endogenous risk, by utilising ETH as part of a shared security mechanism and lowering the inherent risks associated with relying solely on a native AVS token. This is true at all stages of an AVS’s lifecycle.

I believe we’ll also see, as the AVS ecosystem expands, a benefit in the ability of different services to interoperate and leverage shared security features. Notwithstanding the ability for AVSs to rent security ‘on demand’, for example enabling the ability to flexibly switch on higher security for larger transactions etc.

Liquid Restaking Tokens Concerns

Before addressing the concerns surrounding Liquid Restaking Tokens (LRTs), let me quickly define them for context.

LRTs serve as the interface to the EigenLayer ecosystem by securing AVSs and offering a higher yield than ETH staking.

Essentially, users will deposit staked ETH tokens into the LRT protocol, and the LRT protocol will deposit their staked ETH tokens into EigenLayer. From this perspective, LRTs can be thought of as a delegation platform.

The big piece to focus on here however is the ‘liquid’ part. Within LRT protocols, depositors will receive liquid tokens that represent their deposit to the LRT protocol (and therefore to EigenLayer).

So, a user could stake ETH via Lido and receive stETH. They could then deposit this stETH to an LRT protocol, for this explanation let's call that ‘DPC Restaking’, which would issue a token representing this deposit, for example, ‘dpcETH’. The user can now go and use this dpcETH token in DeFi, retaining all the utility benefits of their original LST token (stETH).

If you’re interested in diving into current trends in LRTs, I’d recommend taking a look at this Dune Dashboard. LRTs have managed to accumulate ~1.4m ETH, equivalent to ~$5.8b in TVL, with leaders in the space being EtherFi, Renzo Protocol and KelpDAO.

Source: @hashed_official ‘LRT War - Liquid Restaking Token’ Dune Dashboard

LRT Looping Risk and Liquidation Cascade Concerns

Concern: Within DeFi, looping, raises concerns about potential liquidation cascades that could destabilise the system. There is a fear with LRTs that they could be used recursively to amplify leverage, leading to a precarious situation where cascading liquidations could occur and ultimately impact EigenLayer.

Clarification: EigenLayer has been designed with safeguards to prevent the occurrence of such looping risks within its ecosystem. Specifically, the protocol disallows the depositing of LRTs back into EigenLayer, effectively eliminating the possibility of looping LRTs within its system.

However, the broader DeFi lending markets operate independently, and the practices within these markets may involve leveraging LRTs.

Looping LRTs in lending markets is certainly a risk that could lead to liquidation cascades, although this risk is confined to the specific dynamics of those specific markets and protocols, and does not impinge on the security or stability of EigenLayer itself.

Ethereum Related Concerns

EigenLayer's Independence from Ethereum Social Consensus

Concern: The reliance on Ethereum's social consensus mechanisms by new protocols often raises questions about the autonomy and resilience of these systems. There's a specific concern whether EigenLayer's operational model might be too dependent on Ethereum's social consensus, particularly when it comes to unwarranted slashing risks.

Clarification: EigenLayer moves away from relying on Ethereum's social consensus for critical operational decisions, such as slashing. To address concerns related to unwarranted slashing risks, EigenLayer incorporates a unique feature: a slashing veto committee.

This committee functions as an internal mechanism to safeguard against such risks, mirroring the relay concept in MEV-Boost where a double-trusted party mediates interactions to maintain fairness and remove biases.

Looking ahead, EigenLayer plans to evolve beyond the need for a canonical veto committee, envisioning a marketplace where veto committees are chosen based on the overlapping preferences of operators and AVSs. This aims to enhance inter-subjectivity, allowing for a more nuanced and customisable approach to security and risk management.

EigenLayer's Impact on Validator Centralisation

Concern: A significant worry among the Ethereum community is whether the adoption of EigenLayer might inadvertently pressure Ethereum's validator set towards centralization. This concern stems from the understanding that increased validator requirements could favour more resource-rich operators, potentially skewing the network's decentralisation.

Clarification: It is true that EigenLayer, which imposes additional computational demands on Ethereum validators, in its current form is incentivising a centralisation vector for Ethereum.

EigenLayer attempts to mitigate this by leveraging its product, EigenDA, by incentivising the use of lightweight AVSs that utilise their DA service. This ensures that its operations remain accessible and sustainable for a wide range of validators, thus somewhat removing this centralising factor.

Furthermore, EigenLayer introduces delegation features that provide flexibility for validators. This system allows Home stakers, who wish to support Ethereum's security directly, the option to delegate the operation of more computationally demanding AVSs to other operators.

EigenLayer's Influence on Ethereum's Security Margin

Concern: There's a concern within the Ethereum community that EigenLayer, by leveraging Ethereum's staking mechanism, might erode the security margin of Ethereum itself.

Clarification: In short, EigenLayer does not compromise Ethereum’s security margin. When the stake in EigenLayer is significantly less than the total amount of ETH staked, there is no impact here.

If and when the stake in EigenLayer reaches a certain threshold of total ETH staked, which remains publicly undefined, the protocol sets aside a portion of this stake as a security buffer. This buffer acts as a safeguard, ensuring that only the remaining stake is utilised for EigenLayer's security provisioning, thereby maintaining Ethereum's security margin.

The Necessity of Self-Limiting for EigenLayer

Concern: Concerns have been raised about whether EigenLayer should implement self-limiting measures to avoid dominating Ethereum's validator set and influencing its decentralised nature.

Clarification: Centralisation concerns have historically sat at the layer that owns the validators, with major concerns coming specifically at the LST layer (i.e. Lido of late). The concerns have been targeted at LST protocols given their ownership of validators, and thus control over the Ethereum network. The difference between the LST layer and EigenLayer is that EigenLayer does not have any control over validators or stake.

This distinction is important because it explains why this centralisation risk does not apply to EigenLayer. As such, EigenLayer, through this argument, does not require self-limiting.

Of course, in terms of smart contract risk, it could be argued that EigenLayer should self-limit, given the value deposited to the protocol and its importance to the security of Ethereum.

Final Thoughts

EigenLayer manages to distance itself from key scepticisms once one is familiar with the protocol through distinctions stemming from control and ownership of assets, two key elements of digital assets.

Looking forward, I expect EigenLayer will further innovate to strengthen the integrity of the protocol in the face of such scepticism. The coming months will no doubt be incredibly exciting for the protocol.

If you’d like to engage for more frequent thoughts or reach out for discussion, you can find me on Twitter at @0xbenharvey, or simply click the button below.